Market Overview

January 2025 was shaped by both anticipation and reaction—first to Donald Trump’s upcoming inauguration, then to the immediate policy shifts following his return to office. Markets had surged in November and December after his election victory, with Bitcoin rallying past $90,000, but as the inauguration on January 20 approached, investors were waiting to see how his administration would act. His first days in office confirmed expectations of a pro-crypto agenda, with executive orders and regulatory changes aimed at reversing policies that had restricted the industry. One of the earliest moves came on January 23, when the administration rescinded Staff Accounting Bulletin No. 121, removing the requirement for financial institutions to classify crypto holdings as liabilities. This shift was reinforced by a U.S. Securities and Exchange Commission leadership overhaul.

Regulatory Developments

Central to this transformation was the resignation of longtime SEC Chairman Gary Gensler on January 20, 2025, a move that many in the industry had anticipated given his history of strict enforcement against crypto firms. In his place, President Trump appointed SEC Commissioner Mark Uyeda as acting chair, setting the stage for a shift in regulatory priorities. Uyeda, known for criticizing Gensler’s stringent approach, is expected to lead the SEC toward policies that encourage financial innovation and capital formation. To solidify this pro-crypto shift, Trump also nominated former SEC Commissioner Paul Atkins—a longtime advocate of reduced regulatory burdens—to serve as the permanent SEC chair, pending Senate confirmation. Meanwhile, the administration established a crypto council to guide policymakers on integrating digital assets into national economic strategies. Additionally, an SEC crypto task force, led by Commissioner Hester Peirce, was formed to craft a clearer, more comprehensive regulatory framework. The administration’s sweeping policy changes culminated in an executive order, signed on January 23, that not only expanded regulatory reforms but also initiated discussions on a national cryptocurrency stockpile while explicitly banning the issuance of central bank digital currencies.

Market Reactions

The market responded immediately and dynamically to these regulatory shifts. Bitcoin, for instance, experienced notable volatility throughout January. Beginning the month at approximately $95,301.81, Bitcoin’s price surged to a monthly high of around $109,225 before closing near $105,508.46 on January 31, 2025—a net increase of roughly 10.71%.

Source: altfins.com

Institutional accumulation played a significant role in sustaining this momentum. As of January 31, Bitcoin ETF holdings stood at approximately 1,167,762 BTC ($122.4B), with BlackRock’s iShares Bitcoin Trust leading at 579,304 BTC ($60.72B). Meanwhile, Ethereum ETF holdings totaled 3,641,897 ETH ($12.35B), with iShares Ethereum Trust holding 1,235,138 ETH ($4.19B). MicroStrategy also continued its aggressive Bitcoin strategy, increasing its total holdings to 471,107 BTC.

Source: Lookonchain

Zooming out, Bitcoin fund holdings experienced a massive increase over the past year, reflecting a growing institutional presence. On January 31, 2024, total Bitcoin fund holdings stood at 714,215 BTC ($30.39B). By January 31, 2025, these holdings surged to 1,205,640 BTC ($117.19B)—an increase of 491,425 BTC (or +68.8%) in just one year. This growth underscores a sustained accumulation trend among institutional investors, further supported by rising Bitcoin ETF inflows.

