ETF Outflows, AI Rotation, Tokenization Progress

31th May 2026 • 12 mins read

Key Numbers:

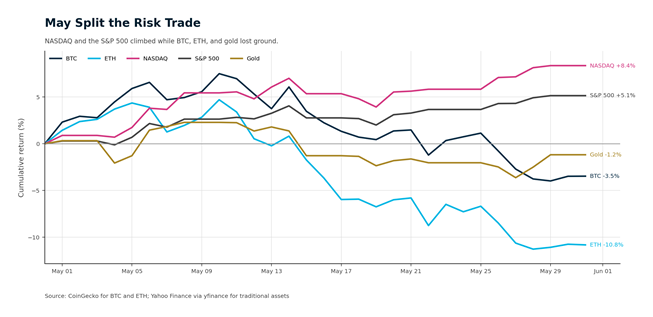

Bitcoin $73,762 (-3.47%) Ethereum $2,017 (-10.81%)

1-month return

Total Crypto Market Cap $2.55T (-4.9%)

2026 returns

Bitcoin –16.81% Ethereum –32.34% Gold 5.43%

NASDAQ 16.05% S&P500 10.73%

This Month’s Highlights

- Bitcoin closed May near $73,763, down 3.47% on a midnight AEST basis, after repeated failures around the $80,000 area left $70,000 as the support level June has to defend.

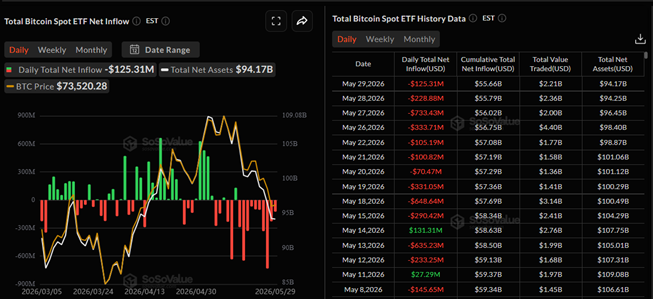

- Spot BTC ETFs lost about $2.8 billion during a record nine-day outflow streak. The wrapper worked; demand left.

- BlackRock’s IBIT absorbed a 29.2 million-share block trade worth about $1.3 billion without disorderly price damage, showing ETF depth even as sellers used that depth to exit.

- Ethereum fell 10.81% to roughly $2,018 despite Bitmine buying 111,942 ETH, Base launching AI-facing wallet and DeFi tooling, and Aave’s active loan book sitting near $10.9 billion.

- ETH lost the $2,100 area late in the month. Reclaiming that level comes first; $2,400 is where the market starts treating the recovery as more than repair.

- NASDAQ gained 8.36% and the S&P 500 rose 5.15%, leaving crypto behind the AI-led equity trade. The marginal dollar had an easier home in chips, data centers, cloud demand, and earnings revisions.

- Sticky inflation kept pressure on liquidity. April CPI rose 0.6% month over month and 3.8% year over year, while Fed minutes kept inflation risk near the center of the policy discussion.

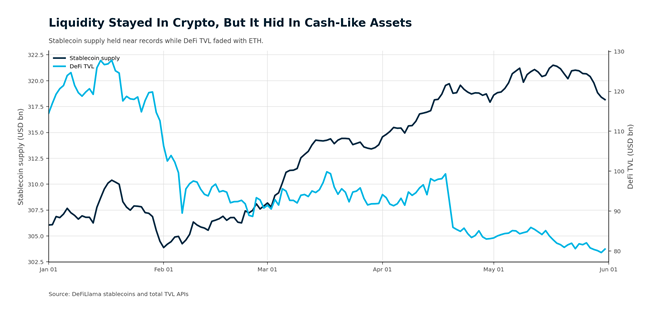

- Stablecoin supply held near $318 billion in DeFiLlama data, with broader late-month coverage pointing to a record-sized market near $322 billion. Cash stayed on crypto rails, but it did not rush back into BTC or ETH.

