Past the CLARITY Bounce

21th May 2026 • 8 mins read

This Week’s Recap

- Trump executive order opens Fed payment rails to crypto firms: The order instructs the Federal Reserve to deliver findings within 120 days on whether non-bank digital asset firms should connect directly to central bank settlement, with Kraken, Ripple, Coinbase, Circle, Anchorage, Paxos, and BitGo all in the frame. If carried through, it would let stablecoin issuers and exchanges move high-value dollars without leaning on a correspondent bank, a structural change to how the dollar moves on-chain.

- Senate curbs Trump’s Iran war powers: A 50-47 vote advanced the Iran War Powers Resolution and eased the late-week energy shock that had pushed crude above $107 a barrel. Oil dropped under $97 on the news, and Bitcoin, Ether, and XRP all caught a small relief bid into Wednesday’s close.

- Tether buys SoftBank’s stake in Twenty One Capital: The stablecoin issuer acquired a 26% holding as SoftBank exited, pushing Tether deeper into the listed Bitcoin treasury and mining stack. The move sits alongside Tether’s expanded T3 compliance unit and recent capital-markets push, turning the company into a more direct participant in the Bitcoin equity trade rather than only its dollar liquidity layer.

- Pan-European stablecoin effort expands to 37 lenders: The Qivalis consortium added more banks ahead of a planned euro-backed token launch in the second half of 2026, framed openly as a response to US dollar dominance in stablecoin markets. A bank-issued euro stablecoin with this much network behind it would be one of the first credible non-dollar payment tokens with European regulatory cover.

- Truth Social drops its spot Bitcoin ETF plan: The withdrawal followed an ETF fee war that has driven competing products to as low as 14 basis points, with Morgan Stanley and other late entrants undercutting earlier issuers. The pull shows how hard it has become to launch a new spot Bitcoin ETF profitably once the largest issuers already own the distribution.

- Polymarket partners with Nasdaq on private-company contracts: The collaboration will let users trade on startup milestones and private valuations through a regulated venue, taking prediction markets beyond elections and sports into corporate finance. It pairs with the Trade.xyz SpaceX perpetuals that opened the week, both signs that synthetic exposure to private companies is becoming a real product line.

- Echo Protocol suffers $76 million exploit on Monad: An attacker minted 1,000 unauthorised eBTC on Monad in a single attack, the second protocol-level minting failure of the spring after the KelpDAO and rsETH incident in April. Echo was a higher-profile launch on a new chain, and the loss reinforced how exposed wrapped-asset designs remain when the issuance contract becomes the attack surface.

- Former BNY exec launches NUVA with $19 billion of tokenised assets: NUVA is routing Figure-originated home-equity loans and Treasury collateral into Ethereum-based DeFi, with a former Bank of New York executive leading the build-out. The project is one of the largest single tokenised-asset pipes pointed at on-chain credit markets, and it gives ETH another quiet anchor in the institutional collateral stack.

- Strategy purchases 24,869 Bitcoin for $2 billion: Saylor lifted total holdings to 843,738 BTC at an average cost of $75,700 per coin and bought into the week’s pullback rather than chasing the earlier $82,000 print. The buy made Strategy the most visible bid in the market on a week when ETF flows were turning negative.

- Bitcoin Depot files for bankruptcy: North America’s largest Bitcoin ATM operator took down more than 9,000 kiosks after Q1 revenue fell 49.2% and roughly $20 million in legal judgments hit the books. A wave of state-level restrictions on crypto ATMs over the last year has changed the unit economics for retail cash-to-crypto, and the filing reads as a structural rather than a cyclical exit.

- Stripe-backed Tempo taps $7.5 billion DeFi lender Morpho: The integration plugs Morpho’s lending engine into Tempo’s payment stack and gives the Stripe-backed network on-chain credit alongside settlement. It is one of the first cases of a major payments-led project building yield and credit functions directly into the rails, rather than bolting them on afterward.

- Standard Chartered takes full ownership of Zodia Custody: The bank moved to buy out the remaining stakes in its crypto custody venture and bring it fully in-house. The shift fits the broader pattern of large banks treating digital asset custody as a core product rather than a joint-venture experiment, the same direction Galaxy’s New York licence and Minnesota’s custody law pointed this week.

