Executive summary

Ethereum enters September 2025 with a valuation that is similar to late 2021, yet the foundation that supports that valuation is materially different. Ether trades near prior cycle highs, while the network now operates under Proof of Stake, supports materially higher effective throughput through Layer 2 execution, and exhibits a supply profile that is close to flat due to sharply lower issuance and persistent fee burns. Institutional access has expanded through regulated exchange traded products, while staking has locked a large share of circulating ETH, which reduces freely tradable supply. Daily on chain activity has approached record territory, yet mainnet fees are a fraction of 2021 levels because activity has migrated to rollups after the Dencun upgrade introduced data blobs for cheaper rollup publishing. In DeFi, headline TVL in dollars has almost returned to 2021 territory, although TVL in ETH terms is lower and composition has shifted toward liquid staking, restaking, and real world asset collateral. NFTs, after a period of exuberance in 2021, have consolidated onto blue chip collections and lower cost Layer 2 venues. Ethereum’s most credible competitor in the L1 space remains Solana, which has captured cultural mindshare in retail driven use cases, but Ethereum continues to lead on developer share, capital depth, and institutional integration.

Market overview, price and capitalization

Where valuation stands now versus 2021

Ether’s prior cycle high was set in November 2021 at $4,891 range. In late August 2025, multiple market data outlets reported fresh intraday highs in the 4,879 to 4,957 range, implying that price has effectively revisited and, on some exchanges, exceeded the 2021 peak. These levels place market capitalization back around the mid 500-billion-dollar area, like late 2021.

Source: https://www.tradingview.com/chart/

What is different in the demand mix

In 2021, the marginal buyer was frequently a retail participant interacting with DeFi farms and NFT mints on mainnet. In 2025, regulated spot ETH exchange traded funds have added a channel for institutional demand, and staking has removed a substantial portion of supply from immediate circulation. Industry commentary and monthly flows show that exchange traded products accumulated meaningful net inflows through mid 2025, which supported the price advance into late summer.

