ETFs Broaden Access, Macro Cuts Spark Volatility

31st October 2025 • 14 mins read

Key Numbers:

Bitcoin $110,109.7 (-2.66%) Ethereum $3,856 (-6.39%)

1-month return

Total Crypto Market Cap $3.71T (-6.08%)

2025 returns

Bitcoin 15.547% Ethereum 13.15% Gold +52.76%

NASDAQ 22.86% S&P500 16.29%

Key Takeaways

- Bitcoin set a new all-time high above $126,000 on October 6, then suffered a $19B derivatives liquidations on October 9 that slammed price to lows near $102,000 within days.

- Bitcoin finished October about 8.5% lower, breaking the six-year “Uptober” win streak as late rebounds failed to reclaim early-month peaks.

- The Federal Reserve cut rates by 25 bps to 3.75%–4.00% on October 29, and the cautious guidance triggered a sell-the-news reaction that kept BTC under pressure into month-end.

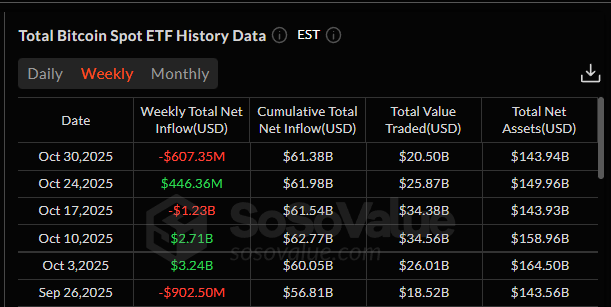

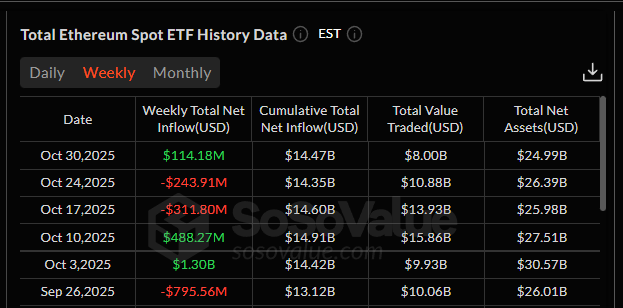

- U.S. spot BTC ETFs showed roughly $62.3 billion in cumulative net inflows with about 1.36 million BTC held, while spot ETH ETFs totaled about $14.75 billion and 6.75 million ETH, but the final week saw about $600 million in net outflows.

- BlackRock’s IBIT crossed 800,000 BTC in assets under management on October 9, underscoring the scale of onshore institutional ownership.

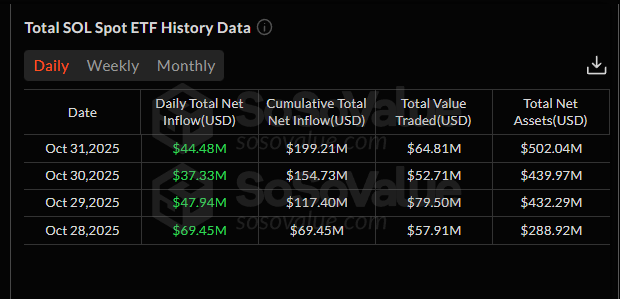

- Hong Kong approved the first spot Solana ETF on October 22 with trading from October 27, and U.S. venues listed Solana, Hedera, and Litecoin spot ETFs the same week despite the SEC’s shutdown-related delays.

- CME launched options on Solana and XRP futures on October 14–15, with inaugural trades from Wintermute, Galaxy, Cumberland, and Superstate, expanding listed hedging beyond BTC and ETH.

- Ethereum developers locked in the Fusaka upgrade for December 3, headlined by PeerDAS to lower rollup data costs, after completing the final Hoodi test on October 28.

- Options risk management took center stage as Deribit’s BTC options open interest hit a record near $50,000,000,000 and CME crypto options OI climbed to about $9,000,000,000 by October 23.

- An October 20 AWS outage disrupted multiple crypto services and some exchanges, elevating cloud concentration and multi-region redundancy as immediate operational risks for market participants.

- Into October 31, U.S. ETF demand turned negative and BTC hovered near $109,000 as Powell’s tone weighed on risk, while new SOL ETFs drew inflows but price lagged amid large on-chain transfers.

- Seasonality disappointed as mid-month drawdowns set up the worst “Uptober” since 2015, reminding investors that leverage and macro shocks can override historical patterns.

