Bitcoin Holds $109K Support, Ethereum Tests $4K Pivot

30th September 2025 • 12 mins read

Key Numbers:

Bitcoin $113,114 (3.95%) Ethereum $4,119.30 (-8.15%)

1-month return

Total Crypto Market Cap $3.95T (2.07%)

2025 returns

Bitcoin 18.69% Ethereum 20.87% Gold 47.34%

NASDAQ 17.34% S&P500 13.72%

Key Takeaways

- Early strength faded late in the month; bitcoin repeatedly held $109,000–$111,000 support, then closed September near $114,000; ether treated $4,000 as a pivot, briefly dipped below, then stabilised.

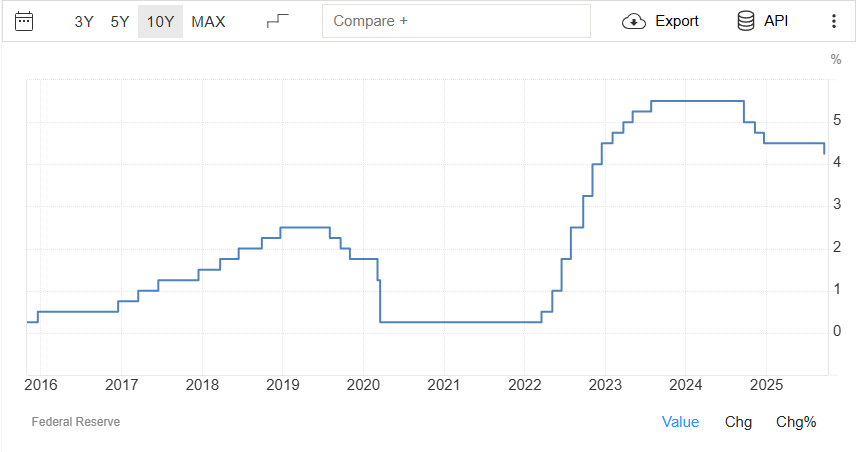

- On 17 September, the Fed cut 25 bps to 4.00–4.25 per cent; the SEP left room to ease further, although a faster disinflation trend was not evident.

- Activity clustered around 10–12, 17–19, and 24–27 September; liquidity thinned on down days, and options positioning amplified intraday swings.

- Strong mid-month ETF inflows supported tests of resistance; late-month outflows accelerated, including a combined draw approaching $700m on 25–26 September; a positive day on 29 September followed.

- Total crypto market capitalisation hovered in the high $3 trillions to low $4 trillions; the month-end snapshot was $3.95t, up 2.07 per cent for September.

- Gold gained roughly 11–12 per cent to near $3,871 per ounce by 30 September; firmer safe-haven demand and lower expected real yields competed for marginal risk capital.

- Listed options around large spot ETFs deepened; volatility and liquidity became more sensitive to a compact set of flows, hedging needs, and creation-redemption mechanics.

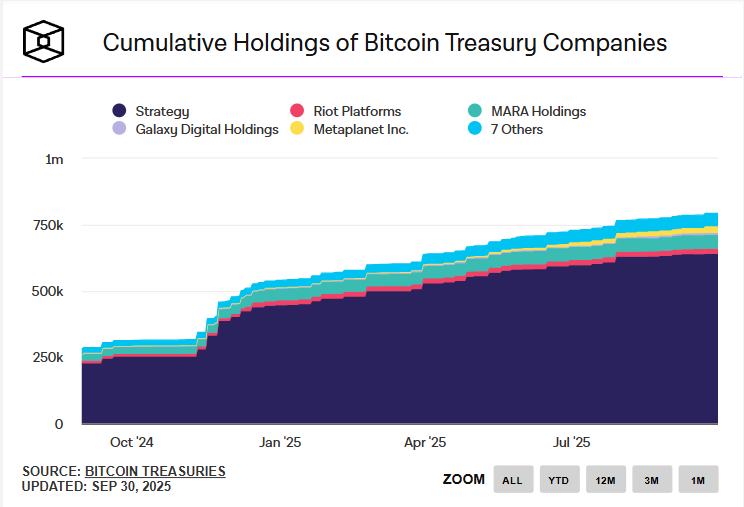

- Strategy Inc. added 1,046 BTC across two weekly disclosures; tracked corporate holdings exceeded 750,000 BTC by 29 September, supported by at-the-market funding programmes.

