Bitcoin Rebounded as Middle East Conflict Cools

26th June 2025 • 12 mins read

This Week’s Recap

U.S. Senate Passes GENIUS Act for Stablecoin Regulation: The Senate approved the bipartisan GENIUS Act by a 68–30 vote, creating a federal framework that treats payment stablecoin issuers as regulated financial institutions with reserve, transparency, and AML requirements. The law mandates 1:1 backing in safe assets, annual audits, and licensure to enhance consumer protection, though smaller issuers warn of higher compliance costs.

Solana Eyes Nasdaq Listing Amid Growing Ecosystem: Sol Strategies filed a Form 40-F to list on Nasdaq under the ticker STKE after raising up to $500 million via convertible notes. A successful listing could broaden institutional access to Solana projects, though valuation assumptions and market conditions will be closely watched.

Ethereum ETF Demand Slows Amid Macro Headwinds: Spot Ethereum ETFs recorded $19.7 million in outflows on June 20, the first net retreat after 30 days of inflows. Rising bond yields and equity market volatility weighed on ETH allocations, challenging its appeal as a yield alternative during economic tightening.

TRON Blockchain Goes Public, Boosting DeFi Interest: TRON completed a reverse merger with SRM Entertainment to form Tron Inc., taking the blockchain public in the U.S. via Nasdaq-listed SRM’s ticker. The move may attract traditional investors to TRON’s DeFi ecosystem, though added compliance obligations could slow its decentralized innovation.

JP Morgan Launches Deposit Token Pilot: JPMorgan introduced JPMD, a dollar-denominated deposit token on Coinbase’s Base network, enabling on-chain settlement with bank-grade KYC/AML. While JPMD promises settlement efficiency and auditability, its cross-bank utility remains to be proven in broader financial use cases.

Bitcoin Futures Open Interest Nears Record Highs: Open interest in Bitcoin futures hit $96 billion on June 21, nearing all-time highs as traders ramped up leveraged positions. The elevated leverage underscores bullish sentiment but raises the risk of large liquidations on sudden price swings.

Coinbase Launches Coinbase Payments with USDC: Coinbase rolled out a USDC payment stack on Base, partnering with Shopify for instant stablecoin checkout at millions of merchants. Success will depend on merchant integration incentives and consumer adoption of digital wallets, potentially accelerating mainstream crypto payments.

Central Asia’s First Solana Economic Zone Launches in Kazakhstan: Kazakhstan inaugurated a Solana Economic Zone offering tax breaks, infrastructure support, and Web3 education under an MOU with the Solana Foundation. The zone aims to diversify the economy and establish a regional crypto hub, contingent on ongoing policy backing and investor interest.

HIVE Digital to Buy Data Center for AI Infrastructure: HIVE Digital acquired a 7.2 MW Toronto data center to support up to 5,000 GPUs for high-performance computing and AI workloads. The pivot from pure crypto mining into enterprise AI services diversifies revenue and leverages HIVE’s data-center expertise.

Crypto Market Faces Liquidations Amid Iran Conflict: U.S. airstrikes on Iran’s nuclear sites triggered $595 million in crypto liquidations as BTC and ETH briefly dropped over 5%. Traders recovered quickly once the conflict’s scope narrowed, underscoring crypto’s sensitivity to geopolitical events.

Circle’s Market Cap Surpasses USDC Value: Circle’s market cap briefly exceeded its USDC supply of $61 billion following its IPO-fueled share rally. The gap highlights investor confidence in stablecoin infrastructure, though growth in USDC usage will be the true test.

Texas Enacts Law to Seize Bitcoin in Criminal Cases: Governor Abbott signed SB 1498, allowing Texas authorities to forfeit cryptocurrency tied to crimes and direct proceeds to a special fund. Advocates call for due-process safeguards as law enforcement prepares to leverage the new crypto-seizure powers.

Fiserv to Launch US-Dollar Stablecoin FIUSD by Year-End: Fiserv, in partnership with Circle and Paxos, will issue FIUSD to integrate with 6 million merchants and 10,000 financial institutions. Fueled by GENIUS Act clarity, FIUSD aims to bridge fiat rails and crypto, though execution risks around compliance and interoperability remain.