Market Overview

October was defined by a tug of war between inflow-powered optimism and macro-driven risk reduction, and that tug of war produced a choppy, net-negative month for investors. Bitcoin began the period with constructive momentum and supportive ETF flows, moved into a mid-month air pocket as crowded leverage unwound during what is now dubbed as “largest crypto liquidation in history”, and then finished the month with a sell-the-news reaction after the Federal Reserve cut rates but signaled that future decisions would depend on incoming data. Ethereum traced a similar arc with less durable follow-through on up days, in part because flows into Ether-focused funds were more tentative than flows into the dominant Bitcoin products, and in part because market participants preferred to carry exposure to the policy-sensitive asset with the most liquid onshore hedging tools.

Source: https://www.coinglass.com/today

The microstructure of the market amplified every macro headline and every turn in ETF demand. When creations were strong and basis was firm, price discovery favored the upside and intraday pullbacks were shallow. When daily redemptions emerged and funding cooled, ranges widened and bids thinned, especially around round numbers and time windows associated with primary market activity. This pattern is not new, but its magnitude increased during the month because a larger share of circulating supply now sits inside regulated wrappers that transmit real-time investor risk appetite into the underlying markets.

Leverage and options positioning shaped the path as much as spot flow. Open interest skewed heavy into the middle of the month and then reset abruptly during the liquidation cascade, which left the market cleaner but also more sensitive to incremental flow. The subsequent week was dominated by hedging around the Federal Reserve decision, and that hedging produced sharp intraday moves that did not always align with the direction of closing prices in related macro assets. The essential lesson for a low-risk sleeve is that the structure now provides deep, auditable pipes for capital, but those pipes can channel volatility just as efficiently as they channel demand.

Macro Market Analysis

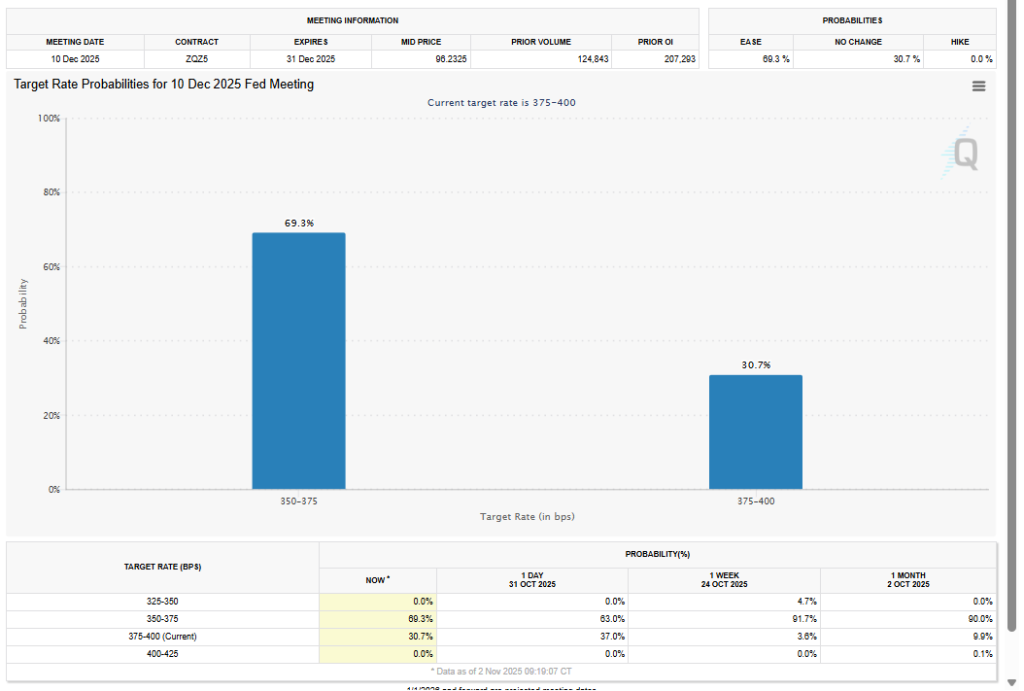

Policy expectations were the proximate driver of the late-month reversal that surprised investors who expected a smoother October. FOMC delivered a quarter-point cut that most desks had penciled in, but the communication emphasized vigilance and optionality rather than a firm glide path to additional easing. Markets had leaned into the meeting with a preference for a clearer dovish signal, so the combination of a cut and cautious guidance produced a fast repricing of forward rates and a sell-the-news pattern across risk assets, including Bitcoin and Ethereum. The reversal was sharper in crypto than in broad equities because open interest was higher relative to spot depth and because some participants had pre-positioned for a headline-driven extension, which left them vulnerable to a modest disappointment.