- “Safe DeFi” gained mindshare, favouring payments, simple savings, fully collateralised lending, synthetic assets, and basic exchange, with conservative risk tooling and oracle design.

- Payments-centric L1s (for example, Tempo; Plasma) prioritised bounded fees and predictable finality; Noble advanced USDC issuance for Cosmos.

- Liquidity linked the month’s moves; where rates, flows, and settlement rails supported depth and stability, price action was orderly; where they weakened, volatility returned quickly.

Market overview

September is commonly treated as a red month for risk assets, or at best a sideways grind. Multi-year seasonality in equities and bitcoin has skewed weaker in September, with average and median returns lagging other months. In 2025, that template was only partly observed. Bitcoin spent the first half of the month firm, then faded into the 24–27 September window as positioning de-risked, and the market faded into the 24–27 September window.

Total crypto market capitalisation, using widely followed composites, moved within a broad range that sat mostly in the high-$3 trillions to low-$4 trillions. Bitcoin and a handful of large caps held relative strength on up days; during down days, drawdowns broadened across mid-large caps, and intraday liquidity thinned around key levels as spot order books adjusted to flows from exchange-traded products, perpetual basis moves, and options hedging.

Volatility clustered around three windows: 10–12 September, 17–19 September, and 24–27 September. The first window carried into the pre-FOMC period, with traders leaning into rate-cut probabilities and constructive ETF flow expectations; the second overlapped the Federal Reserve’s decision on 17 September; the third coincided with a broader risk-off tone and mechanical deleveraging across futures. Open interest and options gamma profiles contributed to intraday swings. Late in the month, liquidity pockets appeared more fragile as several outflow days in spot exchange-traded products were recorded alongside price weakness.

Anchoring levels for the majors framed the month. Bitcoin began September close to $111,000, traded into the mid-$110,000s around 11–18 September, and tested the $109,000 area during 24–27 September before recovering intraday into 30 September. Ether opened near $4,300 on 1 September closes, pressed toward the mid-$4,000s around 17–18 September, then slipped below $4,000 on 25 September during a concentrated deleveraging episode before rebounding around that figure into the final days. Exact month-end closing prints for 30 September may vary across venues and index methodologies; where a specific figure is required, the last widely reported closing snapshot prior to publication has been used.

Momentum softened into the last week as positioning and flows turned defensive. The relationship between listed-product flows, derivatives hedging, and spot liquidity remained evident: persistent inflows or outflows across a few large exchange-traded vehicles can nudge market-making inventories, which in turn influences basis, funding, and options hedging. In September, this linkage was visible in the way strong mid-month inflows aligned with tests of higher resistance bands for bitcoin, then receded as outflow days accumulated into the last week and options skews reflected more demand for downside protection.

Macro setting: the policy decision and its context

On 17 September 2025, the Federal Reserve cut the target range for the federal funds rate by 25 basis points to 4.00–4.25 percent. It was the first reduction of the year after anticipated moves in April and June were deferred due to uncertainty around the inflation and growth effects of the Trump tariff package. The statement cited progress toward the 2 percent inflation goal, marginal labour-market cooling, and moderate growth. It balanced the risk of overtightening against policy lags, and noted that tariff pass-through, supply factors, and expectations would take time to filter through the economy.

