Crypto Volatility with Security Breaches Trade Policies and Market Decline.

28th Feb 2025 • 10 mins read

Key Numbers:

Bitcoin US$ 83,878.34 (-20.50%) Ethereum US$ 2,221.20 (-35.27%)

1-month return

Total Crypto Market Cap US$ 2.78T (-23.20%)

2025 returns

Bitcoin –11.99% Ethereum –34.82% Gold +10.33%

NASDAQ -2.40% S&P500 -1.23%

Key Takeaways

- Bybit Breach: A $1.5B Ethereum heist attributed to North Korea’s Lazarus Group has exposed critical exchange vulnerabilities.

- Tariff Escalation: The renewed imposition of U.S. tariffs has amplified geopolitical risks and compounded market uncertainty, further straining investor confidence and destabilizing sentiment.

- Bitcoin Correction: Bitcoin’s price tumbled sharply from above $100K to below $78

- Ethereum Slide: A precipitous mid-month decline of nearly 38% underscored heightened market risks, even as pockets of investor optimism persisted regarding a potential recovery.

- Solana Under Pressure: The $LIBRA scandal and a broader market sell-off triggered a severe drop in Solana’s metrics.

- ETF Applications Surge: A robust pipeline of ETF filings, highlighted by Franklin Templeton’s Solana spot ETF.

- Speculative Sell-Off: Deep losses in high-risk speculative assets such as memecoins and gaming tokens starkly contrasted with the resilience observed in store-of-value assets.

- ETF Outflows: Significant institutional capital withdrawals from crypto ETFs underscored a decisive shift toward risk-off strategies, as market participants sought to minimize exposure amid escalating uncertainty.

- Inflation & Fed Delays: Persistent inflationary pressures combined with postponed Fed rate cuts have intensified overall market nervousness.

- Regulatory Pivot: Pro-innovation regulatory reforms and the easing of SEC enforcement actions signal a strategic move toward deeper integration of crypto assets into traditional finance.

- Asian Adoption: Progressive regulatory policies in key markets like South Korea and Hong Kong are positioning Asia as a major driver of crypto adoption and growth.

Market Overview

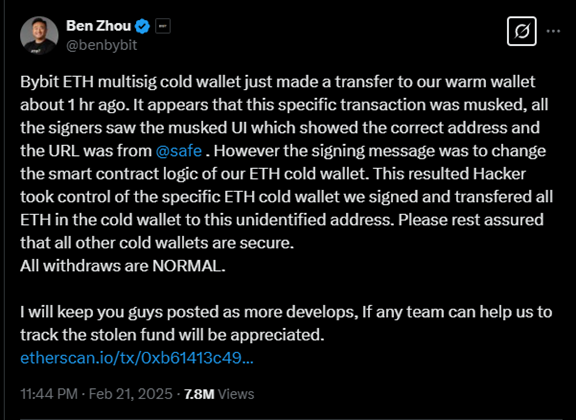

The crypto scene was shaken on February 21, 2025, when reports surfaced that Bybit, one of the largest global cryptocurrency exchanges, had suffered a massive security breach, resulting in the theft of approximately $1.5 billion in Ethereum. Initial blockchain forensics quickly traced the stolen funds to North Korea’s Lazarus Group, a notorious state-sponsored hacking collective responsible for multiple high-profile crypto heists in the past. Despite the magnitude of the attack, Bybit maintained solvency and operational stability, effectively managing withdrawal requests and ensuring market liquidity remained intact. Unlike past exchange collapses that led to fire sales and mass panic withdrawals, Bybit’s orderly response demonstrated its strong financial reserves and risk management framework. However, the scale of the breach undermined investor confidence, reinforcing concerns that even industry giants with robust security measures remain vulnerable. The hack fueled uncertainty in the market, raising questions about exchange security, centralized platform risks, and potential regulatory scrutiny in the wake of the attack.

Source: https://x.com/benbybit/status/1892963530422505586

Just as the market was processing the implications of the Bybit breach, macroeconomic uncertainty intensified with President Donald Trump’s announcement to continue and expand tariffs on key trading partners. Initially, markets had already reacted negatively when the U.S. imposed a 10% tariff on Chinese goods and threatened a 25% tariff on European Union imports. A brief reprieve came when Trump paused some of the measures, leading to a short-lived bounce in risk assets, including crypto. However, the confirmation that tariffs would resume in full force, including a 25% levy on imports from Canada and Mexico starting March 4, 2025, rekindled concerns over global trade disruptions, inflationary pressures, and economic slowdowns. The crypto market responded cautiously, with investors increasingly reluctant to deploy capital amid heightened geopolitical risk. While Bitcoin and Ethereum initially recovered from their February lows, the reality of an escalating trade war and the potential for prolonged economic uncertainty weighed on sentiment, reinforcing a risk-off environment as traders awaited further policy developments.