Source: https://cryptoquant.com/

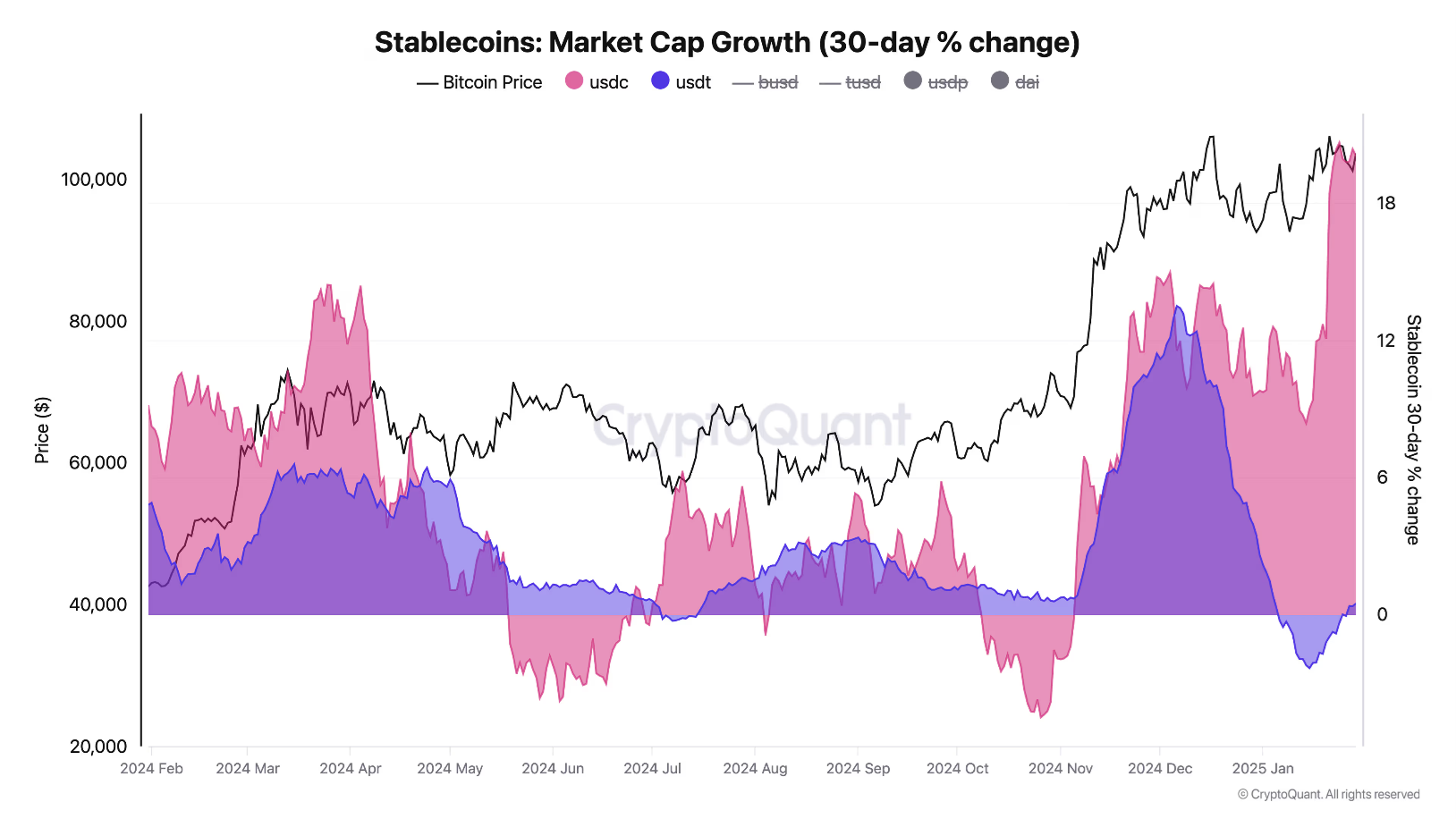

Stablecoin Liquidity Stablecoin liquidity further reinforced this trend, signaling fresh capital entering the crypto ecosystem. USDT’s market cap stood at $139 billion, while USDC’s supply reached $53.4 billion, contributing to a total stablecoin market capitalization of $204 billion, a $37 billion increase since November 2024 (CoinDesk). Historically, expansions in stablecoin liquidity have preceded major market rallies, as these assets act as “dry powder” for investors deploying capital into crypto markets. With a sharp rise in USDT and USDC market cap growth in December 2024 and January 2025 aligning with Bitcoin’s surge past $100,000. Similar trends were observed in early 2024 and 2021, where increases in stablecoin issuance fueled price expansions.

Moreover, the 30-day percentage change in stablecoin supply has mirrored Bitcoin’s movements, reinforcing its role as a liquidity driver. Beyond fueling market upswings, stablecoins also act as a liquidity buffer during volatility, enabling investors to rotate funds without fully exiting the crypto market. With stablecoin supply increasing alongside Bitcoin’s price surge, the data suggests that institutional and retail participants are positioning for continued upside, further strengthening the case for sustained accumulation.