Source: https://tradingeconomics.com/united-states/interest-rate

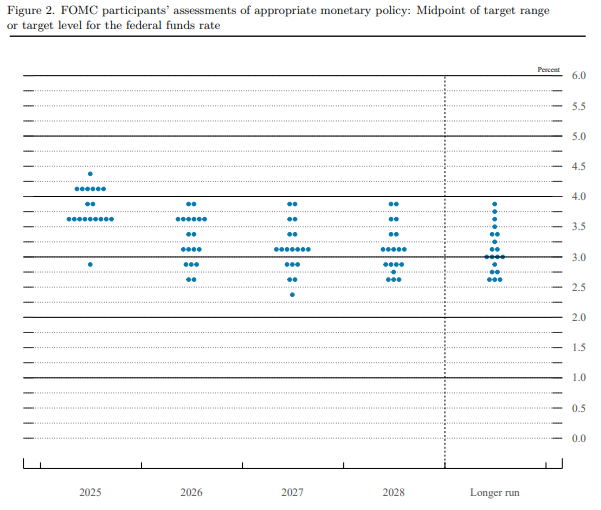

The Summary of Economic Projections on 17 September 2025 showed a median policy-rate path that left room to ease further, with the year-end 2025 median below the pre-meeting effective rate. In the dot-plot, 2025 projections clustered just under 4.0 percent, with a visible spread from roughly 3.0 to 4.5 percent, indicating non-trivial dispersion. For 2026, dots tightened around the low-to-mid 3s; for 2027 they centred near 3.0 percent, with a few outliers closer to 2.5 percent; for 2028 the cluster drifted a little lower, broadly in a 2.7 to 3.2 percent band. The longer-run dots sat mostly between about 2.5 and 3.5 percent, implying little change to longer-run estimates. Relative to the prior projection round, the central trajectory for 2025 appeared modestly lower, while the longer-run view changed little. As in previous cycles, participants emphasised data dependence; a clearer disinflation trend and continued labour-market rebalancing were presented as prerequisites for any acceleration in easing.

source: https://www.federalreserve.gov/

These macro signals interacted with crypto risk appetite through two channels. First, the rates impulse affected the discounting of long-duration risk and the carry environment for stablecoin yields and basis trades. Second, communication clarity, coupled with a perceived reduction in near-term policy uncertainty, coincided with a mid-month window of positive flows into US-listed spot products. Liquidity sensitivity remained elevated. Where a sequence of inflow days appeared, bitcoin pressed toward resistance in the mid-$110,000s; after decision day, flows turned mixed, and the late-month outflow run coincided with spot retracement and more defensive options skew.

Source: https://www.tradingview.com/

Gold held near all-time highs through September, rising about 11 to 12 percent for the month and printing a record intraday near $3,871 per ounce as shutdown worries and softer US labour data lifted Fed-cut odds; spot prices climbed from roughly $3,480 on 1 September to above $3,830 by 29 September, before touching fresh highs on the 30th. Against that backdrop, safe-haven demand and lower expected real yields remained the dominant drivers, with gold’s best monthly gain in over a decade as markets priced additional easing. ETF flow reports pointed to sizeable September inflows into the largest gold funds, reinforcing the bid. For crypto, the implication is a tighter competition for marginal risk capital when bullion sits at or near record levels, particularly if a firm US dollar and conservative equity tone persist; this dynamic likely contributed to choppier post-FOMC flows and a less supportive liquidity backdrop for beta assets.