DeFi, TVL, and market structure

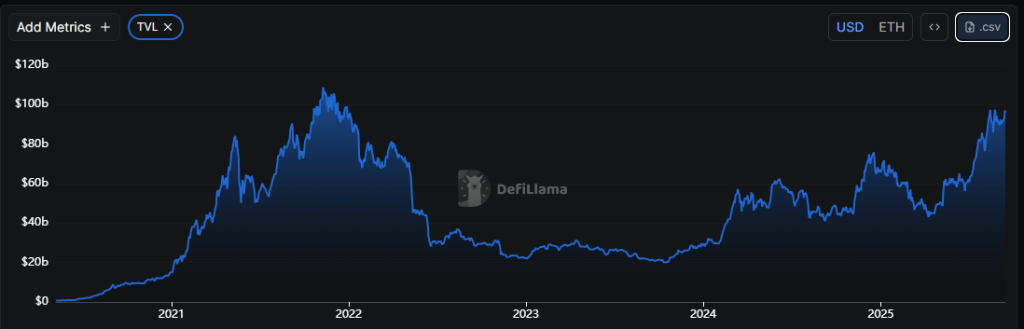

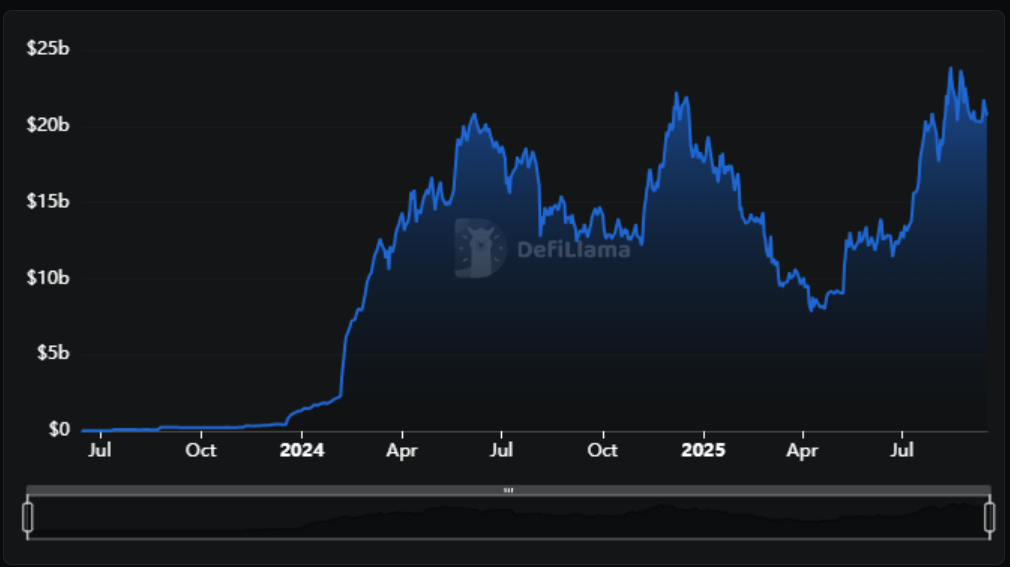

Headline TVL has recovered in dollar terms, composition has changed

At the end of 2021, DeFi TVL on Ethereum peaked at about $105b. By late August 2025, aggregate DeFi TVL on Ethereum has recovered to roughly $95b, a level that is close but still below the prior all-time high in dollar terms and meaningfully lower when measured in ETH due to shifts in collateral composition and liquidity migration to Layer 2 venues. Several market trackers in late August highlighted this gap to the 2021 peak and framed 2025 as a recovery period rather than a full cycle retest of prior highs.

Source: https://defillama.com/chain/ethereum

Liquid staking now anchors the DeFi stack. Lido’s stETH and other liquid staking derivatives have become the dominant form of base collateral across lending markets, structured yield platforms, and rollup-native applications. MakerDAO’s collateral base has diversified into tokenized Treasuries and other real-world assets, setting 2025 apart from the crypto-native collateral mix of 2021. At the same time, perpetual swap exchanges and structured products have proliferated on Layer 2 networks, which allows leverage and hedging activity without the mainnet’s fee constraints.

Risk, capital efficiency, and the end of emission driven TVL

In 2021, many protocols attracted liquidity through high token emissions, recursive borrowing, and liquidity mining. In 2025, capital efficiency is achieved through concentrated liquidity AMMs, oracle design improvements, and protocol revenues that derive from actual usage. Emissions have not disappeared, however they are a smaller part of aggregate returns compared with 2021. Real yield in the 2025 context refers to fees, MEV revenue shares to validators and stakers, and tokenized fixed income coupons, rather than purely inflationary token issuance.