- Galaxy receives New York BitLicense for institutional push: Novogratz’s firm became the second to clear New York’s BitLicense bar this year and now has the framework to expand custody, trading, and tokenisation products into the state’s institutional client base. The licence carries the most demanding compliance posture of any US state regime, so each new approval tends to drag the broader institutional bar up with it.

- Big banks move billions into Solana for tokenisation: Wall Street firms have started routing tokenised fund and payment volume through Solana, repositioning a chain that spent the previous cycle defined by meme trading. The flow gives Solana its first credible institutional narrative this year and pulls the tokenisation race past the BTC-and-ETH-only frame.

- Minnesota legalises crypto custody for banks and credit unions: Local banks and credit unions will be authorised to provide digital asset custody starting 1 August, joining a growing list of states writing crypto custody into existing banking law. Paired with Trump’s executive order on Fed payment rails, the state framework is what makes federal access more than a theoretical step for community institutions.

- Hacker drains $11.58 million from Verus-Ethereum bridge: 1,625 ETH and 103.57 tBTC were taken in a single transaction, the third bridge-related loss of the week after THORChain and Echo. The pattern reinforced why integrators have been moving wrapped-asset and cross-chain flows toward Chainlink CCIP rather than continuing on the messaging layer that has carried the year’s largest exploits.

- SBI and Rakuten plan Japan crypto investment trusts: Both firms are preparing crypto investment trust products once the local regulatory path is finalised, with SBI targeting a $31.5 billion AUM run rate within three years. The pitch hangs on routing a slice of Japan’s roughly $14.8 trillion in household savings into regulated crypto wrappers, a much larger potential pool than the US retail base that drove the first ETF cycle.

- Italy’s largest bank doubles crypto holdings to $235 million: Intesa Sanpaolo grew its digital asset book from about $100 million to $235 million in the first quarter, more than doubling exposure in a single reporting period. The disclosure is one of the cleaner signals that European bank balance sheets are starting to carry direct crypto exposure rather than only client-facing services.

- Solayer launches Visa-compatible USDC card: The card lets users spend USDC balances at any standard Visa terminal, online or contactless, without converting back to fiat first. It is one of the cleaner examples of stablecoin issuers and DeFi projects using the existing card network instead of trying to replace it, the same pattern Tempo and Solana institutional flows are following.

- Spot Bitcoin ETFs bleed $1 billion in a week: The weekly redemption snapped a six-week consecutive inflow run, with a single-day outflow of about $635 million on May 13 ranking as the largest since January. The reversal landed exactly as Treasury yields surged, turning the ETF tape into a clear macro proxy rather than a standalone demand signal.

- Strategy puts Bitcoin sales on the table for bond repurchases: The firm plans to repurchase $1.5 billion of convertible notes and listed Bitcoin sale proceeds as one of the options to fund the buyback. It is the first time Saylor has formally named Bitcoin as a funding source for a corporate liability, a meaningful change to a treasury thesis built on one-way accumulation.

- Bitcoin tumbles below $79,000 as bond yields surge: The US 10-year Treasury yield ran to 4.59% intraday, the highest level in nearly a year, and Bitcoin lost its mid-week reclaim of $80,000 within hours. The move set the tone for the rest of the week as the 30-year yield then pushed to 5.18% and the macro discount rate became the dominant input.

- THORChain confirms $10.7 million cross-chain exploit: The protocol halted trading and rolled out a recovery portal after an attacker drained assets across nine chains, with early analysis pointing at the GG20 signature scheme as the likely failure point. The incident kicked off the week’s broader bridge security reset and accelerated the migration of wrapped-asset flows to Chainlink CCIP.

- Hana Bank acquires $670 million stake in Dunamu: The South Korean lender became the fourth-largest shareholder in the Upbit operator through one of the largest single bank investments into a crypto exchange to date. It cemented the pattern of Asian banks taking direct equity exposure to local crypto venues rather than only offering client services.

- Saudi Arabia secures $12.5 billion in tokenisation mandates: The droppRWA-led initiative is targeting real estate and other Saudi economic activity for on-chain issuance, framed as a wealth-protection layer against global shocks. The mandate size sits among the largest single tokenisation programmes disclosed by any sovereign entity this year.