Deepseek Effect

On January 27, 2025, Chinese AI startup DeepSeek unveiled its R1 model, developed at a reported cost of under $10 million. This announcement raised concerns about the competitive positioning of U.S. tech companies like Nvidia and Microsoft, leading to a significant sell-off in tech stocks. Nvidia’s stock experienced a record one-day decline of nearly 17%, erasing approximately $465 billion in market value.

Source: https://x.com/MarketWatchBot/

The cryptocurrency market mirrored this downturn, with Bitcoin’s price briefly falling below $100,000. The decline was attributed to a shift in broader market sentiment, as cryptocurrencies are often viewed as high-risk assets correlated with tech stocks. Concerns that more affordable AI models like DeepSeek’s R1 could diminish the demand for high-end computing hardware, which has implications for crypto mining and AI-driven crypto projects. This apprehension led to significant liquidations, with over $850 million in leveraged positions wiped out across the crypto market within 24 hours of the news.

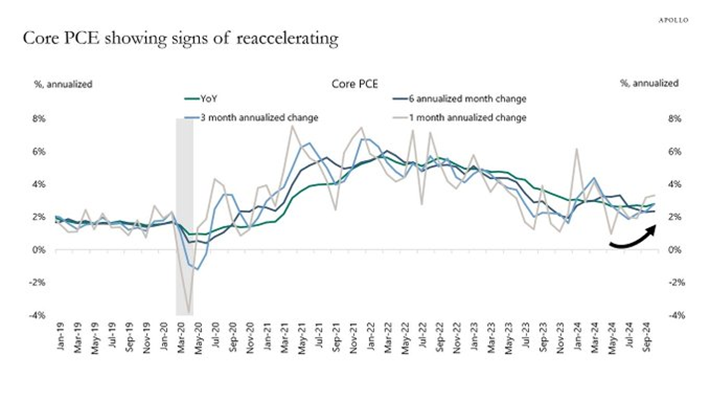

Macroeconomic Indicators The December 2024 inflation report, released on January 15, 2025, showed a year-over-year CPI increase of 2.9%, the highest since July, while Core CPI rose 3.2%, indicating persistent underlying inflationary pressures (BLS). The Personal Consumption Expenditures (PCE) price index, the Federal Reserve’s preferred inflation gauge, reported core inflation at 2.8% year-over-year, with a 0.2% monthly increase, aligning with expectations but reinforcing concerns over inflation’s resilience (Barron’s). Additionally, the U.S. GDP for Q4 2024 came in at 2.3%, driven primarily by declining inventories, reflecting a slowdown in economic momentum (Federal Reserve). Meanwhile, the December 2024 jobs report showed an increase of 256,000 jobs, keeping the unemployment rate steady at 4.1%, marking an acceleration from previous months (FT). While strong employment data signaled continued economic resilience, it also complicated expectations for rate cuts, as the Federal Reserve remained concerned about sustained wage pressures contributing to inflation.

Souce: https://x.com/KobeissiLetter/status/1882497793732104315

In response to these economic indicators, the Federal Reserve held interest rates steady on January 29, 2025, citing persistent inflation and robust consumer spending. Notably, the Fed removed previous language regarding inflation “making progress” toward the 2% target, signaling a less optimistic stance on disinflationary trends (Federal Reserve). The December FOMC minutes, released on January 8, suggested that policymakers viewed the current policy rate as close to neutral, indicating a cautious stance on rate cuts in the near term. This perspective was further supported by the GDPNow estimate for Q1 2025, which projected 2.9% growth, reinforcing expectations of steady economic expansion despite inflationary concerns (GDPNow). Collectively, this data presented a mixed macroeconomic outlook—while inflation remained elevated, employment strength and stable GDP growth provided the Fed with fewer incentives to pivot toward immediate monetary easing