- DeFi TVL slipped from roughly $83.3 billion to $80.5 billion, a 3.36% decline. ETH fell nearly four times as much, so application liquidity held up better than token exposure.

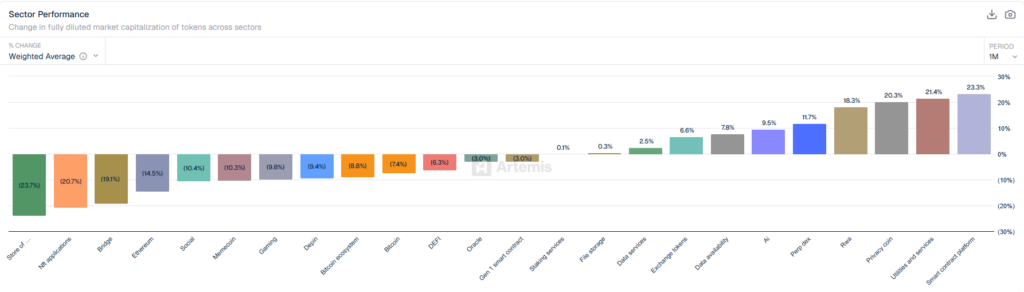

- Artemis sector data split hard: smart-contract-platform tokens rose 23.3%, utilities and services gained 21.4%, privacy rose 20.3%, and RWA gained 18.3%, while store-of-value tokens, NFTs, bridges, ETH, BTC, and DeFi finished on the weak side.

- A May 18 long-liquidation flush cleared about $563 million from bullish positions, and late-month options pressure kept Bitcoin pinned around the same zone where spot price was already struggling.

- BIS Project Agora moved toward real-value testing, while DTCC pushed tokenized securities closer to institutional market infrastructure and signaled plans to connect tokenized assets to Stellar in the first half of 2027.

Macro Watch

April inflation set the tone. CPI rose 0.6% in April and 3.8% over the year, according to the BLS release published May 12, while core CPI rose 0.4% on the month and 2.8% year over year. Energy carried much of the move. Crypto needed easier liquidity to offset ETF outflows, and the inflation data kept that relief out of reach.

The Fed’s April 28 to 29 meeting stayed relevant through May because the minutes kept policy anchored around inflation risk. The target range remained 3.50% to 3.75%, and the market had to weigh energy pressure, geopolitical risk, and the possibility that rate cuts would stay distant. AI equities absorbed that uncertainty through earnings momentum. Crypto had to absorb it through flows, and flows were going the wrong way.

PCE data near month end gave a softer but still uncomfortable signal. The BEA’s Personal Income and Outlays framework kept the Fed’s preferred inflation gauge in focus just as Bitcoin ETF outflows accelerated. Timing hurt. Crypto was losing its flow cushion while the macro calendar refused to give investors an all-clear.

The dollar and yield backdrop also kept stablecoin dry powder from becoming spot demand. Investors could wait inside cash-like crypto balances and retain optionality. That beats a forced exit, but it delays the rebound. June starts with jobs, CPI, PPI, PCE, and the FOMC all capable of changing the rate path. Crypto enters that sequence without much flow protection.

Regulatory Developments

U.S. policy work kept moving while price ignored it. Stablecoin and market-structure proposals gave the industry more to map against, especially around the SEC-CFTC boundary, reserve standards, issuer oversight, and stablecoin-yield compromises. The regulatory direction is more legible than it was a year ago. May showed the limit of clarity when redemptions are setting price.

The U.K. brought enforcement deeper into stablecoin routing. On May 26, the government announced sanctions targeting cryptocurrency exchanges and the A7 network, saying the network had been used by Russia to evade restrictions and channel funds tied to the war in Ukraine. Stablecoins are now payments infrastructure. Payments infrastructure gets supervised.

May’s regulatory direction was clear: more legitimacy, more rules, more enforcement. Tokenization projects moved closer to regulated wholesale rails, stablecoins moved closer to mainstream payments, and sanctions policy moved deeper into crypto routing. Serious institutions benefit from clearer boundaries. Loosely supervised activity loses space.