- Lombard moves $4 billion in assets to Chainlink: Lombard joined the migration off LayerZero in the aftermath of the April KelpDAO incident, taking the total cross-chain flow displaced to Chainlink CCIP to roughly $4 billion. The move turned Chainlink’s bridge product into the default beneficiary of the broader cross-chain security reset.

- Bitcoin hits $82,000 as CLARITY Act advances: The market-structure bill cleared the Senate Banking Committee in a 15-9 vote and briefly pushed BTC to the cycle’s upper resistance band, while Coinbase led the listed crypto stocks higher. The print marked the week’s high before bond yields took the bid away the next session.

- Kevin Warsh confirmed as Federal Reserve Chair: Warsh was sworn in as Jerome Powell stepped down after eight years, taking the chair as the first Fed lead to personally own crypto and frame Bitcoin as the new gold for younger investors. The handoff sits inside a sharper macro setup as well, with the new chair inheriting a yield curve already pricing in policy uncertainty.

- Trump and Xi reach agreement on Strait of Hormuz: The leaders agreed in Beijing to keep the shipping lane open and paired the visit with a Chinese commitment to buy 200 Boeing aircraft. The geopolitical relief gave risk assets a small lift before the bond market took back any cushion later in the week.

- JPMorgan raises IBIT exposure by 174%: The bank lifted its spot Bitcoin ETF holdings 174% during the first quarter, well before the late-week ETF outflows. The disclosure is another step in the slow normalisation of large US banks holding spot Bitcoin exposure on their own books rather than just facilitating client trades.

- Kraken migrates kBTC to Chainlink CCIP: Kraken is moving its wrapped Bitcoin out of LayerZero in the aftermath of the KelpDAO and rsETH incidents, taking roughly $3 billion of cross-chain TVL with it. The decision turned the exchange into the most visible early mover in the wider migration to Chainlink CCIP that defined the rest of the week.

Bitcoin Market Analysis

Bitcoin came into the week with $80,000 reclaimed and CLARITY clearing committee. By the close, neither cushion was working. Price had touched about $82,000 on the legislative news, then drifted back through the round number as the 10-year Treasury yield climbed to 4.66% and the 30-year touched 5.18%, the strongest reading since 2007. The latest technical snapshot showed BTC near $77,601, with a one-week move of negative 2.21% and an intraday range of about $76,503 to $77,839. The breakout case did not survive contact with the bond market. The pullback case did not yet break the recovery.

Source: https://altfins.com/technical-analysis

The trend stack lost some of last week’s polish. Short-term trend was flipped back to Down, medium-term shifted to Neutral, and long-term stayed Neutral. MACD remained bearish, with the line still below its signal even as the histogram bars began to rise from the lows. Most short moving averages turned lower while the 30-day and 50-day SMAs and the 26-day and 50-day EMAs still pointed up. That mismatch describes the week well: enough damage to call this a real test, but not enough yet to declare the spring repair finished.

$75,000 is now the line the chart needs. The first listed support sat at $75,000, with $70,000 underneath, while resistance moved back down to $80,000 and then $85,000. The earlier $80,000 reclaim has flipped into the first resistance to clear, and the 200 SMA still sits in the $80,000 to $83,000 band that rejected price twice during the month. A daily close back above $80,000 would re-open the $83,000 to $85,000 zone. A loss of $75,000 would route the conversation toward the prior channel-down breakout area.