Bitcoin: price action and listed-product flows

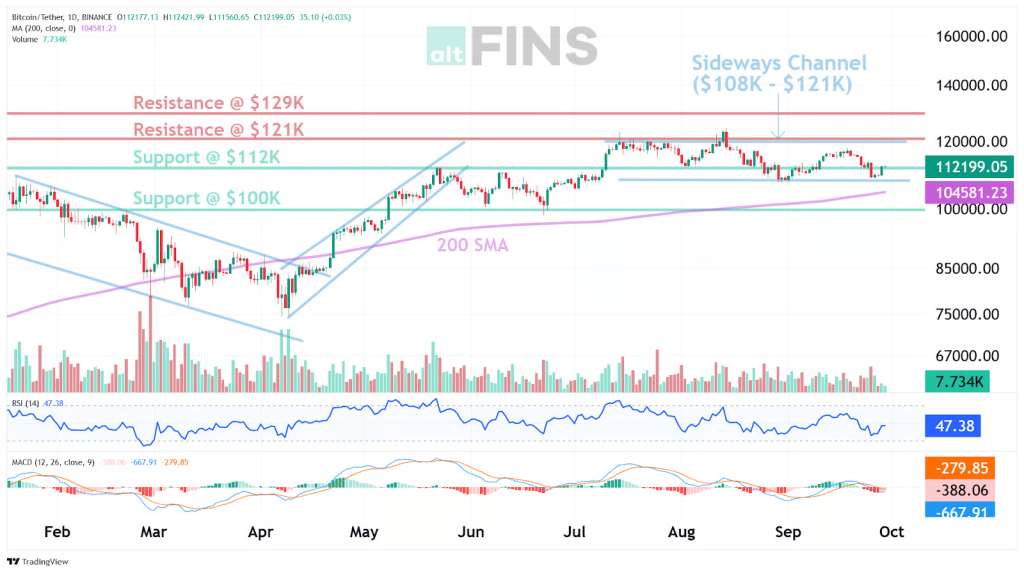

Early in the month, price reclaimed $111,000; by 11 September, the market pressed into the mid $110,000s. During 17–18 September, intraday highs in the $116,000–$117,000 zone were recorded across several major venues, coinciding with the FOMC decision and a concentrated run of positive ETF flows. The final week saw a give-back of gains: bitcoin traded under $111,000 on 25 September, tested near $109,000 on 26 September, then recovered into month-end. Bitcoin closed September at about $113,000. Support was repeatedly observed around the $109,000–$111,000 band; resistance formed in the mid to high $110,000s.

Source: https://altfins.com/technical-analysis

Flows into US spot bitcoin ETFs provided high-frequency context. In the 11–16 September window, several large single-day inflows were reported, with gross additions across the cohort running into the hundreds of millions of dollars on multiple sessions. Decision day produced mixed prints at the issuer level, but the aggregate remained positive. The pattern reversed late in the month. On 22 September and 23 September, net outflows were logged; 25–26 September combined outflows approached the better part of $700 million. A strong positive day followed on 29 September, reducing the cumulative draw for the final fortnight.

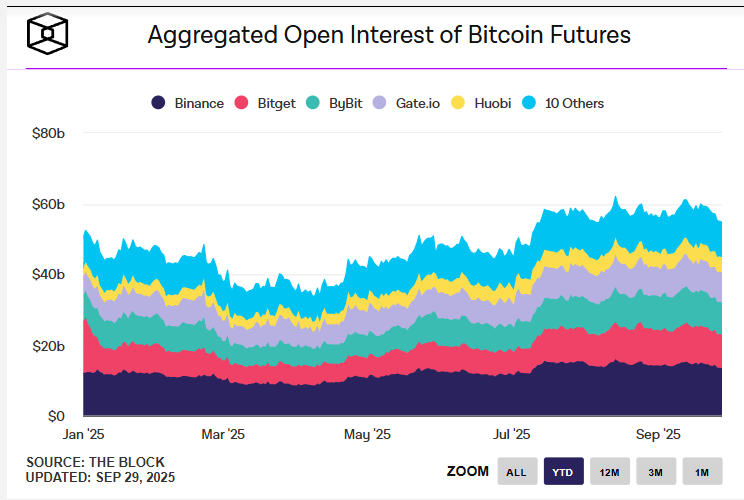

Market microstructure contributed to the transmission of these flows into price and volatility. Options activity associated with large spot ETFs expanded, with listed options on a leading vehicle reported as rivalling, and in some sessions surpassing, activity on offshore venues. The effect on intraday liquidity was twofold. First, options hedging created feedback loops around strikes that had high open interest, which could slow or accelerate directional moves depending on position orientation. Second, the expansion of on-venue options liquidity encouraged more activity to migrate to regulated venues, concentrating liquidity and risk management responsibilities among a smaller set of market makers with strong balance sheets. [Inference]

On-chain conditions presented a mixed picture. Into mid-month, a large share of circulating supply sat in profit, which historically correlates with more distribution into strength. Options open interest reached elevated levels ahead of the 26 September expiry, indicating a crowded options calendar and a potential catalyst for late-month volatility. Fees remained manageable compared with peak congestion episodes from earlier in the year, although several bursts in activity were recorded during the three volatility windows described above.