Network usage, throughput, and fees

Transactions and active addresses near records, fee burden structurally lower

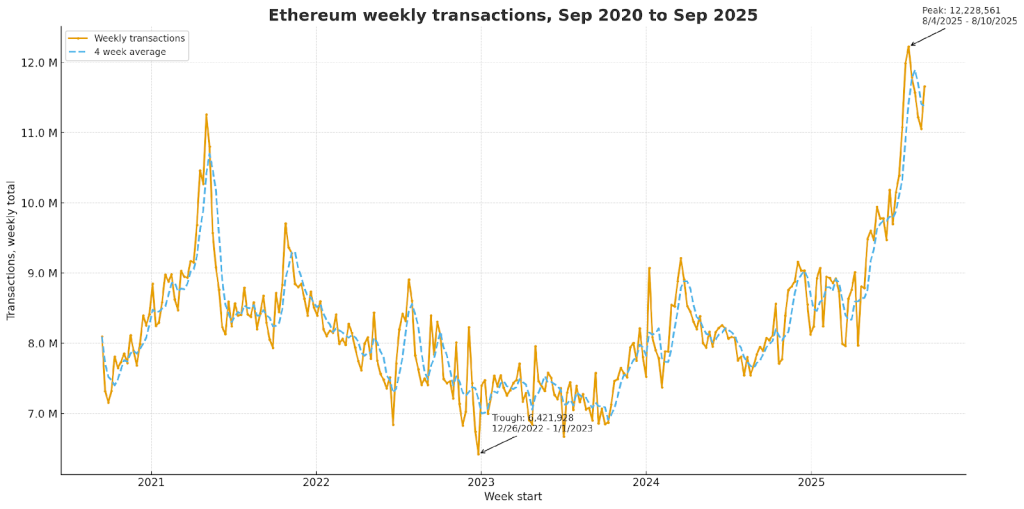

Ethereum Layer 1 processed nearly 1.8 million transactions on August 15, 2025, placing activity within striking distance of the historical high near 1.9 million transactions in a day. Daily active addresses moved toward the 600,000 area during August, which ranks among the highest sustained periods on record when excluding known one off spam spikes. Despite the high utilization, fee revenue in 2025 is far lower than the 2021 peaks because a large share of retail and application interactions occur on rollups. One industry outlet summarized the August activity spike together with an estimate of roughly 97 billion dollars locked in DeFi at that time, which aligns with the TVL observations above.

In parallel, token burn that accrues to holders through EIP 1559 has varied with fee levels. A recent summary of monthly Ethereum revenue that tracks burn pointed out that revenue fell sharply in August even while price printed fresh highs, underscoring how scaling has decoupled price from fee spikes.

Why fees fell and throughput rose, the role of Dencun and EIP 4844

The Dencun upgrade on March 13, 2024 introduced proto danksharding, often referred to as EIP 4844, which added data blobs for rollups. This change reduced the cost of data availability for rollups, which is the largest cost component for optimistic and zk rollups, and it improved the throughput capacity of the combined system at a given fee level. As a result, more user transactions fit into the same cost envelope. Documentation and educational write ups published at the time confirm the go live date and the purpose of blobs as a transitional step toward full danksharding.

Source: https://app.artemisanalytics.com/

Layer 2 adoption and the modular stack

Execution has moved to rollups

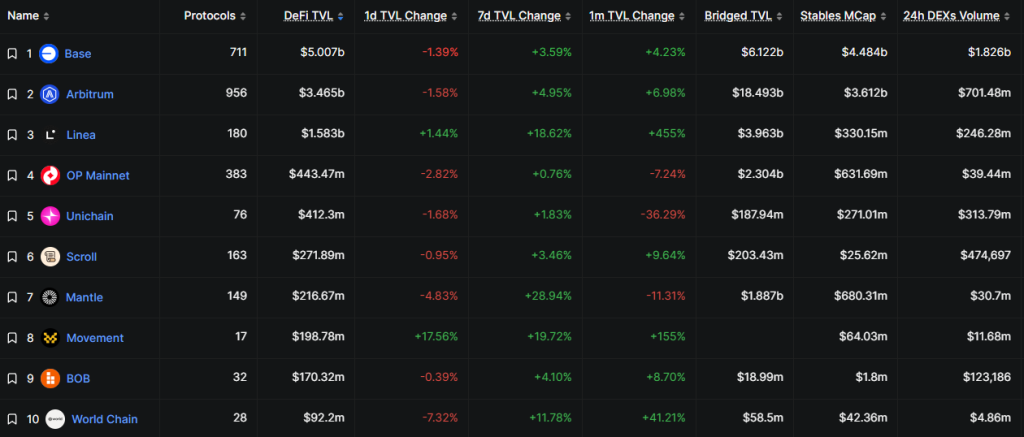

By 2025, the primary execution surface for retail users and many applications resides on rollups such as Arbitrum, Optimism, Base, and several zk based systems. These networks regularly clear millions of transactions per day at fees that are measured in cents rather than dollars. Coinbase’s Base launched in 2023 and grew into one of the most active rollups, becoming a home for consumer oriented social applications, NFT activity, and a growing DeFi base. Various ecosystem summaries in 2025 placed Base’s DeFi TVL in the multibillion dollar range, with frequent references to approximately $5b during the summer.

Source: https://defillama.com/chains/rollup

Arbitrum has specialized in derivatives and leveraged trading, including order book and GMX style perpetuals, while Optimism has pursued an open-source OP Stack model that powers additional rollups including Base. zkSync, Scroll, and Starknet have focused on zero knowledge proof performance and EVM compatibility. Liquidity has become more distributed, which required better bridges, message passing, and unified order routing to deliver acceptable user experience across rollups.