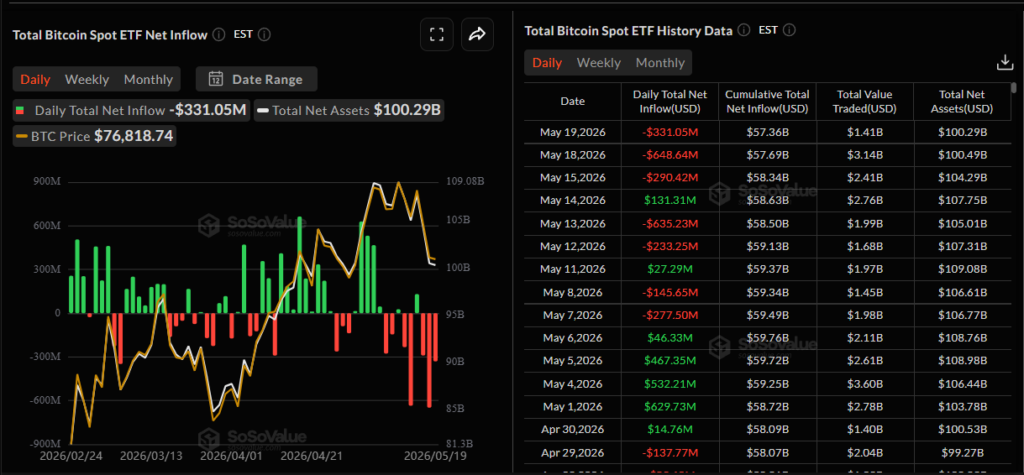

Source: https://sosovalue.com/assets/etf/us-btc-spot

ETF flows turned the macro story into a clear demand signal. The SoSoValue table showed about $331 million of net outflows on the latest day shown, with $648 million leaving the prior session and a $635 million single-day outflow on May 13 that ranked as the largest since January. Total net assets sat near $100.3 billion, down from above $107 billion only a week earlier, while cumulative net inflow held above $57 billion. Weekly aggregate outflows reached roughly $1.1 billion, the worst run in five months. Earlier first-quarter inflow weeks kept the cumulative line in positive territory. The pace of the latest redemption shows how quickly ETF demand can step back when yields move against risk assets.

Source: https://sosovalue.com/assets/etf/us-btc-spot

The corporate side answered with size. Strategy bought 24,869 BTC for about $2 billion, taking total holdings to 843,738 BTC at an average cost of $75,700, and Tether picked up SoftBank’s 26% stake in Twenty One Capital to push its own balance sheet further into the treasury and mining stack. The complication came from the same filing: Strategy now lists Bitcoin sale proceeds as one of the options to fund a $1.5 billion convertible-note repurchase. Conviction buying still anchors the bid. The treasury trade is no longer a one-way street, and the market now has to price the chance that a forced seller and a strategic buyer share the same balance sheet.

The political layer carried the better headlines. The CLARITY Act cleared the Senate Banking Committee 15-9 with Galaxy Research now putting the odds of an August signing at 75%, and Donald Trump signed an executive order directing the Fed to evaluate payment-rail access for Kraken, Ripple, Coinbase, and Circle. Bitcoin’s macro problem is short-dated. Its policy problem is being solved on a faster track than the prior cycle. The question for the next few weeks is whether $75,000 holds long enough for the structural story to catch up with the yield curve.