Source: https://www.theblock.co/data/crypto-markets/futures

Strategy Inc. disclosed two bitcoin purchase updates in September. On 22 September 2025, a Form 8-K reported 850 BTC acquired between 15 and 21 September for $99.7m at an average price of $117,344 per BTC, lifting aggregate holdings to 639,835 BTC, with a cumulative cost of $47.33b and an average purchase price of $73,971 inclusive of fees. A subsequent update for the week of 22–28 September detailed an additional 196 BTC for $22.1m at an average of $113,048 per BTC, bringing total holdings to 640,031 BTC and cumulative cost to $47.35b.

Source: https://www.theblock.co/data/crypto-markets/futures

By 29 September 2025, tracked corporate treasuries collectively held more than 750,000 BTC, with Strategy the dominant holder alongside Marathon, Riot, Galaxy Digital, Metaplanet, and others. Funding continued to rely on multiple at-the-market programmes: the 22 September Form 8-K outlined draws across common-stock and preferred-stock ATMs, and disclosures for 22–28 September noted $128.1m in net proceeds, a portion of which funded the 196 BTC purchase that week, with the remainder retained for general corporate purposes, including preferred-stock dividends.

Ethereum: price action and the “safe DeFi” framing

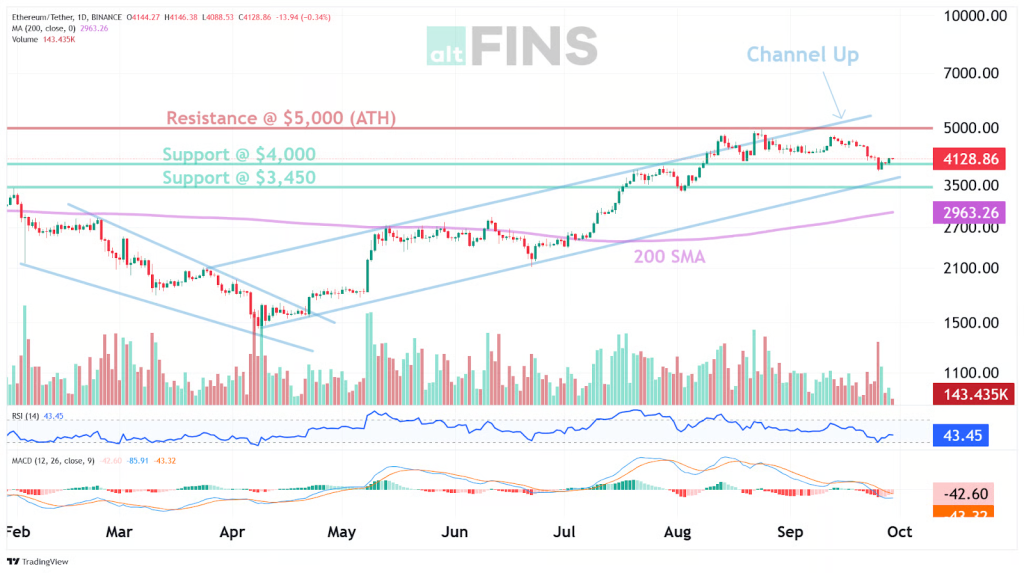

Ether’s September range was well defined. Daily closes showed a start near $4,314 on 1 September, a rise toward the mid-$4,000s around 17–18 September, and a dip to the high-$3,800s on 26 September during the most concentrated deleveraging phase. The $4,000 figure acted as a pivot, with multiple tests and defences during the month; it was temporarily lost on 25 September before stabilisation resumed. The pattern broadly mirrored bitcoin’s arc, with beta slightly higher on down days.

Source: https://altfins.com/technical-analysis

US spot ether ETFs, where listed, showed choppy net flows. Large positive prints were recorded on 12 September and 15 September, with cumulative multi-day additions supporting the push into mid-$4,000s. During 22–26 September, a series of outflow days aligned with price weakness beneath $4,000. A recovery day on 29 September brought a return to positive net flow. The flow-price relationship remained bidirectional, as ETF demand can follow price as often as it leads it, particularly when intraday volatility and options hedging pressures increase. [Inference]

Vitalik Buterin’s mid-September post set out a revenue-versus-mission tension inside Ethereum, then argued that “low-risk DeFi” can resolve it. The claim positioned payments, simple savings, fully collateralised lending, synthetic assets, and basic exchange as the network’s analogue to Google’s search: a durable, culturally aligned revenue engine that can subsidise experimentation elsewhere. The rationale rested on two points: these services provide irreplaceable utility to users that lack reliable TradFi access; and they fit Ethereum’s values by favouring transparency, permissionless access, and predictable outcomes over reflexive leverage.