What this means for Ethereum’s economics

Mainnet fee revenue is lower than in 2021 because fewer transactions compete directly for Layer 1 block space. Value accrual comes through settlement usage by rollups, the economic security of staked ETH, and the network effect of assets and applications that remain anchored to Ethereum’s security domain. This shift is consistent with the long-discussed idea that Ethereum is a settlement and data availability layer for a modular stack where execution migrates to layers that can scale cheaply.

ETH supply, issuance, staking, and validators

From inflationary PoW to near flat PoS supply

Under Proof of Work in 2021, annual issuance approximated 4 to 5 million ETH, which implied a mid single digit inflation rate unless offset by unusually high burns. The Merge in September 2022 reduced issuance by roughly 90 percent, while EIP 1559 continued to burn a portion of fees. In practice, post Merge supply has been close to flat through mid 2025, with month to month drift depending on fee levels. Educational summaries of the Merge consistently describe the order of magnitude reduction in issuance that underpins this shift.

Staking participation and validator count

Staked ETH has grown from roughly 7 to 8 million ETH in September 2021 on the Beacon Chain to more than 35 million ETH in mid 2025, which corresponds to approximately 30 percent of circulating supply. Several market data recaps and Dune Analytics sourced stories during July and August 2025 cited the 36 million ETH area as a reference point. At the validator level, Ethereum has exceeded one million active validators in 2025, with recent reporting around mid September noting that the total active set is well above that threshold.

Yields have normalized toward the mid single digit range, reflecting the larger staking base and the evolution of priority fees and MEV capture into validator and delegator revenue. Shanghai in April 2023 enabled withdrawals, which removed the liquidity risk that had constrained some staking participation during 2021 and 2022.

Liquid staking and concentration risks

Liquid staking derivatives, most notably Lido’s stETH along with Rocket Pool’s rETH and Coinbase’s cbETH, now represent a large share of staked ETH. The convenience and composability of these tokens created a base collateral for DeFi. However, the concentration of staking with a handful of operators introduces governance and correlation risks. Institutional allocators often prefer pooled staking or regulated providers for operational reasons, which can amplify concentration effects unless counterbalanced by solo stakers and decentralized pools.

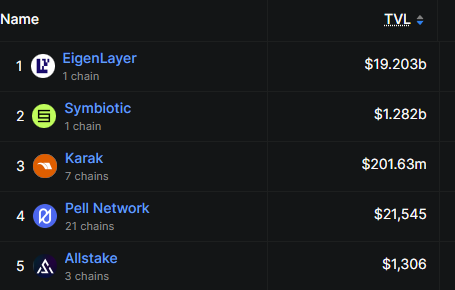

Restaking as an emergent layer

Restaking on EigenLayer allows ETH and LSDs to secure middleware and services in exchange for additional yield. This introduces new income streams for stakers, yet it also brings new vectors of slashing and smart contract risk. As restaking grows, risk management frameworks must account for correlated failures and cross protocol dependencies.

Source: https://defillama.com/protocols/restaking/ethereum

NFTs and token markets

From mania to a more durable base

NFT activity on Ethereum during 2021 featured multi billion dollar monthly volumes, frequent gas auctions on mainnet, and widespread retail participation. In 2025, NFT activity on Ethereum mainnet is markedly lower. On August 1, 2025, analytics tallies recorded approximately 1,127 NFT trades on Ethereum mainnet, which is an all time low count for that series. The downshift illustrates how activity has consolidated into blue chip collections, into Layer 2 marketplaces, and into use cases where transaction costs are negligible relative to asset price.

Blur overtook OpenSea in professional trading share during 2023 and 2024, and marketplace competition has changed royalty practices and creator economics. On the other side, Base has emerged as a Layer 2 home for NFT minting and trading that targets retail friendly fee levels, and brand oriented programs continue to operate on Polygon and other low cost environments.