Ethereum Market Analysis

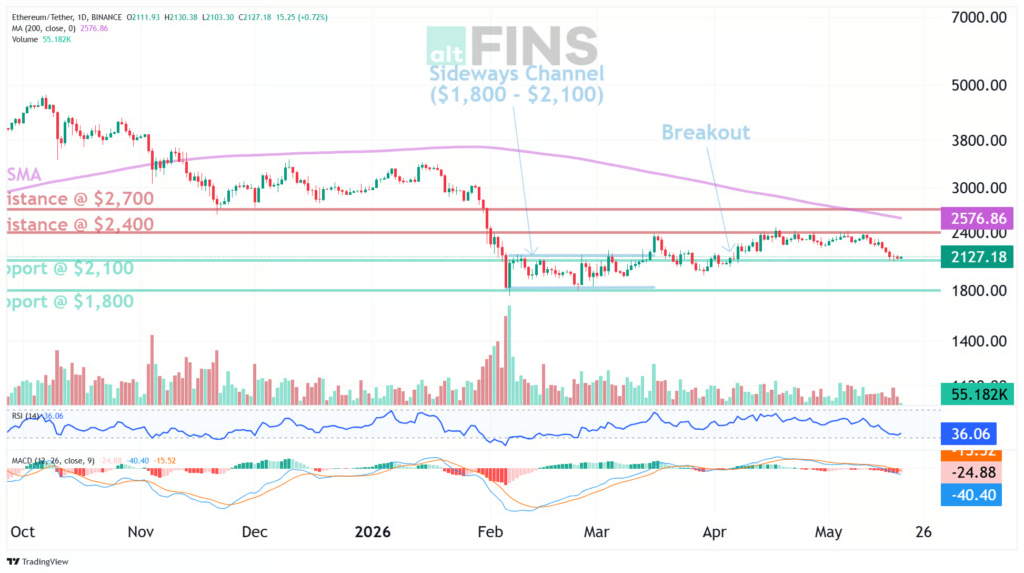

Ethereum did not have Bitcoin’s protection. ETH retreated to about $2,129 in the latest technical snapshot, down 5.72% over one week and 7.98% over one month, after the prior recovery had pushed price back into the $2,400 resistance band. The daily range ran from roughly $2,103 to $2,149, putting trade close to the lower Bollinger Band near $2,087 rather than the upper band near $2,432. Last week ETH was working on confirmation. This week it returned to defending the level that made the rebound credible in the first place.

Source: https://altfins.com/technical-analysis

The indicator set leaned softer than Bitcoin’s. Short-term trend was Strong Down, medium-term trend was Down, and long-term trend stayed Neutral. Stochastic, Stochastic RSI, CCI, and Williams readings were all oversold, while RSI stayed neutral. MACD remained bearish with the line still below its signal, although the histogram showed the same early inflection seen in Bitcoin. The setup is consistent with a stretched, exhausted seller move rather than a fresh breakdown. ETH can bounce from here without earning back its recovery.

$2,100 is the line that keeps the rebound alive. Support sat at $2,100 first, with $1,800 underneath, while resistance held at $2,400 and then $2,700. A close above $2,400 would re-open the $2,700 target and rebuild the breakout case. A loss of $2,100 would push price back into the range that had defined the winter drawdown and trigger the broader deleveraging move some traders have already started to warn about. The level matters because it sits exactly where last month’s swing-trade structure was built.

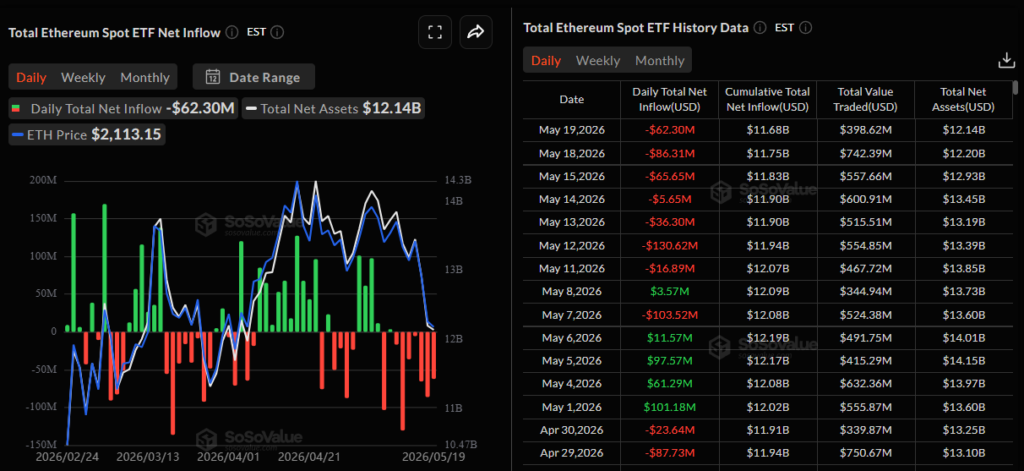

Source: https://sosovalue.com/assets/etf/us-eth-spot

ETF flows worked against the support test. The SoSoValue table showed about $62 million of net outflows on the latest day, with $86 million leaving the prior session and a $130 million outflow earlier in the week. Total net assets sat near $12.1 billion, down from above $13.4 billion only a week earlier. Cumulative net inflow held near $11.7 billion. Last week’s $98 million inflow read looked like the start of a healthier tape. This week erased that progress and left ETH carrying its own air at the same time BTC was losing the $80,000 line.

The structural story moved on regardless. NUVA launched with $19 billion of Figure-originated tokenised assets routed toward Ethereum DeFi, ETH still anchors 67% of the $38.3 billion tokenised real-world asset market, and Stripe-backed Tempo plugged into Morpho’s $7.5 billion lending engine for onchain credit. The protocol layer kept pulling new collateral and new payment flows toward Ethereum even as the chart looked tired.