The post contended that the case for low-risk DeFi has strengthened as protocol, oracle, and operational risks have fallen relative to earlier cycles, when high yields were sustained by subsidies or speculative churn. Regulatory frictions were cited as a historical reason for misaligned activity, while a “stable core” of resilient applications was described as emerging as code quality and risk tooling improved. The proposed design principles emphasised conservative loan-to-value ratios, robust medianised oracles with fallbacks, circuit breakers, measured liquidations, proof-of-reserves or equivalent attestations for custodial pools, segregation of client assets, and strict limits on rehypothecation. Preference was expressed for stablecoins with strong issuance frameworks and for savings products backed by short-duration, fully reserved assets.

Source: https://vitalik.eth.limo/general/2025/09/21/low_risk_defi.html

A forward path was outlined in which low-risk DeFi becomes a base for broader functionality. With more financial and non-financial activity recorded on-chain, reputation-based undercollateralised lending could become viable; prediction markets could serve as practical hedging tools alongside traditional positions; and the ecosystem could incrementally diversify beyond USD exposure toward baskets, CPI-linked “flatcoins”, and other stable forms of value. The post argued that this mix would contribute meaningfully to ETH-denominated collateral demand and to fee revenue, avoid incentives that push the L1 toward high-frequency trading optimisation, and align Ethereum’s economic engine with services that are culturally defensible and socially useful.

Stablechains: Stablecoin-first blockchains

The “stablecoin-first” thesis has moved from a niche idea to a focal point in developer and investor discussions. The thrust is operational rather than speculative: architect for fiat-pegged tokens and payments, then prove reliability at consumer scale. The design brief converges on four properties, each emphasised by payment-ops practitioners and compliance teams: fees that remain low and bounded during traffic spikes; fast, predictable finality with low revert rates; native integration with issuers, money-service businesses, and on-ramps; and merchant-grade UX features such as programmable refunds, recurring payments, spend limits, and recoverable accounts. The draw for experts is straightforward. As stablecoin settlement and payroll use grow, card-like predictability and bank-grade reconciliation become more important than raw throughput or trader-oriented features.

Source: https://www.mckinsey.com/industries/

Among current leaders, three patterns stand out. Tempo is being positioned as a payments-first L1 that treats issuer relationships and fintech distribution as first-class concerns. Public materials describe sub-cent target fees, tight finality guarantees, and controls to suppress extractive MEV on retail flows, with initial use cases spanning global payouts, remittances, micro-spend, and agent-to-agent settlement. Plasma advances a similar posture with near-zero-fee transfers and high-throughput targets, plus an explicit go-to-market around merchant and wallet partners; its claims emphasise breadth of stablecoin support and partner integration rather than trader liquidity. In the interchain domain, Noble functions as a canonical issuance hub for native USDC in Cosmos, allowing IBC-level distribution so appchains can settle in dollars without managing issuer integrations themselves; this makes dollar rails a built-in primitive across interoperable chains.

Why the narrative is growing can be traced to concrete operational gaps that these designs try to close:

- Settlement reliability under load: payments fail when fee markets spike; stablecoin-first stacks prioritise bounded fees, congestion controls, and preconfirmations so consumer transactions complete on time.

- Compliance and reconciliation: issuer-aware primitives, traceable transfers, and standardised metadata reduce exceptions for PSPs and acquirers, and simplify audits.

- Merchant economics: sub-cent fees, immediate settlement, and programmable refunds improve unit economics against legacy rails where interchange, scheme, and FX costs compound.

- Agentic software and machine payments: bots and autonomous agents require high-frequency, low-value transfers with deterministic outcomes; predictable blockspace and low revert rates are prerequisites.