GameStop Plans Bitcoin Acquisitions for Treasury: GameStop exercised a $450 million greenshoe on its convertible debt, raising total proceeds to $2.7 billion for potential BTC buys. The strategy may reshape GameStop’s narrative toward digital-asset holdings, though investors debate the impact on its core retail business.

Barclays to Ban Crypto Purchases via Credit Cards: From June 27, Barclays will block all crypto transactions on its credit cards to protect customers from volatile markets. Supporters praise the move as prudent risk management; critics warn it may drive users to unregulated alternatives.

Kraken Expands Stablecoin Offerings with New Partnerships: Kraken added native USDC support on Arbitrum, Optimism, and Polygon, plus deposits/withdrawals for USDT, DAI, PYUSD, and more. The expanded lineup aims to deepen liquidity for DeFi protocols, institutional traders, and cross-border payments.

Ripple Expands Cross-Border Payment Solutions: Ripple partnered with Standard Chartered and Flutterwave to roll out On-Demand Liquidity rails in Asia and Europe using XRP as the bridge asset. The collaboration seeks to cut FX costs and compliance friction for remittance providers, furthering blockchain adoption in real-world payments.

Bitcoin Market Analysis

Bitcoin’s rally picked up pace this week, rising from a June 19 close of $103,934.50 to hit $107,902 on June 26. It reclaimed the $105,000 zone early in the week and tested $108,000 resistance, confirming the short-term uptrend that emerged after breaking above $100,000 support last week. That breakout signaled renewed confidence among traders, who piled back in around key levels and helped push price to fresh local highs.

Source: https://altfins.com/technical-analysis

Technically, the outlook remains firmly bullish. Bitcoin sits comfortably above its 200-day simple moving average near $96,000, anchoring the long-term trend. The 14-day RSI hovers at 54, indicating healthy momentum without overbought extremes, while the MACD histogram has turned positive as the MACD line crossed above its signal line, suggesting buyers are regaining control. Trading volume has stayed in line with recent norms, and the old $100,000 resistance now acts as a polarity zone any dip to $100,000–$103,000 should attract buyers, reinforcing that level as reliable support.