Where are we Currently in this Cycle

Source: https://cryptoquant.com/

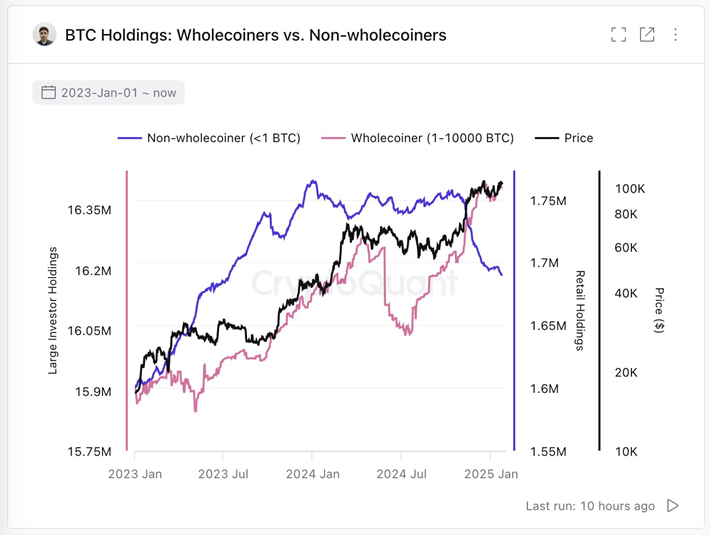

As the market digests these developments, Bitcoin’s on-chain data suggests that the cycle is entering an early distribution phase. Data from CryptoQuant shows that retail investors holding less than 1 BTC have started selling, while wholecoiners (1-10,000 BTC) continue to accumulate. This pattern differs from previous cycles, where large-scale Bitcoin distribution was primarily driven by whales offloading to retail. Instead, this cycle is seeing a more structured reallocation, with long-term retail holders and whales shifting Bitcoin into ETFs, institutional custody, and corporate treasuries. Ki Young Ju, CEO of CryptoQuant, notes that Trump’s pro-crypto stance and global influence could extend the cycle, keeping institutional demand strong and delaying the final phase of distribution—where retail and institutional investors fully absorb the remaining supply—until at least mid-to-late 2025. While macro uncertainty remains, Bitcoin’s increasing integration into institutional portfolios and stable liquidity conditions suggest that this cycle has yet to reach its final stages.