The risk layer was less helpful. The Ethereum Foundation lost more high-profile researchers, Verus’s Ethereum bridge was drained for $11.58 million, and Aave only just restored WETH borrowing limits as the KelpDAO contagion eased. ETH needs $2,100 to hold before the price section catches up with the institutional layer. The institutional layer is not waiting for the chart to be ready.

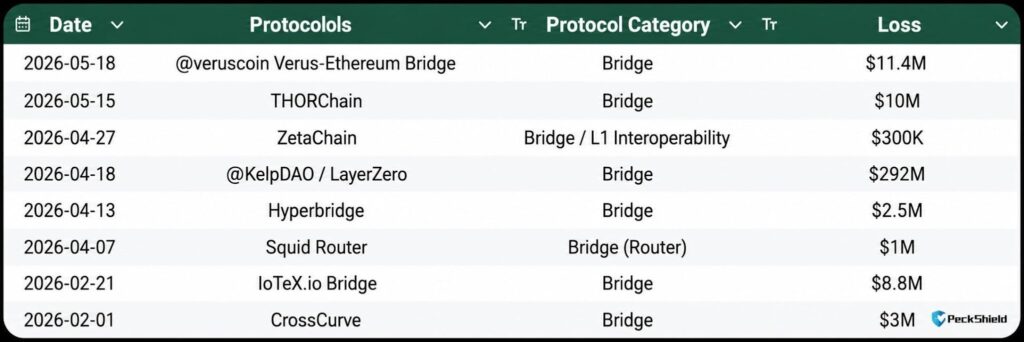

Bridge Security Forces a Chainlink Reset

The week’s quietest story was the loudest one underneath. THORChain halted trading after a multichain exploit drained roughly $10.7 million across nine chains. Echo Protocol on Monad lost $76 million in an unauthorised eBTC minting attack. The Verus-Ethereum bridge gave up $11.4 million in a single transaction. The KelpDAO and rsETH incident from April still rippled into Aave’s collateral parameters before being walked back. Four separate cross-chain venues, one bad stretch.

Source: https://news.bitcoin.com/crypto-bridge-exploits-328-million-may-2026-peckshield/

The market response was direct. Kraken announced it would move kBTC from LayerZero to Chainlink CCIP, and Lombard followed with $4 billion of assets, pushing the cumulative Chainlink CCIP migration above the same headline number. Bridges have been the soft middle of crypto infrastructure for years, but the price of running on weaker messaging is rising as wrapped-asset volumes scale. When a single bridge exploit can pull collateral parameters across half a dozen lending markets, integrators stop treating cross-chain choice as a vendor decision and start treating it as a risk policy.

The risk also extends past code. Hyperliquid, holding $176 billion in 30-day volume, drew formal scrutiny from CME and ICE this week as the established exchanges asked the CFTC to look at potential manipulation channels. Bankr was breached for $440,000 after a trust connection to Grok was misused. Bitcoin Depot, the largest US ATM operator, filed for bankruptcy after revenue fell 49.2%. Security stress is not staying inside DeFi. It is bleeding into onramps, AI-linked trading agents, and the listed venues that handle the size.