If these chains sustain low, stable fees and predictable finality in real traffic, they will become easier to plug into existing fintech distribution, with fewer reconciliation edge cases and cleaner compliance surfaces. That prospect, rather than headline TPS, is what has pushed stablecoin-first designs to the centre of current debate.

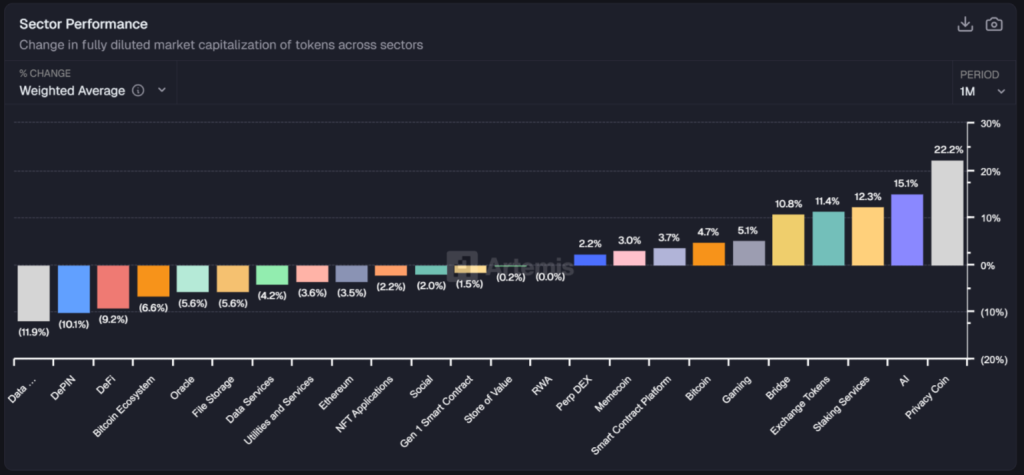

Sector Performance

Sector moves were dispersed. Leaders were Privacy Coin up 22.2 per cent, AI up 15.1 per cent, and Staking Services up 12.3 per cent, with Exchange Tokens and Bridge also positive. Bitcoin’s sector sat in the green, while Ethereum’s sector was modestly negative, which is consistent with BTC’s firmer tape through mid-month. Laggards clustered in DeFi, DePIN, and data or oracle infrastructure, which finished lower as risk was pared back on down days. The split points to a market rewarding clear, cash-flow or utility narratives, and penalising leverage-sensitive segments when liquidity thins.

TradFi rails for tokenised money

The narrative has centred on banks formalising their own tokenised-money rails, with September marking a shift from pilots to concrete programmes and funding. On 23 September 2025, Fnality announced a $136m Series C backed by Bank of America, Citi, WisdomTree, KBC, Temasek, and Tradeweb, with existing investors including Santander, Barclays, BNP Paribas, DTCC, Euroclear, Goldman Sachs, ING, Nasdaq Ventures, State Street, and UBS; funds were earmarked to expand beyond the live sterling system toward multi-currency settlement in wholesale tokenised cash.

Two days later, on 25 September 2025, nine European banks, including ING, UniCredit, KBC, Danske Bank, SEB, and Raiffeisen, disclosed a new company to issue a euro-denominated stablecoin, targeting a first release in the second half of 2026. The move signalled a coordinated, bank-led approach to tokenised money for retail and corporate payments in the euro area.

On 30 September 2025, the Financial Times reported that SWIFT would launch a bank-backed shared ledger in partnership with ConsenSys and tier-one banks such as Bank of America, Citigroup, and NatWest, aiming for instant, always-on cross-border settlement with smart-contract-based validation and ISO 20022 interoperability. The plan positioned SWIFT’s rail as a compliance-first alternative that can interoperate with banks’ existing back-office systems while responding to the rise of stablecoins.

JPMorgan’s Kinexys sat alongside these developments as the corporate-payments rail most frequently cited by banks and press through the month. On 23 September 2025, a detailed Forbes profile placed Kinexys at the centre of the bank’s digital-asset strategy, highlighting programmable, always-on USD settlement for corporates; separate industry coverage during late September’s Sibos cycle reiterated tokenised-deposit and on-chain FX extensions as near-term priorities.