May’s Cross-Asset Rotation

Investors still wanted risk in May. They wanted it with earnings momentum attached. NASDAQ gained 8.36% and the S&P 500 rose 5.15%; Bitcoin lost 3.47% and Ethereum dropped 10.81%. The bid went to growth, liquidity, and index weight. Crypto beta sat outside it.

AI equities had the easier case: chips, data centers, cloud demand, and earnings revisions. Crypto had ETF redemptions, fragile support levels, and a token market still repairing from the earlier-year drawdown. Gold also slipped, so this was not a defensive rotation. Capital stayed in motion. It narrowed its preference.

May revealed more than another synchronized selloff would have. When everything falls together, crypto can blame macro and wait for relief. This time, the market kept rewarding parts of risk while crypto sat outside the winning group. Infrastructure progress helped the long-term case, but the month paid for demand, momentum, and earnings visibility.

Bitcoin Market Analysis

Bitcoin opened May near $76,411 and closed near $73,763 on a midnight AEST basis. The monthly loss was mild on paper, but the damage underneath was clearer. Early strength kept the April rebound alive, then ETF flows turned and the push toward $80,000 faded. By late May, the old breakout zone had become overhead supply. June begins with Bitcoin closer to a support test than a momentum chase.

Source: altFINS / TradingView

Bitcoin spent the month trying to turn $75,000 into a floor. It failed late. Support now sits around $70,000, while the first serious resistance band remains near $80,000 and then $85,000. Repeated rejection near $80,000 gave sellers a simple reference point, and the 200-day average sat close enough to that zone to make every reclaim attempt heavier. A daily close back above $80,000 would change the tone. Until then, rebounds still look like repairs.

ETF flows turned the month. May began with investors still willing to talk about April’s inflow recovery, then the second half flipped. CoinDesk reported that spot Bitcoin ETFs lost more than $2.26 billion over two weeks, then extended into a record nine-day outflow streak by May 29. Roughly $2.8 billion left the category. Price already had the bearish narrative it needed: the marginal buyer stepped back in public.

Source: https://sosovalue.com/assets/etf/us-btc-spot

BlackRock’s IBIT kept the ETF market credible. The fund absorbed a 29.2 million-share block trade worth about $1.3 billion without disorderly price damage. Liquidity made the exit smoother; it could not manufacture demand.

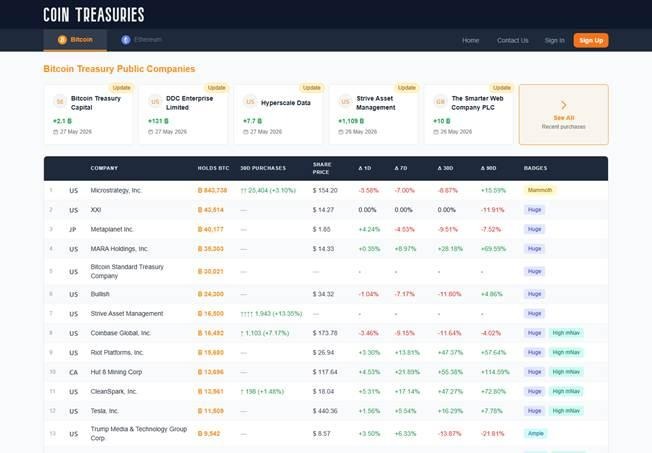

Corporate treasury activity kept a bid under Bitcoin, and the category became messier. Strive bought 1,109 BTC, taking reported holdings to 16,500 BTC, and SpaceX’s IPO process surfaced 18,712 BTC on its balance sheet. Trump Media pulled the other direction after a wallet linked to the company moved 2,650 BTC to Crypto.com. Treasury buyers remain part of the market. May made the category feel more like balance-sheet management than automatic accumulation.

