Ceasefire Relief, ETF Competition, and a Still-Fragile Tape

9th April 2026• 6 mins read

This Week’s Recap

- Crypto markets rally as Trump announces two-week Iran ceasefire: Digital assets jumped as geopolitical de-escalation improved risk appetite and forced roughly $600 million in short liquidations, making the ceasefire the clearest late-week catalyst for price recovery.

- Bitcoin breaks critical support as dollar and oil move together: Earlier in the week, Bitcoin lost key support near $68,000 and traded as low as $66,218 while oil and the dollar rallied, showing that macro stress still dominates when geopolitical risk surges.

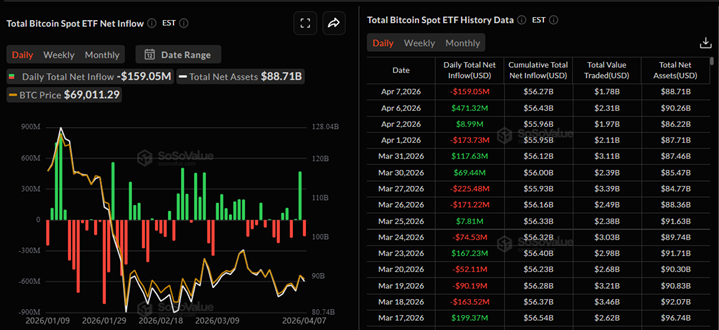

- Bitcoin ETF inflows hit highest level since February: Spot BTC ETFs pulled in $471.3 million on 6 April, a meaningful stabilisation signal after weaker prints, although that improvement was not sustained cleanly in the latest daily reading.

- Morgan Stanley’s bitcoin ETF opens today: Morgan Stanley launched a spot BTC ETF with a market-low 0.14% fee, turning the weekly story from simple ETF demand into ETF competition for institutional balance-sheet and wealth-platform flows.

- Coinbase wins initial bank regulator nod for trust charter: Coinbase’s conditional OCC approval reinforced the idea that the industry’s next growth lane is federally supervised custody and settlement infrastructure, not only retail trading volume.

- Strategy acquires 4,871 BTC and now holds 766,970 BTC: Strategy added again into a volatile tape, helping keep the corporate treasury bid alive while the market debated whether the war-driven selloff had already exhausted itself.

- Metaplanet acquires 5,075 BTC in single purchase: Metaplanet’s purchase pushed it above 40,000 BTC and reinforced that listed-company accumulation remains one of the strongest structural support stories underneath headline volatility.

- North Koreans hackers likely behind the roughly $285 million Drift Protocol exploit: The Drift incident stayed relevant all week because attribution, social-engineering mechanics, and laundering patterns pointed to a deeper operational-security problem than a one-off code failure.

- Solana Foundation unveils security overhaul: Solana’s STRIDE initiative was an immediate ecosystem response after reports variously sized the Drift exploit around $270 million to $286 million, and it underscored that large protocols now need permanent security operations, not only audits, to defend meaningful TVL.

- SEC crypto safe harbor heads to White House review: The proposal reaching White House review gave the market a constructive medium-term policy signal by suggesting a path for projects to decentralise without immediate enforcement pressure.

- SEC drops 30% of enforcement actions: The rollback of a significant share of prior cases added to the sense that US crypto oversight may be moving from blanket confrontation toward a more selective market-structure approach.

- US Treasury starts GENIUS Act rollout with notice of proposed rulemaking: Stablecoin policy moved deeper into formal rulemaking, keeping issuer regulation, licensing thresholds, and federal oversight at the centre of the payments-and-tokenization story.

- Ethereum Foundation doubles staked ether: The foundation reaching its 70,000 ETH staking target supported the institutional staking narrative, even as later treasury management headlines showed that Ethereum treasury behaviour is still pragmatic rather than purely directional.

- Aave contributors exit lending empire: Chaos Labs and BGD Labs winding down their involvement left Aave’s scale intact but reminded the market that governance, risk operations, and protocol staffing remain as important as headline TVL.

- Ethereum Foundation swaps 5,000 ETH for stablecoins: The sale was small relative to Ethereum’s overall market, but it mattered symbolically because it framed the foundation as an active balance-sheet manager during a fragile recovery.