Ethereum

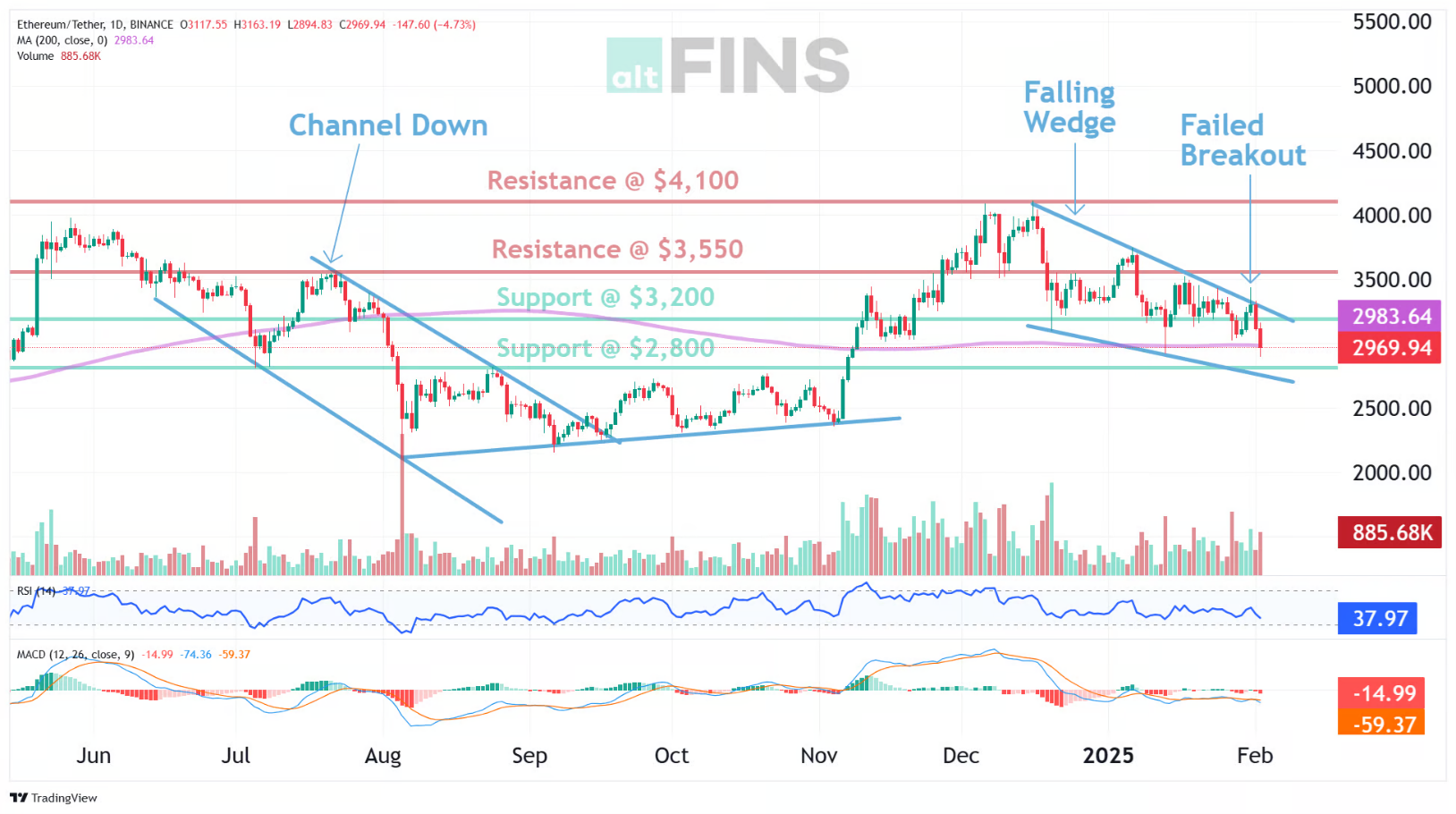

In January 2025, Ethereum’s price exhibited modest fluctuations. ETH commenced the month at approximately $3,400 and concluded around $3,431, reflecting a slight increase of about 0.7%. This performance was influenced by broader market dynamics and internal network developments. Notably, announcements from Ethereum co-founder Vitalik Buterin regarding plans to scale both Layer 1 and Layer 2 solutions introduced uncertainty among investors. These ambitious upgrades coincided with an unexpected increase in ETH supply, diverging from the anticipated post-Merge deflationary model. This shift dampened investor enthusiasm, leading to reduced whale activity and a more cautious outlook compared to the optimism observed in Bitcoin markets.

Source. https://altfins.com/technical-analysis Buterin’s January 2025 post outlined a long-term vision for Ethereum’s scalability, focusing on enhancing both Layer 1 and Layer 2 efficiency. He highlighted L2 adoption milestones, with networks securing billions in value and reducing transaction fees significantly. However, his proposal to increase the “blob” count for greater transaction capacity, alongside calls for L2s to allocate a portion of their fees to ETH through burning or staking, introduced mixed market reactions. While these initiatives aimed to reinforce ETH’s economic role within the ecosystem, they also raised concerns about potential shifts in Ethereum’s fee structures and supply dynamics. Additionally, Buterin emphasized improving interoperability to create a more seamless Ethereum experience, further positioning the network as a unified system rather than a fragmented collection of rollups. Despite the long-term benefits of these scaling plans, investors reacted cautiously, weighing the implications of technical changes and ETH supply adjustments amid existing market uncertainties.