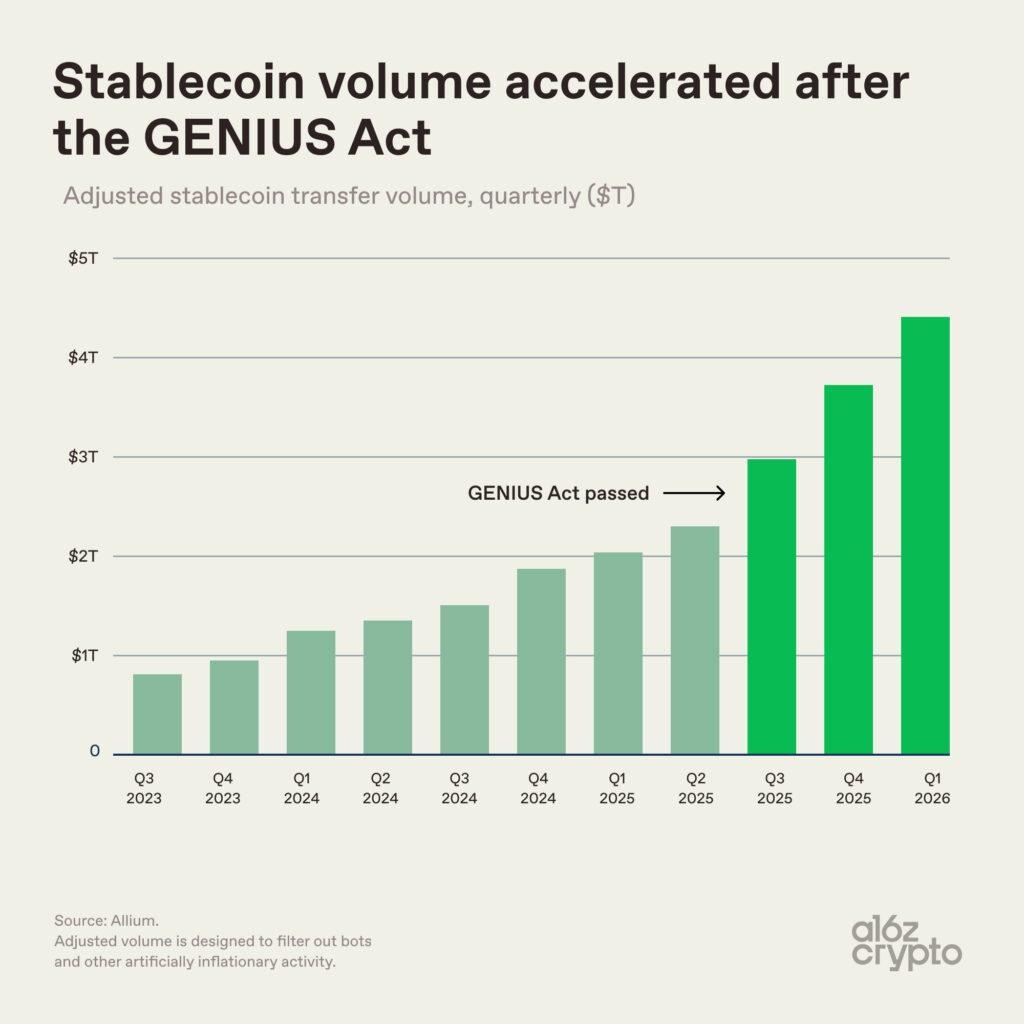

A New Dollar Rail Gets Federal Permission

The other quiet story was the one inside Trump’s executive order. The directive instructs the Federal Reserve to evaluate account access for digital asset firms including Kraken, Ripple, Coinbase, and Circle. Stablecoin issuers and exchanges have spent the cycle building around banks. The order opens the door to settling alongside them. Combined with Minnesota legalising crypto custody for banks and credit unions, Galaxy clearing the New York BitLicense, and Standard Chartered bringing Zodia Custody fully in-house, the regulatory direction looks less like accommodation and more like absorption.

Source: https://a16zcrypto.com/posts/article/stablecoin-data-charts/

The product layer kept moving in the same direction. Stripe-backed Tempo tapped Morpho to bring $7.5 billion of onchain lending into a payments-first stack. Solayer launched a Visa-compatible USDC card that lets stablecoin balances move through normal merchant rails. The Qivalis consortium expanded to 37 European lenders ahead of a euro-backed token launch later this year, and Tether’s T3 unit froze $450 million as part of its expanded compliance posture.

The signal sits at the intersection of those moves. Federal access, state custody rules, and bank ownership of crypto infrastructure are converging on a single picture: the next dollar rail is being built inside the regulated perimeter rather than outside it. Bitcoin and Ether traded the yield curve this week. The bigger fight, again, was over who gets to operate the pipes that move the dollars once they go on-chain.

Mark Your Calendars

Economic Data Releases:

- May 28, 2026 (Thursday): U.S. Q1 GDP second estimate, weekly jobless claims, pending home sales

- May 29, 2026 (Friday): U.S. PCE inflation, personal income and spending, Chicago PMI

Token Unlock

- May 22, 2026 (Friday): STRK scheduled unlock window listed by CoinMarketCal

- May 24, 2026 (Sunday): SOLV unlocks a major share of supply

- May 25, 2026 (Monday): ENA monthly unlock window

- May 28, 2026 (Thursday): SUI scheduled unlock window

- May 31, 2026 (Sunday): IO and APT scheduled monthly unlock windows