Tokens, stablecoins, and real world assets

The ERC 20 token landscape in 2025 emphasizes yield backed tokens, stablecoins with strong attestation, and tokenized fixed income. MakerDAO’s transition toward real world collateral, the growth of tokenized Treasury funds, and the participation of regulated asset managers on Ethereum and its rollups have shifted attention away from emission driven governance tokens. The collapse of algorithmic stablecoins in 2022 ended the prior cycle’s most aggressive experiments and raised the bar on design and disclosure for new stablecoin initiatives.

Developer activity and ecosystem growth

Developer share and project count

Multiple ecosystem reports during 2025 place Ethereum at the top of smart contract platforms by active developer share and by project count. One widely circulated 2025 summary shows approximately 20,8 percent of active crypto projects built on Ethereum, with the next largest ecosystems around the low double digits. A plurality of Ethereum developers now target Layer 2 environments, which is a change from 2021 when most developer effort landed on mainnet. The migration reflects the reality that new consumer applications, games, and high frequency trading venues require the cost structure of rollups to be viable.

Grants, venture, and institutional capital

Grant making has continued through the Ethereum Foundation and public goods funding programs, while venture funding has become more selective than in 2021. Capital today favors scaling infrastructure, zero knowledge research and engineering, account abstraction tooling, custody and compliance layers, and applications that have a clear line of sight to revenue. Institutional allocators have moved from experimental pilot programs toward formal allocations in vehicles that hold staked ETH or tokenized fixed income, which in turn has shaped the type of applications that find product market fit.

Protocol upgrades that guided developer focus

The Merge in 2022, Shanghai in 2023, and Dencun in 2024 provided a predictable cadence that aligned developer roadmaps. The first removed mining and reduced issuance, the second enabled withdrawals that catalyzed staking adoption, and the third enabled cheaper rollup data that catalyzed Layer 2 execution growth. Education resources published at each stage document both dates and the primary technical objectives, which has helped enterprise stakeholders plan multiyear deployments. That cadence has continued with the Pectra upgrade in May 2025, which raised validator effective balances and advanced account abstraction. Looking forward, the Fusaka hard fork scheduled for late 2025 is set to deliver PeerDAS and data availability sampling, followed by the Glamsterdam fork in 2026 with Verkle trees. Together these upgrades maintain a transparent roadmap that enterprises can track against their infrastructure planning cycles.

Closing Thoughts

Ethereum in September 2025 is not the same network that existed in September 2021, despite similar price levels. The network has shifted to Proof of Stake, it has scaled through a modular rollup centric design, and it has attracted institutional capital through exchange traded products and staking programs. The transaction data in August 2025 show that demand for block space remains healthy, yet the fee burden on end users is lower because execution has migrated to rollups and because data costs are lower after Dencun. The supply profile is structurally stronger than in 2021 due to the order of magnitude reduction in issuance after the Merge. Staking participation near 30 percent of supply, and a validator set that exceeds one million, point to a widely distributed security budget, although concentration within large liquid staking providers deserves continued attention.

DeFi has matured from emission driven loops into a system anchored by yield bearing collateral, tokenized fixed income, and rollup native derivatives. NFTs have normalized after the 2021 boom, with mainnet activity consolidating and lower cost environments handling high frequency trading and minting. Developer share data and industry surveys continue to place Ethereum at the center of smart contract development, with a meaningful tilt toward Layer 2 engineering and product design.

Competition is active and credible. Solana has built a thriving culture around low fee, high throughput applications, and EVM alternatives continue to serve large user populations. The modular path allows Ethereum to respond without abandoning security and decentralization goals, which is visible in the broad adoption of rollups, the OP Stack model, and the continued investment in zero knowledge proof systems.

Looking ahead, the determinants of value for Ethereum appear to be the pace of rollup adoption, the health of staking and restaking markets, the durability of exchange traded product inflows, and ongoing progress on data availability and proof systems. The past year’s data points, including new price highs on several venues, high transaction counts on mainnet, and the growth of staked ETH, indicate that Ethereum has translated 2021’s demand into a more sustainable architecture. The continued integration of real world assets, the improvement in account abstraction and wallet UX, and the hardening of cross domain infrastructure will influence whether the next stage of adoption broadens beyond the current user base.