- U.S. March jobs smash expectations, with 178,000 added: Stronger-than-expected labour data reinforced the higher-for-longer macro backdrop early in the week and helped explain why crypto remained sensitive to oil and dollar strength during the selloff.

- Charles Schwab opens waitlist for direct bitcoin and ether trading: The broader message from the Schwab-related trading rollout theme was that traditional brokerage distribution is still expanding, even while spot sentiment remains unstable.

- Circle unveils plans for wrapped bitcoin token cirBTC: Circle’s move added another institutional wrapper headline to the week and underscored how much infrastructure competition is moving toward custody, settlement, and tokenised collateral rails.

- Stablecoins flip automated clearing house volume in February: Stablecoin transaction volume overtaking ACH at the monthly level kept the payments narrative constructive even as speculative markets stayed dominated by macro and war-risk headlines.

- Bitcoin payments allowed for Hormuz tanker tolls: The report mattered less as immediate adoption proof than as a sign that geopolitical stress is beginning to pull crypto settlement ideas into real-world trade narratives.

- South Korea proposes bank-style stablecoin laws: South Korea’s draft framework reinforced the global push toward stricter stablecoin supervision and made it clearer that the next regulatory phase is about integration into bank-style controls.

- Stablecoin issuers get closer to US federal rules: The FDIC proposal added to the week’s steady march toward a formal US stablecoin rulebook, which is bullish for infrastructure clarity but likely more restrictive for weaker issuers.

- Citadel and Fidelity back EDX federal trust bank bid: EDX’s trust-bank push reinforced the view that regulated market structure, not only token price direction, remains one of the strongest long-run institutional themes in the asset class.

- RWA network Pharos lands $1 billion valuation: Pharos’ fundraise reinforced that regulated tokenization infrastructure is still attracting serious capital even in a headline-driven market week.

- Americans’ losses to crypto scams rose to over $11b: The FBI fraud figures were a reminder that user-protection failures still scale rapidly in bull and bear conditions alike, and that trust remains a major constraint on broader retail re-acceleration.

- Bitcoin options market pricing major downside: Options positioning kept a defensive tone even as spot rebounded, which fit the broader weekly pattern of tactical relief rather than a fully accepted bullish regime shift.

- Polymarket bags 97% of onchain prediction market fees: Polymarket’s dominance showed that crypto-native product-market fit still exists in selective verticals, even as broader DeFi yields and participation remain less convincing.

- Cardano targets Bitcoin liquidity with $80 million fund: The proposal reflected a wider cross-chain push to capture Bitcoin-linked liquidity and fees, turning BTC from a held asset into a strategic collateral pool for competing ecosystems.

- Standard Chartered looking to take over Zodia Custody: The deal discussion mattered because it pointed to continued bank appetite for plugging crypto custody directly into existing corporate and institutional distribution channels.

- Six Swiss banks launch digital franc sandbox: The Swiss sandbox added another data point supporting the thesis that tokenised cash and regulated onchain settlement are moving deeper into mainstream banking experimentation.

Bitcoin Market Analysis

Bitcoin finished near $71,072, up about 4.43% on the week, after recovering sharply from the early selloff that briefly dragged price below $68,000. The rebound improved the near-term tone, but the broader market still looks range-bound rather than fully repaired, with BTC trading back inside a larger $66,000 to $75,000 band. The latest daily session printed a high near $72,854 and a low near $70,464, leaving price close to the top of the recent range but still short of a decisive reclaim of $75,000.

Source: https://altfins.com/technical-analysis

Trend conditions improved, but not enough to call a clean bullish reset. Short-term momentum turned constructive, while the medium- and long-term backdrop still reflects the damage done during the prior breakdown. RSI held in neutral territory, MACD stayed supportive, and broader momentum readings leaned positive, which fits a market that is bouncing with force but has not yet rebuilt a stronger higher-timeframe structure. Volatility also remained elevated, with the Bollinger range running roughly from $65,047 to $72,296 and spot pressing the upper end of that band without yet breaking clearly beyond it.

The level structure is relatively straightforward. Support still clusters in the mid to high $60,000s, with the range floor around $66,000 and the lower-band area near $65,047 acting as the first meaningful retest zone if risk appetite weakens again. On the upside, the nearest friction line sits around $72,296, but the more important ceiling remains the $75,000 range high. In other words, Bitcoin has recovered to a stronger part of the chart, yet it is still trading below the level that would make the move look like a proper breakout instead of a relief rally.