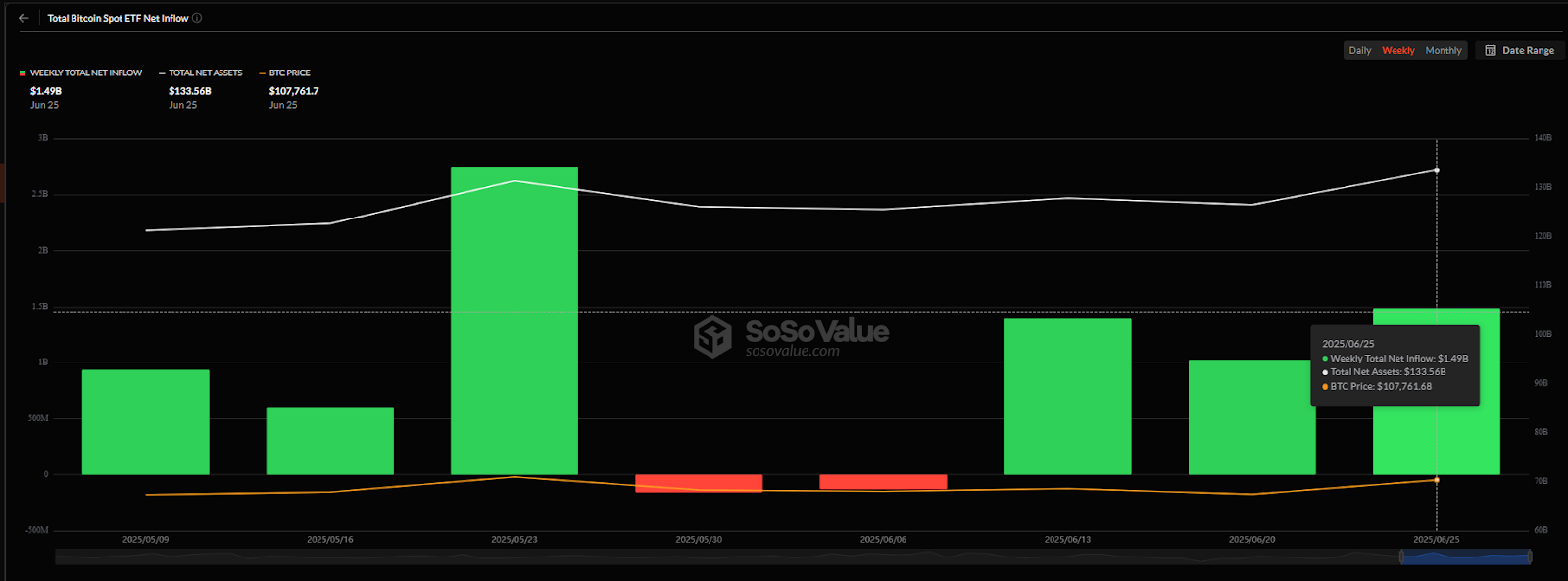

On the fundamentals side, institutional demand shows no signs of slowing. Since Bitcoin’s all-time high in May, six of the last eight weeks have seen net positive spot ETF inflows, with just two minor outflows in late May and early June. The week ending June 25 alone brought in $1.49 billion, lifting total ETF assets to $133.6 billion as Bitcoin traded between $100,000 and $112,000. Those steady inflows underscore how large investors are quietly stacking Bitcoin, effectively building a price floor under current ranges.