Source: https://cointreasuries.net/

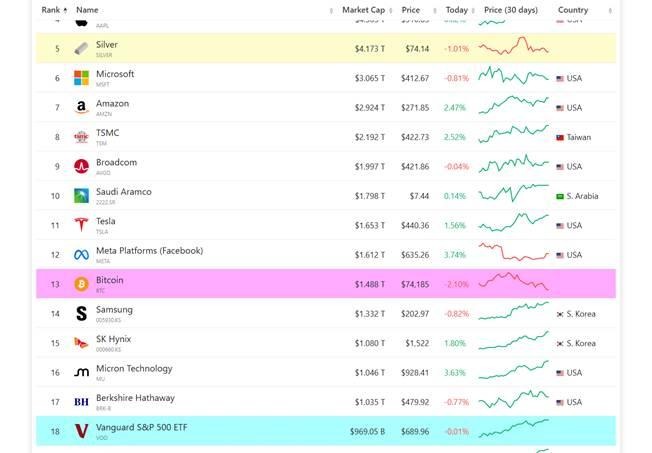

Bitcoin also lost the attention contest. BTC slipped to the 13th largest global asset as AI and semiconductor names climbed the market-cap table. ETF access used to be a major differentiator for institutional capital. In May, access was table stakes. The asset needed inflows and a reclaimed $80,000 level. It had neither.

Ethereum Market Analysis

Ethereum had a better month on the product side than the token showed. Base pushed AI-facing wallet and DeFi tooling, Aave’s loan book stayed large, and Bitmine bought into weakness. ETH still fell 10.81% to roughly $2,018. The network gave investors usable material. The token failed to convert it.

Source: altFINS / TradingView

Price carried the other side of the argument. ETH lost the $2,100 area late in the month and closed near the $2,000 handle, with $1,800 sitting as the next major support zone from the May technical work. Resistance remained at $2,400 and $2,700. The recovery path is wide. Reclaiming $2,100 would reduce the immediate damage, but leadership returns only if ETH can force the market to talk about $2,400 again.

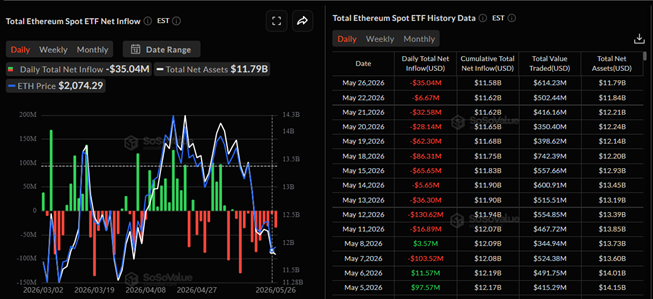

ETF flows gave Ethereum little help. The late-May SoSoValue snapshot showed daily ETH ETF redemptions while total net assets drifted toward the $12 billion area. Cumulative inflow remained positive, but ETH still lacks the depth and reflexive institutional bid that Bitcoin gets from its larger ETF base. For an asset already down more than 30% year to date, smaller passive demand left price exposed when spot buyers stepped away.

Source: https://sosovalue.com/assets/etf/us-eth-spot

Bitmine gave Ethereum its clearest balance-sheet headline. The firm bought 111,942 ETH worth about $237 million during the pullback, its largest ETH acquisition of 2026 by volume. The muted price response said more than the purchase. One treasury buyer can soften pressure; it cannot replace ETF persistence, broad spot demand, and macro support.

Usage gave Ethereum the better argument. Base launched an AI-facing MCP tool that lets AI clients prepare wallet and DeFi actions through natural language, while Aave’s active loan book reached about $10.9 billion. Ethereum-adjacent infrastructure keeps moving closer to financial software. May’s market refused to pay for that distinction. ETH traded like beta.

Privacy became the roadmap issue to watch. Developers face a 12-month push for native privacy while privacy-first assets pull investor attention. Ethereum needs user-level confidentiality that can sit beside regulated access, wallet controls, and institutional compliance. The product path still has weight. The price path needs proof.