Source: https://sosovalue.com/assets/etf/us-btc-spot

Price still needs confirmation through acceptance, not just through a squeeze-driven rebound. BTC has climbed back toward the top of its recent volatility band, but a market sitting just below resistance with higher-timeframe trend damage is still vulnerable to another failed reclaim. A durable move through $72,296 and then $75,000 would matter more than the rebound itself. If that follow-through fails, attention will quickly return to whether the mid-$60,000s can hold on the next downside test.

The first narrative layer is flow quality. Spot BTC ETF flows improved from an early-week drag to a much stronger 6 April rebound, but the latest daily print turned negative again, so the tape still reads as unstable rather than cleanly accumulative. That is why Morgan Stanley’s 0.14% spot Bitcoin ETF launch matters beyond the headline itself: it adds another institutional distribution channel, but it also intensifies fee competition at a moment when managers still need to prove they can retain and compound inflows.

The second narrative layer is balance-sheet sponsorship versus downside hedging. Strategy’s 4,871 BTC purchase and Metaplanet’s 5,075 BTC acquisition reinforced that listed-company demand is still one of the strongest structural supports under spot, but that support is offset by options market downside pricing and by Moody’s 28% haircut framework for Bitcoin-backed credit, which keeps liquidation mechanics relevant if macro stress returns. The result is a stronger market than the one seen at the start of the week, but not yet one with fully repaired conviction.

Ethereum Market Analysis

Ethereum finished near $2,190, up about 2.11% on the week, but the recovery remained less convincing than Bitcoin’s. ETH did join the late-week bounce, yet it still lagged in both price leadership and flow quality, which left the market treating the move as stabilisation after a prior downtrend rather than as a clear momentum reset.

Source: https://altfins.com/technical-analysis

Trend and momentum signals improved at the margin but remained mixed overall. The short-term move turned constructive, the medium-term backdrop looked more neutral than outright bearish, and the long-term structure still leaned clearly negative. RSI stayed neutral, MACD remained supportive, and ATR near $106.73 kept day-to-day risk meaningful relative to price. The Bollinger range ran roughly from $1,958.62 to $2,233.84, and the latest daily session printed a high near $2,270.71 and a low near $2,162.48, leaving ETH close to the top of its immediate volatility envelope without clearly escaping the broader recovery range.

Support and resistance are easier to map than conviction. The nearest support zone sits around $2,100 and then $1,800, while resistance is still defined by $2,400 and then $2,700. That matters because the market is still deciding whether the recent rebound is only a relief move inside a damaged structure or the start of something more durable. Holding above $2,100 is the minimum condition for stabilisation, but a cleaner constructive shift would still require ETH to work back through $2,400.

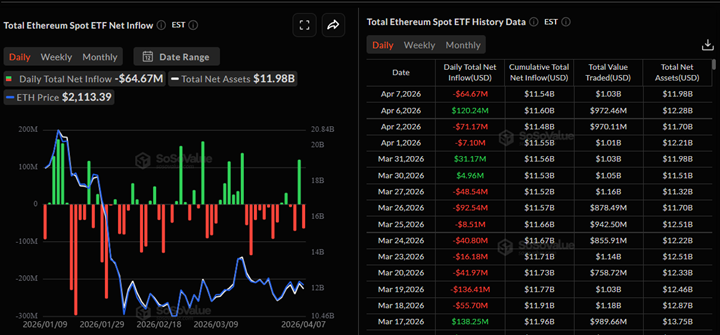

Source: https://sosovalue.com/assets/etf/us-eth-spot

ETH also remains more vulnerable to rejection than BTC because its recovery has not yet shifted the broader structure. Price is near the top of the immediate Bollinger envelope, but resistance at $2,400 still sits well above current trade, and the larger pattern is better described as stabilisation after damage than as a confirmed uptrend. If ETH loses $2,100 again, the market will quickly start debating whether the next meaningful test is back toward $1,800 rather than toward a fresh upside leg.

The first narrative layer is internal Ethereum sponsorship, but even that came with mixed signalling. The Ethereum Foundation reaching its 70,000 ETH staking target supported the idea that staking remains a core long-horizon commitment, while the foundation’s later 5,000 ETH swap into stablecoins reminded the market that treasury management is still pragmatic and operational rather than purely directional. That combination fits a market where strategic belief in Ethereum remains intact, but near-term cash management still matters.