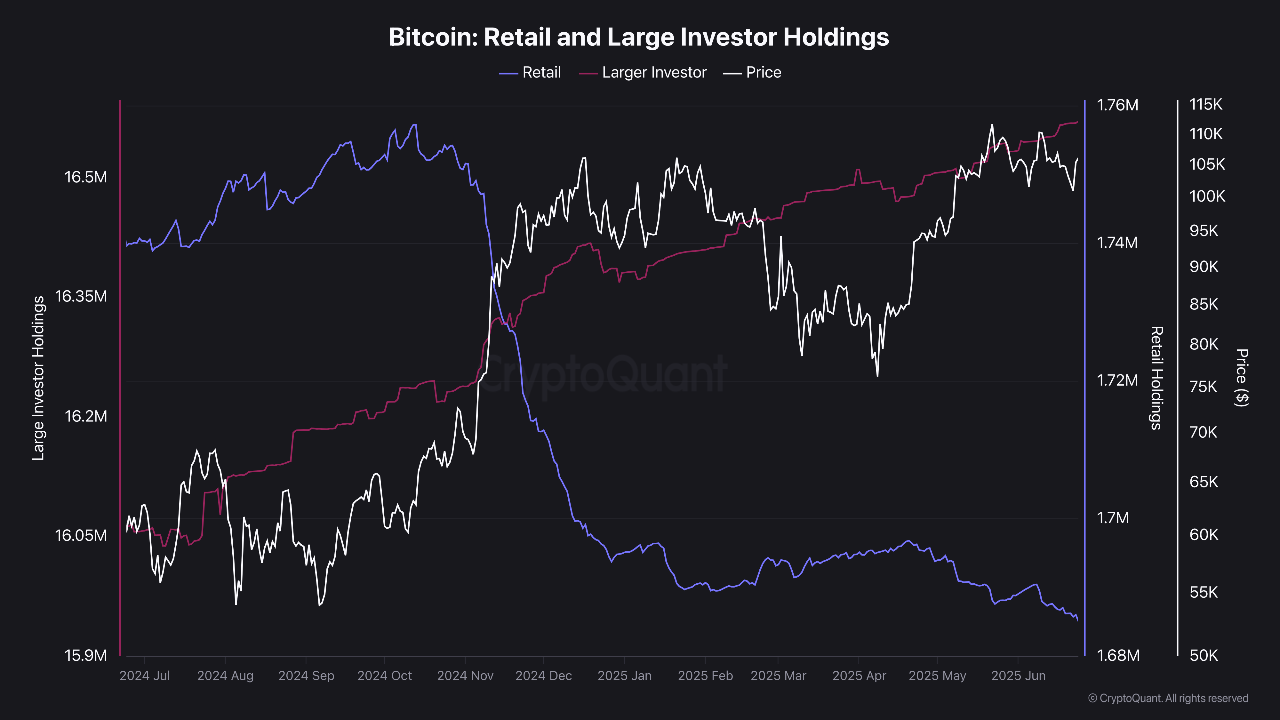

Meanwhile, on-chain metrics reveal supply flowing steadily into stronger hands. Retail wallets now hold 1.69 million BTC—a year-on-year drop of 54,500 at roughly 220 BTC per day—while large addresses (≥1,000 BTC) control 16.57 million, up 507,700 coins over the same period at about 1,460 per day. Institutions are absorbing about seven times more Bitcoin than small holders release, creating a genuine squeeze. This upstream shift shows up in exchange flows too: on June 24, Binance net taker volume topped $100 million—driven by retail buying and forced short covering—while stablecoin withdrawals from derivatives platforms reached $1.25 billion, the largest since mid-May.

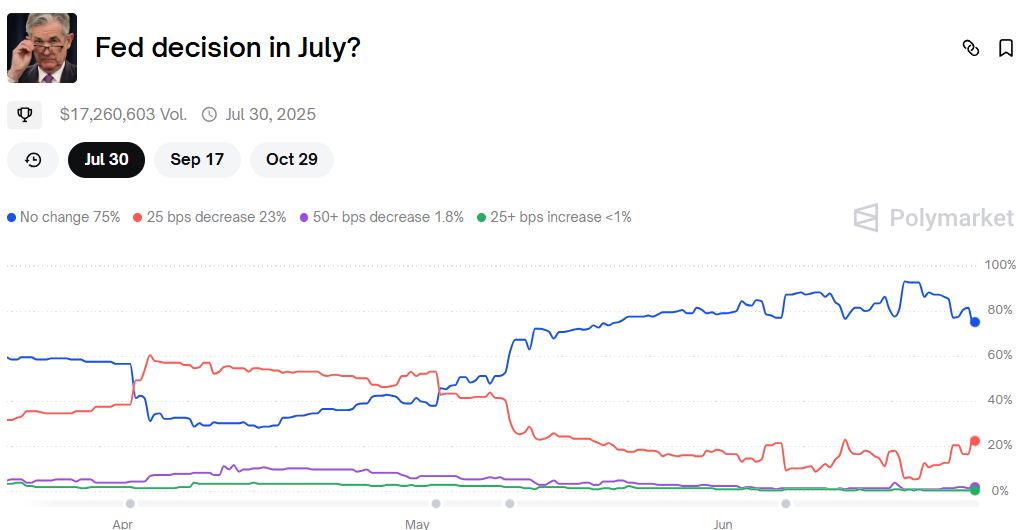

Finally, macro forces add another layer of complexity. Fed Chair Jerome Powell has made clear that a July rate cut is unlikely, yet Polymarket odds for a 25-basis-point cut have climbed from roughly 7 percent in June 19 to about 20 percent today. That disconnect suggests traders either expect inflation to remain subdued through July or anticipate political pressure could force the Fed’s hand. Taken together—the technical strength, institutional accumulation, supply squeeze and clashing monetary signals—Bitcoin appears poised at a critical inflection point where a healthy pullback may be more probable than a straight run to new highs.