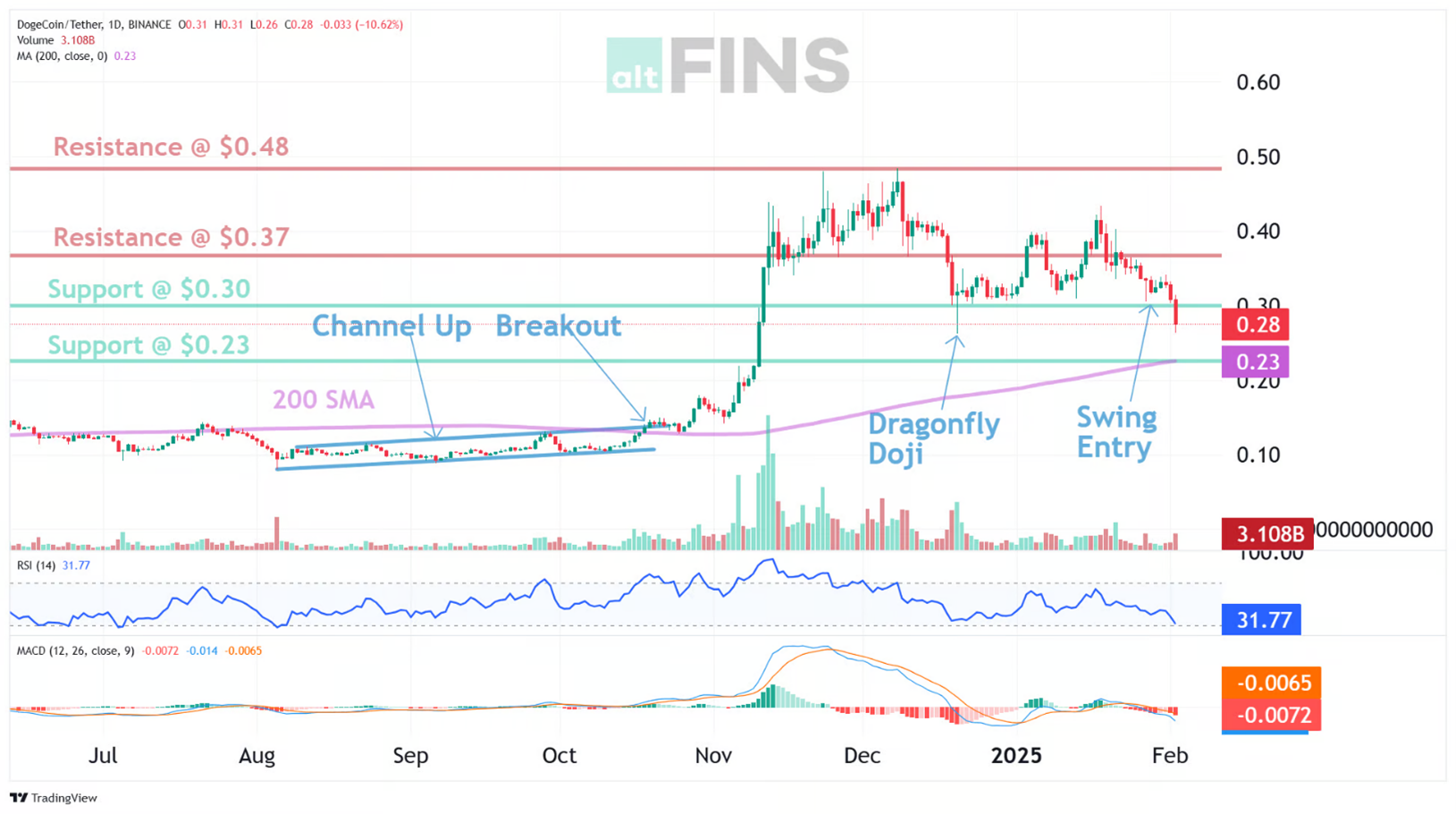

DOGE

In November 2024, President-elect Donald Trump appointed Elon Musk and Vivek Ramaswamy to lead the newly established Department of Government Efficiency (DOGE). This move was widely covered in the media, including by The Guardian. Following this announcement, Dogecoin (DOGE) experienced significant volatility. According to historical data from Yahoo Finance, between September 2024 and January 31, 2025, DOGE’s price fluctuated notably. Dogecoin’s unlimited supply and reliance on external factors, such as social media trends and public endorsements, continue to influence its market performance. These characteristics underscore the challenges faced by cryptocurrencies that lack intrinsic economic utility.