AI Took The Marginal Dollar

Bitcoin lost May to a competing growth trade as much as to crypto-specific selling. AI and semiconductor equities pulled money into liquid, familiar public-market structures while Bitcoin defended support and Ethereum tried to explain why product progress was not helping price. NASDAQ rose 8.36%, the S&P 500 gained 5.15%, BTC fell 3.47%, and ETH dropped 10.81%.

Source: https://companiesmarketcap.com/assets-by-market-cap/

AI had the cleaner case. Investors could point to data centers, chips, cloud demand, capex cycles, index weight, and earnings revisions. Bitcoin investors had a deeper ETF market, but that market was bleeding. Ethereum investors had real application work, but ETH was losing $2,100. In a month with sticky inflation and no policy all-clear, capital rewarded the trade that needed the fewest explanations.

AI also had a cleaner feedback loop. Strong semiconductor performance can feed index buying, options activity, and analyst upgrades. Bitcoin’s loop ran in reverse: price weakness fed ETF redemptions, redemptions added pressure, and allocators waited for a better entry. Ethereum had an even harder task because its best news lived in product development, not immediate token demand.

The marginal dollar chose momentum it could defend in a committee meeting. Crypto’s improvements were slower and more structural. Price action won.

Tokenization Moved Into The Plumbing

BIS Project Agora gave May its strongest non-price development. The project said tokenized central bank reserves and tokenized commercial bank deposits could support atomic cross-border settlement, and it will move toward real-value transactions. The work sits in wholesale payments, which gives it weight. Banks and central banks are trying to reduce settlement friction.

DTCC pushed the same direction from the securities side. In May commentary, DTCC described tokenization as a move from theory toward operational market infrastructure, with institutional risk controls, settlement certainty, and legal frameworks at the center. CoinDesk also reported that DTCC plans to connect tokenized securities to Stellar in the first half of 2027. The institutional version of crypto keeps moving closer to regulated rails.

Stablecoins moved along the same track. Block began a phased Cash App stablecoin rollout to part of its nearly 60 million-user base, while stablecoin supply hovered around record levels. Dollar tokens are becoming ordinary enough for consumer payment apps and important enough for regulators to treat them as payments infrastructure.

The common thread was settlement. Bitcoin’s May centered on investment demand, Ethereum’s on application activity, and tokenization’s on money and assets moving with fewer handoffs. That kind of adoption rarely creates an immediate token bid. It raises the floor under crypto’s relevance by pulling banks, market utilities, payment companies, and central banks into the same infrastructure conversation.

Stablecoins deserve more attention than their price stability suggests. A record-sized stablecoin market is cash parked on crypto rails. In May, that cash stayed parked instead of rushing into BTC or ETH. The market felt weak, with funds still close enough to move.

ETF Demand Cracked While The Wrapper Held

Bitcoin ETFs carried May’s clearest crypto-specific signal. The products processed large trades, maintained deep net assets, and handled heavy turnover. Flows still turned against the market. A strong wrapper cannot create a bid when holders use it to redeem exposure.

The late-month streak changed the tone around institutional demand. CoinDesk put the run at nine consecutive outflow days, with about $2.8 billion leaving spot BTC ETFs. April’s recovery flows had kept the bull case alive. By the final week of May, ETF redemptions were the first line on the risk sheet.

The IBIT block sale gave the month a cleaner test than daily flow totals alone. A $1.3 billion trade moved through the largest Bitcoin ETF without a disorderly break, proving that regulated wrappers can absorb institutional size. The plumbing worked. The order was still a sale.

ETF flows now operate as price discovery. Earlier cycles forced investors to infer institutional demand from futures basis, Coinbase premiums, or over-the-counter color. May put the answer on screen every day through creations, redemptions, and fund-level volume. That transparency is useful. It also makes weakness harder to ignore.