Ethereum Market Analysis

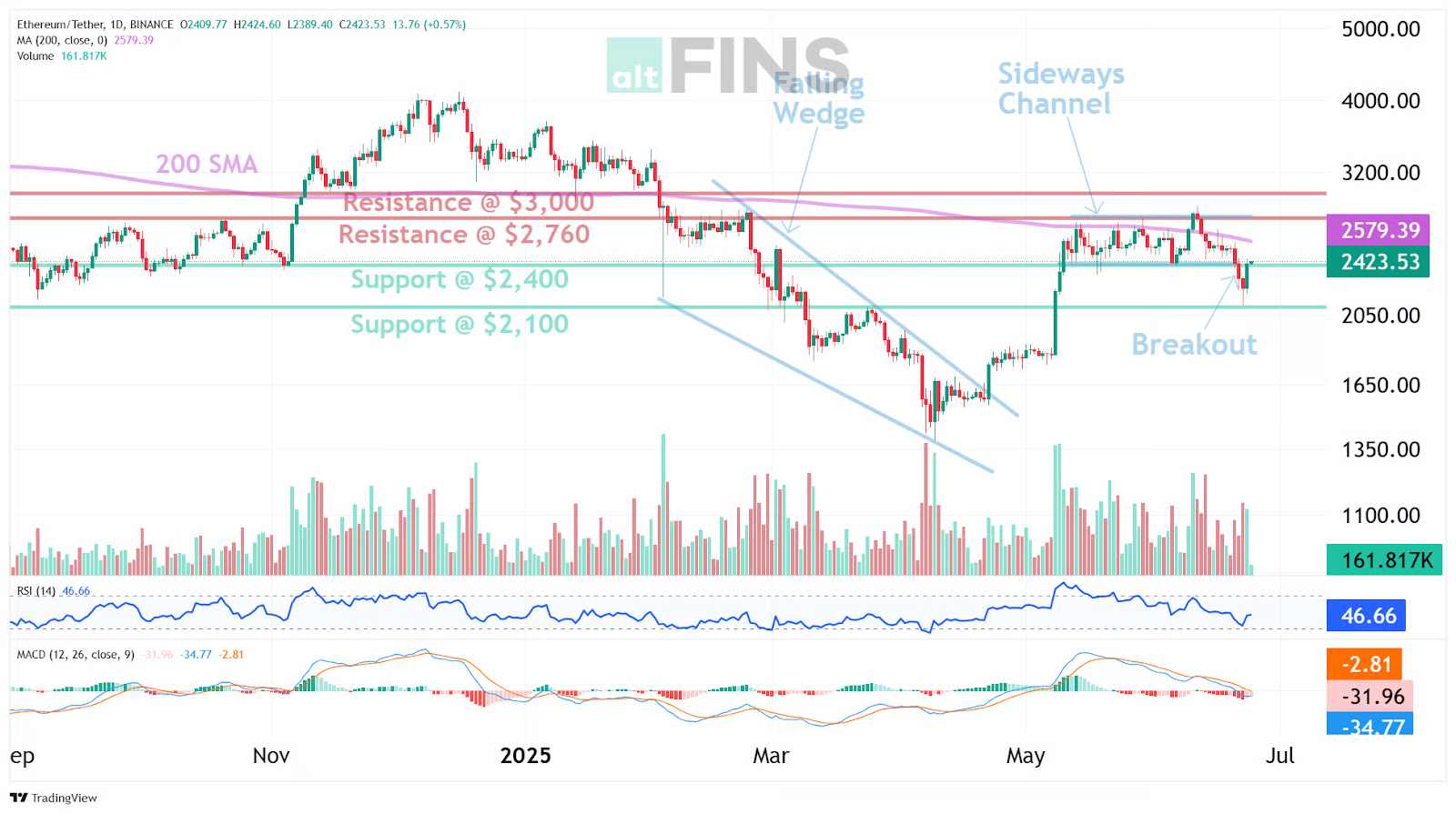

Over the past seven days, Ether slipped from the top of its $2,400 to $2,760 trading range into a clear downtrend. Early in the week it still hovered near $2,700 but a break below $2,400 support signaled sellers taking control. That breakdown carried price under the 200-day moving average around $2,580 and confirmed a shift from last week’s neutral channel into a short-term decline that remains intact today.

Source: https://altfins.com/technical-analysis

Technical indicators reinforce this bearish bias but hint at a potential pause. The 14-day RSI is sitting around 46, so Ether is neither overbought nor oversold. The MACD line remains below its signal line but the histogram bars have been rising, suggesting momentum may be bottoming out. Volume has stayed steady on the sell-off, lending conviction to the break from the sideways channel.

Looking ahead, $2,400 and then $2,100 stand out as the first support zones where buyers might step in. On the upside, reclaiming $2,760 would open the door for a move back toward $3,000. With short- and medium-term trends still down, it makes sense to wait for a decisive bounce above the recent channel before assuming a turnaround. Setting an alert at $2,400 can help you catch the next swing, whether it’s a rebound or another leg lower.