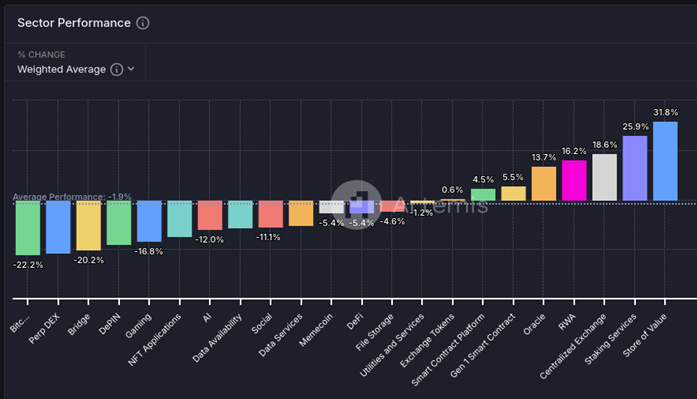

Sector Performance

Sector performance in the market varied significantly, with some sectors recording notable gains while others experienced declines. The Store of Value sector had the strongest performance, increasing 31.8%, followed by Staking Services, which rose 25.9%. The Centralized Exchange (CEX) sector gained 18.6%, while RWAs (Real-World Assets) and Oracles increased 16.2% and 13.7%, respectively. Smart Contract Platforms and Exchange Tokens also showed positive performance, rising 5.5% and 4.5%, respectively. These movements reflected capital flows into sectors linked to asset storage, staking incentives, and trading infrastructure.

The Bitcoin Ecosystem recorded the largest decline, falling -22.2%. Perp DEX tokens followed with a -21.3% decrease. Bridges (-20.2%), DePIN (-17.1%), and Gaming (-16.8%) also saw declines. AI tokens dropped -12.0%, while Data Availability (-11.7%) and Social (-11.0%) experienced similar losses.