Current Implied Rate Cut Probabilities

Source: https://www.cmegroup.com/markets/interest-rates/

The global backdrop added cross-currents rather than clarity. Hints of trade de-escalation between the United States and China briefly boosted risk appetite and helped stabilize prices after the initial reaction to the Federal Reserve, but follow-through was limited by a firm dollar and by mixed messages from large-cap technology companies on capital spending. In this environment, crypto traded like a high-beta macro instrument most days, especially during United States hours when ETF primary and secondary market activity concentrated liquidity and volatility into narrow windows. The broad point for allocators is that monetary policy is easing from a high base, but the path of cuts is conditional, so flows will continue to swing with each data print that moves the probability of the next decision.

Operational fragility also mattered during the month, and it mattered in a way that does not show up in standard macro dashboards. A major cloud outage reminded everyone that many critical crypto services rely on centralized infrastructure, and that dependence can degrade user experience and execution quality during volatile markets. Exchanges and data providers that lacked multi-region redundancy saw service interruptions and latency spikes, which in turn widened spreads and reduced depth at the worst possible times.

Regulation and Institutional Participation

Regulatory developments pushed in two directions at once, and the net effect was to widen access while injecting timing noise into approvals and launches. In the United States, a federal government shutdown constrained agency capacity and delayed portions of the decision pipeline that affects ETPs and market-structure oversight. Issuers and listing venues adapted by sequencing filings and operational steps around the constraints, and the market still saw new spot funds for assets beyond Bitcoin and Ethereum make it to screens by month-end. This outcome confirms that regulated wrappers are now the primary distribution path for broad investor access, even when policy headlines are less than tidy.

Stablecoin policy moved from statute to early implementation in October, with the Federal Reserve’s Vice Chair for Supervision outlining how the new law will be applied to reserves and oversight in an October 16 speech, which emphasized highly liquid, itemized reserve assets and coordinated supervision. Industry signals in the same month pointed to execution, as Visa announced on October 30 that it would expand stablecoin support across additional blockchains, indicating that large payments incumbents are budgeting and building to distribute on-chain dollars at scale.

The Asia-Pacific region continued to act as an important test bed for regulated access. Hong Kong authorized a Solana spot ETF, which broadened the local menu beyond Bitcoin and Ethereum and demonstrated that product innovation is not confined to a single jurisdiction. Japan advanced discussions on bank-perimeter participation in digital assets, a signal that custody and trading services could migrate further inside institutions that already dominate capital markets in that time zone. These moves do not eliminate jurisdictional dispersion, but they do mean that liquidity and price discovery can shift across venues as specific products come online.

Source: https://sosovalue.com/assets/etf/us-sol-spot

Bitcoin Market Analysis

Bitcoin absorbed the month’s shifting flows with resilience early on and vulnerability late, and that pattern reflected the sequence from strong creations to heavy redemptions more than it reflected any change in long-term narratives. Bitcoin opened October at $113,114. on October 1 and closed at $110,109.7 on October 31, a decline of about 2.66 percent for the month. The early days of October saw robust demand from ETFs, firm basis, and persistent bids that nudged the asset to fresh highs, including a new record in the $125,400 to $125,689 zone on October 5, which kept realized volatility elevated but manageable. The mid-month liquidation that followed was abrupt and large in dollar terms, with October 17 printing an intraday range of roughly $5,690 from a high near $109,480 to a low near $103,790, which reset open interest to healthier levels while exposing how thin order books can become when funding sours quickly. The final week delivered the most difficult trading conditions for longs who had expected a dovish surprise from the Federal Reserve, because guidance stayed balanced and market structure was skewed toward forced de-risking, including a wide intraday swing on October 30 between about $111,612 and $106,377.

Source: https://altfins.com/technical-analysis

Ownership concentration inside regulated funds remains the structural headline for Bitcoin, and that concentration cuts both ways. The largest product crossed an eye-catching milestone in coins under management, and the complex as a whole held a meaningful fraction of circulating supply by month-end. That scale provides a durable base of demand on weak days, and it creates a clear, auditable mechanism for capital to enter the asset. It also creates a mechanism for tactical outflows to translate into supply that hits the market quickly when macro confidence falls, and that translation is most visible around the times of day when creations and redemptions drive dealer hedging.

Source: https://sosovalue.com/assets/etf/us-btc-spot

Derivatives continued to provide both risk and relief. Options open interest built into the middle of the month and then reset after the flush, which removed some of the gamma-driven accelerants that would otherwise have amplified every intraday move. Futures on regulated venues remained the preferred tool for institutions that require centralized clearing and transparent margining, and that preference helped concentrate liquidity in places where risk managers are comfortable. The combined picture points to a mature market that can accommodate very large flows without structural stress most days, but that can still experience sharp, mechanical moves when a crowded positioning regime collides with a macro surprise.