Against this backdrop, February 2025 was packed with key developments across the crypto space, from major protocol upgrades to security breaches and corporate moves toward public listings. Ethereum’s much-anticipated “Pectra upgrade” remained a focal point, with expectations that its scalability improvements could reignite ETH’s momentum later in the year. Other blockchain networks also made strides in performance upgrades. Cardano introduced Node 8.3.0, optimizing network synchronization and dApp efficiency, while laying the groundwork for the Conway Ledger Era, which enhances decentralized governance. Polkadot 2.0 pushed forward with refinements to its parachain model, improving scalability and interoperability, alongside governance streamlining to foster more efficient decision-making.

Price Performance

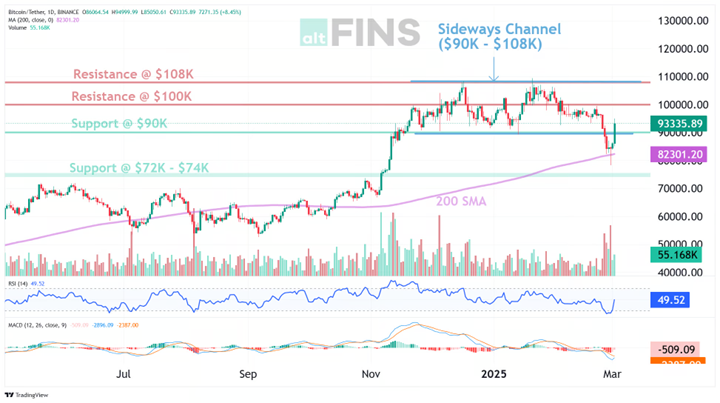

Bitcoin (BTC): February 2025 was a volatile month for Bitcoin, reversing some of its late-2024 gains. Entering the month above $100,000, BTC was buoyed by strong institutional inflows from January but faced a sharp mid-month correction driven by macro uncertainty and ETF outflows. This pullback saw Bitcoin drop below $90K for the first time since November 2024, ultimately falling from a peak of $105,000 early in the month to $78,000 by the final week- a nearly 25% correction. These events culminated in record-setting outflows, with investors withdrawing over $1 billion from spot Bitcoin ETFs in a single day, marking the largest one-day outflow since their inception. The confirmation of continued and expanded tariffs by President Donald Trump further exacerbated market instability, leading to cautious sentiment among investors and significant capital retraction from crypto ETFs. Compared to late-2024 highs in the mid-$90K range, Bitcoin briefly reached a new all-time high (~$105K) before retreating, closing the month lower than its previous peak. Nevertheless, Bitcoin’s February 28 price remained significantly higher year-over-year, and its post-2024 halving trend remains structurally bullish in the long term.

Source: https://altfins.com/

Ethereum lagged behind Bitcoin in February, weighed down by ETF outflows and a broader market rotation. Starting the month near $3,400, ETH dropped sharply to $2,100—a decline of about 38.24%—before recovering to $2,264 by month’s end. In addition to the earlier noted Bybit hack, investor fears that hackers might offload the stolen tokens, triggering a domino effect of panic selling, further pressured the price action. Despite these setbacks, Ethereum’s strong staking participation (with over 30 million ETH locked) and anticipation for the upcoming “Pectra” upgrade to boost network scalability sustained a positive long-term outlook.

Source: https://altfins.com/

Solana experienced a significant price decline in February, facing a double blow from the broader market downturn and the $LIBRA scandal. The collapse of $LIBRA, a meme coin promoted by Argentine President Javier Milei, triggered widespread panic after it surged past a $4 billion market cap before crashing by over 90% amid allegations of fraud and insider trading. The scandal severely damaged investor confidence in Solana’s ecosystem, particularly within its meme coin sector, leading to a sharp decline in DEX volumes and a 40% drop in Solana’s total value locked (TVL) over 30 days. While Solana had previously been seen as Ethereum’s strongest competitor, the combination of a market-wide sell-off and the $LIBRA debacle accelerated its decline, reinforcing investor caution toward high-risk assets in the ecosystem.