Regulatory clarity around spot Ethereum ETF staking can reshape Ether’s outlook. If U.S. regulators allow ETFs to stake ETH directly, institutional demand could surge as investors chase yield. This catalyst comes amid $19.7 million in outflows on June 20 and mounting macro pressures, showing how clear rules could turn sentiment upside down. Watching updates on staking approvals will be crucial to see if this new demand can halt the downtrend.

Institutional Adoption

Over the past week, traditional finance and crypto have moved closer as established institutions and public companies took concrete steps into digital assets. SOL Strategies filed a Form 40-F to list on Nasdaq under the ticker STKE, providing institutional investors with direct exposure to Solana-based projects. At the same time, TRON completed its reverse merger with SRM Entertainment to become Tron Inc., making its DeFi ecosystem accessible through a U.S.-listed vehicle.

Meanwhile, banks and payment processors introduced tokenized deposit solutions designed for efficiency and compliance. JPMorgan launched JPMD, a dollar-denominated deposit token on Coinbase’s Base network, marking the first major bank-issued digital deposit on a public Layer-2 chain. Fiserv announced FIUSD, a stablecoin built with Paxos and Circle, which will integrate into its payments infrastructure serving over ten thousand institutions and six million merchants. These offerings aim to streamline settlement and provide transparent audit trails without compromising regulatory standards.

Corporate treasury strategies also reflected growing interest in digital assets. GameStop exercised a $450 million greenshoe option, bringing its available capital for Bitcoin acquisitions to $2.7 billion and signaling a cautious move toward holding digital gold as part of its reserves. With clearer stablecoin regulations in place, we expect additional partnerships between major financial firms and blockchain networks in the coming months, as digital assets continue to transition from niche instruments to standard elements of financial operations.

What to Expect in July

July’s macro backdrop is set to hinge on central banks and policy risks. In the United States, markets will zero in on the Federal Open Market Committee meeting scheduled for July 29 and 30, parsing any shifts in the dot-plot forecasts and listening closely to Chair Powell’s comments. While Governor Waller has openly suggested cutting rates as soon as this meeting, citing cooling inflation and a softer labor market, several colleagues remain more reserved. Abroad, the European Central Bank appears likely to stand pat at its two percent policy rate before considering any easing later in the year, and the Bank of Canada faces the tricky task of balancing slowing growth against persistently sticky price pressures.

New U.S. tariffs on steel, aluminum and autos have added to policy uncertainty. The Trump administration has also postponed several of its threatened reciprocal levies into early July for example, the 25 percent tariff on Japanese cars and matching duties on other Japanese goods are held off until July 9 before they could snap back up to 25 percent. Planned 50 percent tariffs on EU imports face the same July 9 deadline, giving negotiators more time to strike a deal . Keep an eye on debt-ceiling talks in Congress any stalemate could trigger fresh volatility.

On the growth and inflation front, forecasts point to U.S. GDP growth slowing toward 1.4 percent this year, with core PCE inflation gradually re-anchoring near three percent before drifting closer to the Fed’s two percent target. The OECD’s latest outlook anticipates global growth of around 2.9 percent in 2026, down from 3.3 percent in 2024, while trade frictions and ongoing policy uncertainty remain clear headwinds.

Earnings season will wrap up in July, with analysts forecasting roughly five to seven percent growth in S&P 500 profits, driven by financials and energy even as consumer staples feel the squeeze from higher wages and input costs. In the commodities complex, Brent crude is trading between seventy-five and eighty dollars a barrel as OPEC+ curbs counter softer Chinese demand, while gold is finding support near twenty-one hundred dollars an ounce amid growing rate-cut expectations.

Mark Your Calendars

Economic Data Releases:

- July 3, 2025 (Thursday): U.S. employment report

- July 3, 2025 (Thursday): U.S. unemployment rate

Token Unlock

- July 1, 2025: SUI (SUI) unlocks $119.23 m (1.30 % of market cap)

- July 2, 2025: ENA (ENA) unlocks $10.58 m (0.67 % of market cap)