The second narrative layer is ecosystem quality and competitive yield. Aave contributor exits kept governance and risk-operations concerns in focus, DeFi yields falling behind traditional savings rates limited the strength of the ETH-linked carry story, and the Drift exploit’s insider-risk framing kept security nerves elevated across the broader onchain complex. Taken together, those narrative inputs explain why ETH joined the ceasefire rebound but still did not convert it into the same quality of conviction that Bitcoin showed.

Institutional Rails and Fee Competition

Morgan Stanley’s 0.14% spot Bitcoin ETF launch matters because it turns the weekly ETF conversation from simple inflow direction into competitive market structure. In a tape where spot BTC ETF flows have rebounded sharply and then slipped again, pricing power becomes part of the macro narrative: lower fees are now being used to win distribution, defend incumbent share, and pull traditional wealth channels into closer competition. That means ETF demand can no longer be read as a single monolithic signal, because who gathers assets, at what price, and through which advisory network increasingly shapes the quality of the inflow story.

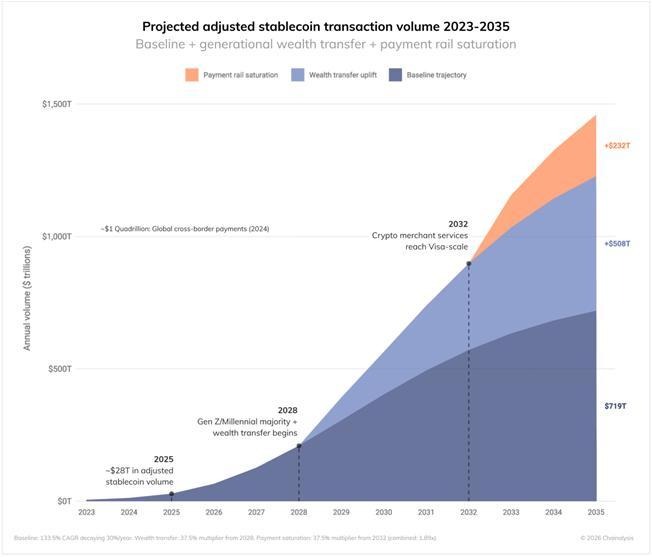

Source: https://www.chainalysis.com/blog/stablecoin-utility-future-of-payments/

The key point is that fee compression is usually a sign of market maturation, but it also raises the bar for what counts as constructive follow-through. If flows remain choppy, tighter pricing alone will not prove durable demand; it may simply intensify competition over a limited pool of near-term allocators. If, however, assets continue to gather even as pricing gets more aggressive, that would suggest that crypto exposure is becoming a standardised product inside broader institutional plumbing rather than a niche trade driven only by temporary enthusiasm. In that sense, the fee war is not just about margins. It is about whether Bitcoin wrappers are becoming normal financial infrastructure.

The same institutionalisation is visible in stablecoin rulemaking. US Treasury stablecoin policing proposals, South Korea’s bank-style stablecoin bill, and the Swiss franc stablecoin sandbox backed by major banks all point in the same direction: stablecoins are being pushed away from the lightly governed edge of crypto and toward supervised payment, settlement, and deposit-adjacent infrastructure. The significance of that shift is not only regulatory clarity. It is that policymakers and banks now appear to be designing for stablecoins as part of the financial system rather than treating them as a temporary experiment.

Custody and control layers reinforce that same read. Coinbase’s trust-charter progress and Standard Chartered’s interest in Zodia Custody suggest that the longer-cycle opportunity may sit less in new token narratives and more in the regulated scaffolding around them: custody, issuance, settlement, reporting, and bank-compatible access. Taken together, the ETF fee war and the stablecoin-bank rails story describe the same deeper transition. Crypto is still volatile and headline-sensitive at the asset level, but the underlying rails are being built to look more like mainstream financial infrastructure than a separate system.

Mark Your Calendars

Economic Data Releases:

- April 10, 2026 (Friday): CPI and Core CPI

- April 14, 2026 (Tuesday): PPI and Core PPI

Token Unlock

- April 12, 2026 (Sunday): Aptos (APT) unlocks US$10.58 M

- April 10, 2026 (Friday): Babylon (BABY) unlocks US$8.05 M