Bitcoin’s ETF base still leaves the asset in a better structural position than it had before U.S. spot products existed. Cumulative net inflows remain positive over the full cycle, daily turnover is large, and large blocks can clear. May drew the line between durable access and bullish demand. The market has the first. It needs the second back.

Sector Performance

Sector returns were brutally selective. Artemis weighted-average data ranged from -23.7% at the weakest end to +23.3% at the strongest. That spread is too wide for a simple broad-market drawdown. Capital left stale themes and chased live ones.

Source: Artemis Analytics

The worst returns clustered in store-of-value tokens (-23.7%), NFT applications (-20.7%), bridges (-19.1%), Ethereum (-14.5%), social (-10.4%), memecoin (-10.3%), gaming (-9.8%), DePIN (-9.4%), the Bitcoin ecosystem (-8.8%), Bitcoin (-7.4%), and DeFi (-6.3%). That mix includes speculative pockets and core crypto exposure. The market was cutting assets where the price story had gone stale or where earlier narratives lacked a fresh catalyst.

The winning side looked more specific. Smart-contract-platform tokens led at +23.3%, followed by utilities and services (+21.4%), privacy coin (+20.3%), RWA (+18.3%), perp DEX (+11.7%), AI (+9.5%), data availability (+7.8%), exchange tokens (+6.6%), and data services (+2.5%). RWA tied into tokenization, AI carried the broader equity-market tailwind, perp DEX benefited from derivatives activity, and privacy had a live product debate. Generic beta struggled. Specific themes had room.

Ethereum’s sector result made the split harder to ignore. ETH itself fell hard, yet smart-contract-platform tokens led the group. Programmable blockchains still had buyers. Ethereum’s May setup had weak ETF flow, fragile support, and spot price pinned near $2,000. Other smart-contract exposure could still work when momentum and narrative were cleaner.

Market Structure

Flows and leverage weakened market structure. Settlement held. CoinDesk reported about $563 million in long liquidations on May 18, the largest one-day bullish wipeout since February. Late-month options positioning added another pressure point, with reports around the May 29 expiry putting Bitcoin options notional near $6.2 billion to $6.3 billion and max pain around $75,000. That level sat right where spot price was already struggling.

Stablecoin balances held up better than price. DeFiLlama data cached for this report shows stablecoin supply near $318 billion at both the start and end of May, while broader market reporting put late-month stablecoin value near a record $322 billion. Capital shifted into cash-like assets and waited. Funds stayed close to the market, just unwilling to chase.

Source: DeFiLlama stablecoins and total TVL APIs

DeFi TVL moved from roughly $83.3 billion to $80.5 billion during May, a 3.36% decline. ETH fell nearly four times as much. Application liquidity was more stable than the token price implied, which fits the wider month: rails held up better than exposure to those rails.

Capital changed form rather than leaving the system outright. Stablecoin supply rose into mid-May and stayed elevated even as DeFi TVL drifted lower. Directional risk came down, collateral stayed available, and application liquidity softened without a deeper break. ETF flows and cooler macro data can repair that kind of air pocket quickly. Broken settlement would require a longer rebuild. May looked closer to an air pocket.

Wrap-up

May was a rotation month with a weak crypto finish. Bitcoin’s ETF wrapper passed a liquidity test, but ETF demand failed the direction test. Ethereum’s application layer kept producing real developments, while ETH traded like the market had enough beta already. Stablecoins stayed large, DeFi TVL held better than token prices, and tokenization advanced through BIS and DTCC. The structure held.

Crypto needs flows alongside infrastructure progress. AI equities had flows. Bitcoin had outflows. Ethereum had product news without price confirmation. Macro data kept the Fed cautious, and late-month leverage clears reminded traders that support levels can break quickly when positioning is crowded.

June starts with three live tests: Bitcoin reclaiming $80,000 or defending $70,000 cleanly, ETH recovering $2,100 before $2,400 matters again, and ETF flows finally stopping the bleed. Stablecoins give the market dry powder. May showed that dry powder can sit still when a cleaner trade is moving somewhere else.