Context data points reinforced why this narrative is growing. Research published on 12 September 2025 estimated tokenised cash near $300bn in circulation, with about $270bn in stablecoins and rapid growth in tokenised T-bills and money-market funds; bank groups and market-infrastructure operators have framed bank-operated rails as a way to deliver finality, reconciliation, and regulatory auditability at that scale.

Taken together, 23–30 September delivered three visible steps forward for bank-grade rails, each pulling the narrative toward implementation: fresh capital for wholesale tokenised cash, a euro stablecoin issuer group, and a SWIFT-operated shared ledger aligned with bank compliance and messaging standards.

Market structure: retail-facing L1 competition

As Q4 begins, the L1 contest for retail flow is escalating, framed as the last sprint of this cycle. The competitive levers are clear: sub-cent trading costs, faster time to finality, breadth of spot and derivatives products, and seamless distribution through wallets and on-ramps. Platforms that can prove resilience under traffic spikes, offer deep and liquid markets, and confirm reliably on mobile are the ones attracting day-to-day users.

Solana has emphasised engineering improvements aimed at predictable fees and lower failure rates during activity bursts, positioning itself as the chain optimised for retail sessions. BNB Chain is pushing validator proposals to compress fees and shorten intervals, while coupling this with exchange-driven distribution through Aster. Hyperliquid continues its derivatives-first strategy, pairing native dollar rails with fast matching and visible liquidation handling to replicate an exchange-grade feel while remaining on-chain.

User experience and distribution remain decisive. Wallet features that cut first-trade time, enable account recovery, and support one-tap funding have become non-negotiable for retail. Listings are concentrated on meme tokens and low-slippage stablecoin pairs, with incentives deployed selectively around launches. The message from September is practical: retail capital follows concrete improvements in cost, speed, convenience, and access—not TPS claims. This sets the stage for Q4 as the decisive battleground, where each venue signals whether its edge lies in fee leadership, reliability under load, or depth in derivatives.

Closing

September 2025 conformed to its reputation as a difficult month for risk assets. A modest rally in early to mid-month, aided by a 25-basis point policy rate cut on 17 September and strong ETF inflows, carried bitcoin toward the mid-$110,000s and pushed ether into the mid-$4,000s. The final week reversed that progress. Futures liquidations rose, ETF outflows accumulated, and options skews reflected more demand for downside protection. Bitcoin found support around the $109,000–$111,000 band; ether lost $4,000 briefly, then stabilised.

Macro remained the dominant frame. The Federal Reserve’s decision and dot plot provided a cautious easing signal; the absence of a clear disinflation acceleration left participants alert to two-way risks into Q4. The migration of derivatives activity toward on-venue listed options for large spot ETFs further integrated crypto volatility with regulated market microstructure. Liquidity thus became more sensitive to a compact set of flows, hedging imperatives, and creation-redemption mechanics.

Infrastructure developments centred on stablecoin-first rails and bank-operated settlement systems. Tempo and Plasma articulated payments-centric visions on public chains, while SWIFT and Fnality advanced bank-grade settlement approaches. These strands converged on a shared objective: reliable, compliant, low-latency settlement for tokenised money. The trade-offs differed. Public chains emphasised openness and distribution; bank-chains emphasised control and compliance.

Corporate treasuries continued to allocate to bitcoin, although the amounts were modest relative to prior quarters. Fair-value accounting made the drawdown during 24–27 September immediately visible in reported earnings for exposed firms. Market-structure competition across retail-facing L1s persisted, with Solana’s client diversification and BNB Chain’s fee reductions highlighting two approaches to the low-fee race. Direct comparisons remained difficult in the absence of consistent metrics for finality under load, user experience, and fiat on-ramp breadth.

The month closed with the drivers of Q4 already visible: policy settings that remain data dependent; an ETF pipeline that could expand; an Ethereum narrative leaning toward “safe DeFi”; and bank-chain pilots that may demonstrate concrete settlement benefits. The connective tissue across these topics remained liquidity. Where rates, flows, and rails support deeper and more stable liquidity, price action tends to be more orderly; where they falter, volatility returns quickly. The events of September 2025 presented a compact study in how these elements interact, without offering definitive conclusions.