Ethereum Market Analysis

Ethereum progressed on fundamentals while trading like a higher beta reflection of Bitcoin and macro tone, and that contrast between technology momentum and price hesitation is important for patient allocators. Developers completed final rehearsals for the Fusaka hard fork and locked mainnet for December 3, with PeerDAS as the headline feature to cut data-availability costs for rollups and reduce node bandwidth, as confirmed on October 28 and October 30. October price action stayed choppy, with Ether setting a monthly high at 4,752.57 on October 7 and a monthly low at 3,471.22 on October 10, then closing October 31 at 3,856.99, which captured the shift from early resilience to late hesitation. The execution risk is not zero, but the public testnet cadence and the locked date give investors concrete milestones to track.

Flows into Ether-focused ETPs reflected that roadmap only modestly in October. U.S. spot ETH ETFs saw intermittent outflows around mid to late month, consistent with generalist capital waiting for post-upgrade data before adding exposure. That caution showed up on the tape, where Ether faded at round-number zones near 4,000 to 4,200 multiple times during October 14 to October 29, and where a macro headline shock on October 14 pushed Ether to 3,900.80 before a partial rebound.

Source: https://sosovalue.com/assets/etf/us-eth-spot

Derivatives provided both risk and relief. The largest intraday downswing occurred on October 10, when ETH traded a 4,393.63 to 3,471.22 range, a swing of about 922 dollars, alongside broad crypto liquidations later cited in market coverage. A late month sell-the-news move around the Federal Reserve communication on October 30 produced another wide range day, from 3,948.73 to 3,680.67, which reinforced why hedged core exposure outperformed unhedged longs during policy-sensitive weeks.

The medium-term case strengthened even as near-term price disappointed traders. If PeerDAS lowers and stabilizes data costs as designed, rollups can expand capacity and compress fees, improving consumer-grade experiences and pushing more on-chain activity over time.

Altcoin Market Analysis

Sector-level dispersion intensified around the ETP and derivatives headlines, and that dispersion created both opportunities and traps. Solana captured the month’s product spotlight in the United States and in Hong Kong, where spot funds offered regulated access and, in some cases, embedded staking policies that attracted attention from allocators who wanted yield inside a familiar wrapper. Early trading sessions produced respectable turnover and a visible broadening of the investor base, but price performance lagged during a week when macro flows overwhelmed asset specific optimism. The message is not that products failed, but that product innovation does not immunize assets from policy or positioning shocks.

Source: https://app.artemisanalytics.com

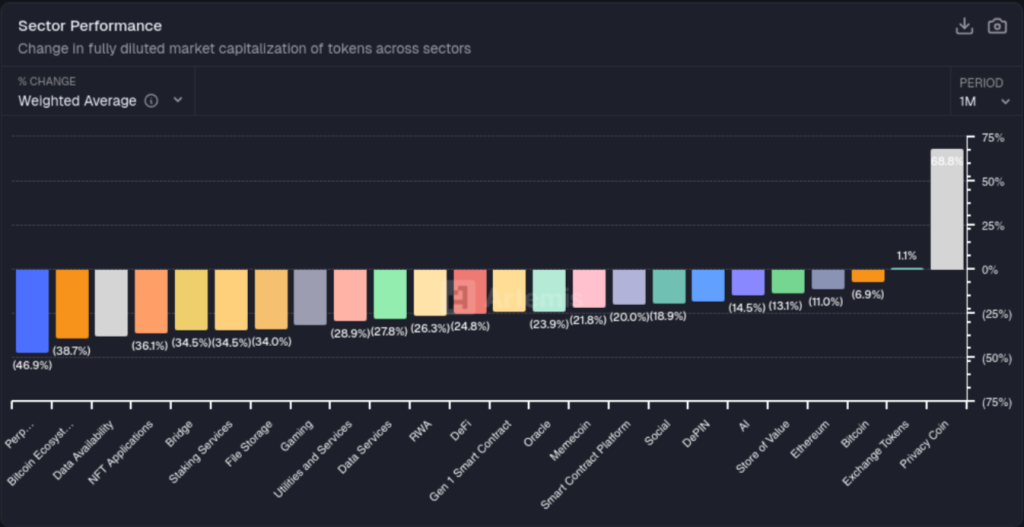

In October, returns were overwhelmingly negative, with only privacy coins solidly positive at about 68.8%. Most categories fell between 15% and 35%, including AI at about 13%, DePIN at about 14.5%, Social at about 18.9%, Oracles and smart contract platforms near 20% to 24%, DeFi at about 24.8%, RWA at about 26.3%, Data Services at about 27.8%, Gaming at about 28.9%, and File Storage, Staking Services, NFT Applications, and Bridges clustered around 34% to 36%. Ethereum sector performance was about 11% lower, the Bitcoin sector was about 6.9% lower, and several infrastructure cohorts such as Data Availability were down about 38%, with the weakest group close to 46.9%. The mix shows extreme dispersion, so product headlines and derivatives launches helped specific narratives, but macro pressure dominated breadth.