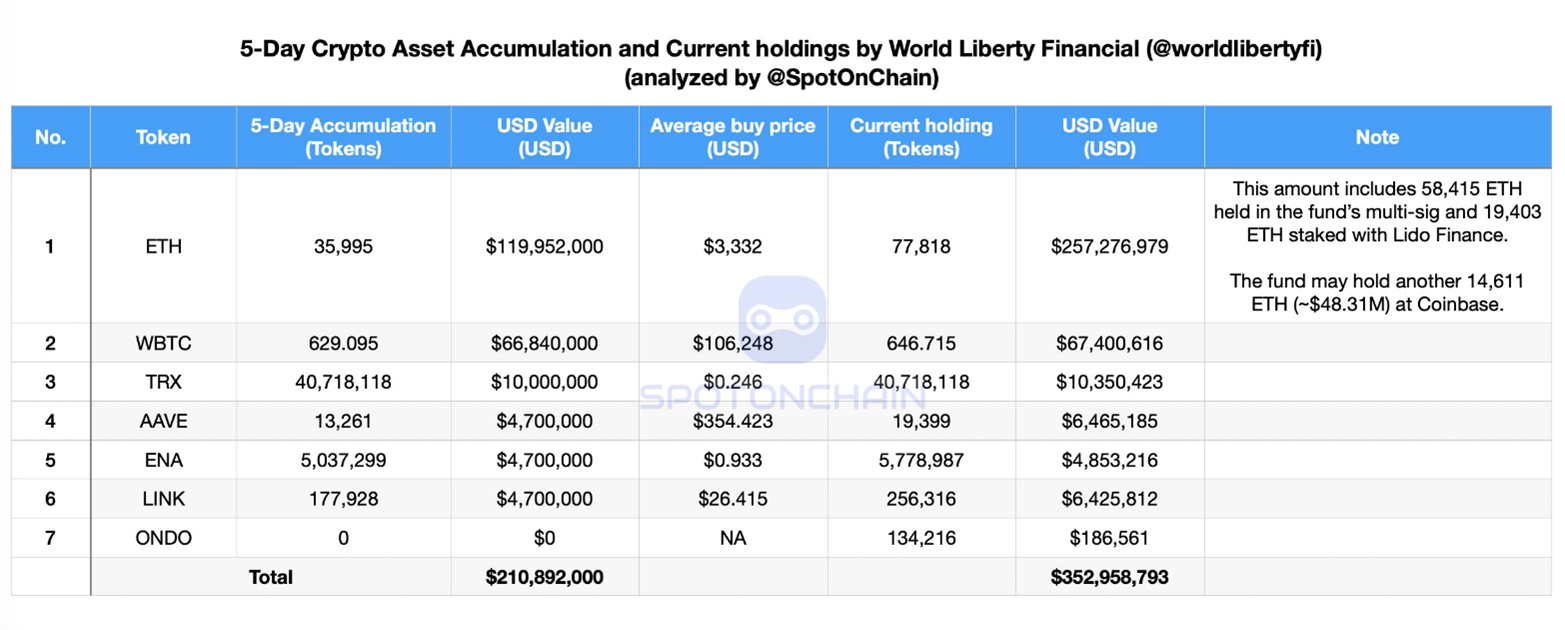

Other NewsWorld Liberty Financial (WLF) continued its aggressive accumulation strategy across multiple cryptocurrencies, significantly expanding its holdings in January 2025. The fund now holds approximately $352.96 million in digital assets, with Ethereum (ETH) remaining its largest position. WLF’s total ETH holdings stand at 77,818 ETH, valued at $257.28 million, including 58,415 ETH in its multi-signature wallets and 19,403 ETH staked with Lido Finance. The fund may also have an additional 14,611 ETH (~$48.31M) at Coinbase.

Source: https://x.com/spotonchain/status/1882949734211686885/photo/2

Beyond Ethereum, WLF has built sizable positions in Wrapped Bitcoin (WBTC), holding 646.715 WBTC worth $67.4 million, and Tron (TRX), with 40.72 million TRX valued at $10.35 million. Additional allocations include 19,399 AAVE ($6.47M), 5.78 million ENA ($4.85M), 256,316 LINK ($6.43M), and 134,216 ONDO ($186K).

Over the past five days, WLF has acquired approximately $210.89 million in new digital assets, demonstrating its continued expansion into the crypto market. Its growing portfolio highlights a strategic focus on major blockchain ecosystems, particularly Ethereum, Bitcoin, and DeFi-related assets.

Adding to the complex tapestry of events, the ongoing FTX bankruptcy repayment process—estimated between $14.7 billion and $16.5 billion—introduced another layer of market nuance. While some analysts speculated that the gradual return of capital to creditors could improve liquidity and sentiment, others pointed to historical precedents, such as the Mt. Gox repayment process, where the release of funds did not immediately lead to sustained bullish trends. Given the scale of repayments and the potential for recipients to liquidate assets, market participants remained cautious about the long-term impact on price stability (Reuters).

Wrap Up

Looking ahead, the developments of January 2025 are expected to have lasting implications for the cryptocurrency market. The administration’s regulatory actions and leadership changes at the SEC mark a shift in the U.S. approach to digital assets, with a focus on institutional participation and policy clarity. Bitcoin ETF holdings and stablecoin liquidity have expanded significantly, reflecting increased engagement from financial institutions. Market forecasts vary, with some analysts projecting higher valuations for Bitcoin, though future price movements will depend on capital flows and broader economic conditions. Ethereum’s performance will likely be influenced by the progress of its scalability upgrades and its continued role in decentralized finance (DeFi).

In summary, January 2025 was a period of significant change for the cryptocurrency industry. Regulatory adjustments, institutional investment trends, and macroeconomic conditions shaped market behavior. Bitcoin’s integration into investment portfolios, Ethereum’s technical developments, and the evolving policy environment remain key areas of focus moving forward. The industry will continue to adjust to these shifts, with regulatory decisions and institutional strategies playing a central role in determining long-term market dynamics.