The derivatives stack expanded in a way that will matter for how volatility propagates across large caps. The launch of options on Solana and XRP futures at a major regulated crypto derivatives venue added listed hedging tools for assets that previously relied on offshore exchanges or bespoke over the counter structures. The first blocks crossed between well-known market making firms and asset managers, and open interest began to build in a pattern that suggests genuine hedging rather than just speculative punt and pray activity. This expansion makes it easier for funds to run diversified books with coherent risk management, and it creates pathways for cross asset hedging that can either dampen or concentrate volatility depending on positioning.

Stablecoins and payments provided a second axis of sector development that is more consequential over a multi-quarter horizon than it is over a single month. Visa said it will expand stablecoin settlement to additional coins and blockchains, extending support for USD and EUR stablecoins within its settlement platform, which ties global card networks to on-chain rails and signals production intent rather than pilots. Western Union announced USDPT, a dollar token to be issued by Anchorage Digital Bank on Solana, alongside a new Digital Asset Network, connecting a federally supervised issuer with a consumer distribution footprint that reaches more than 100 million customers; the company is targeting an initial launch window in 2026. The move reframed stablecoins as a complement to existing payment rails rather than an existential threat, and it shifted the conversation toward throughput, latency, cost, and compliance.

Narrative and Other News

Spot access widened, but the market rewarded real utility more than new wrappers. Uniswap added Solana support on October 15, letting users connect Solana wallets and swap SOL alongside Ethereum from one interface, which reduces cross chain friction and helps retail flow persist when macro turns choppy. Tokenization moved from pilot to plumbing as J.P. Morgan completed the first live private fund flow on Kinexys with Citco on October 30, a concrete step toward faster subscriptions and redemptions for alternatives. Banks clarified the wholesale roadmap when Citi argued for tokenized deposits as a better fit for large value payment.

Narrative rotation showed up in price and in treasury plans. A listed company, SharpLink, outlined a plan to deploy 200,000,000 dollars in ETH over multiple years on Linea using Anchorage custody with ether.fi and EigenLayer, reframing restaking as institutional treasury management rather than only DeFi carry. Privacy coins also drew attention mid month, led by Zcash, highlighting how regulatory tone can quickly redirect leadership even during weak breadth.

One caution still applies. New access and better hedging do not negate macro, options expiries can cluster and pin late in the month, and large scale tokenization or stablecoin plans still depend on operational resilience, which the October 20 AWS outage showed can be a single point of failure for the access layer. The practical takeaway is simple, use the broader toolkit and access, but size exposures with liquidity and operational constraints in mind.

Closing Insights

October offered a clear message to anyone running a low-risk,portfolio. The institutional rails that make allocation safer, more transparent, and more auditable are getting stronger, and those rails continued to improve during a month that disappointed momentum traders. ETFs accumulated meaningful inventory even as flow momentum reversed late in the period, listed derivatives deepened across more assets, and a major payments company introduced a plan that could drive real-world stablecoin usage at scale. Ethereum moved methodically toward a cost-reducing upgrade that can improve user experience on rollups and broaden the addressable market for applications, and Bitcoin continued to benefit from the scale and quality of its holder base even as it absorbed a sharp bout of de-risking.

None of these positives eliminated volatility or timing risk, and the end of the month proved that disciplined process beats confident prediction. The correct posture for November is to maintain a Bitcoin-anchored core, to keep a patient Ethereum sleeve through the upgrade window, and to use the growing menu of regulated instruments to control drawdown around known catalysts. The operative words are discipline, sizing, and telemetry. Add when basis is clean and flows are turning, trim into exuberance when creations run hot, and let the data around rollup costs and network throughput guide increases in Ether exposure rather than headline excitement. Respect macro as the master variable, but do not let it drown out the structural story that the plumbing is getting better and the distribution is getting broader. The market will continue to reward investors who can hold that dual view and who can execute a plan that pairs long-term conviction with short-term risk management.