Sector Performance

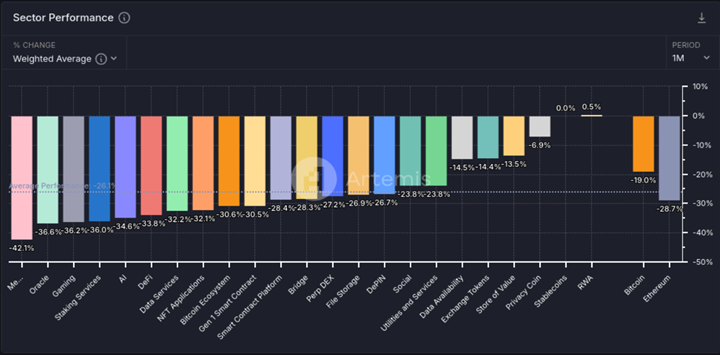

Source: Artemis.xyz

The broader crypto market mirrored Bitcoin’s struggles, with nearly every sector suffering steep losses in February. Memecoins (-42.1%), Oracles (-36.6%), and Gaming (-36.2%) led the declines, as risk appetite evaporated, and speculative assets faced the most aggressive selling. The average sector decline stood at -26.1%, with AI (-34.6%), DeFi (-33.8%), and the Bitcoin Ecosystem (-32.1%) also seeing significant drawdowns. Only a handful of categories outperformed Bitcoin’s -19.0% decline, including Data Availability (-14.5%), Exchange Tokens (- 14.5%), Store of Value (-13.5%), and Privacy Coins (-6.9%), suggesting a shift toward slightly more resilient assets. Meanwhile, Ethereum underperformed Bitcoin, sliding -28.7%, reflecting deeper weakness in altcoins. The one exception to the widespread downturn was Real-World Assets (RWA), which managed a modest 0.5% gain, reinforcing the sector’s growing appeal as a stable investment class amid market turbulence.

Institutional Adoption and Sentiment

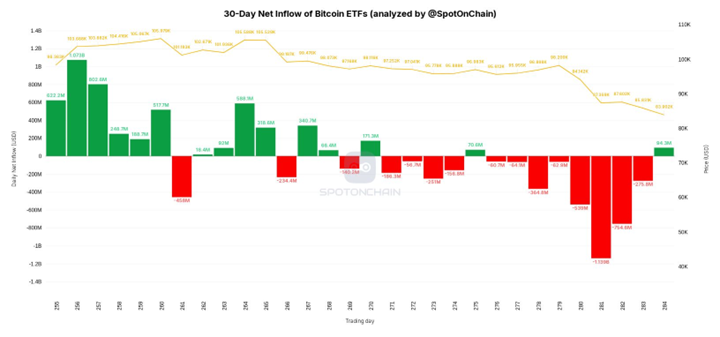

In early 2025, the market experienced significant fluctuations, impacting exchange-traded funds (ETFs). January commenced with robust inflows into crypto-based ETFs, particularly those tracking Bitcoin, as institutional investors sought exposure to the burgeoning asset class. Notably, BlackRock’s iShares Bitcoin Trust (IBIT) amassed substantial assets under management during this period. From January 13 to February 5, 2025, U.S.-listed spot Bitcoin ETFs attracted $4.4 billion in net inflows, a 175% increase compared to the same period in 2024.

Source: https://platform.spotonchain.com/

Despite these headwinds, the crypto ETF market saw notable shifts in February, with institutional participation remaining strong despite increased volatility. Bitcoin ETFs, which had amassed over $40 billion in assets within their first year, faced significant net outflows as investors locked in profits following Bitcoin’s rally. Total withdrawals across Bitcoin ETFs reached approximately $3.5 billion, with BlackRock’s iShares Bitcoin Trust (IBIT) alone losing $721 million. This sell-off coincided with an 18% drop in Bitcoin’s price, reflecting a broader risk-off sentiment. Ethereum ETFs also recorded net outflows, including $41.82 million on February 28, contrary to earlier expectations of inflows ahead of the Pectra upgrade. Despite these outflows, ETF trading volumes remained strong, with Bitcoin ETFs averaging $3–4 billion in weekly turnover. Prices reflected market volatility, with Bitcoin ETF shares declining 10–15% and Ethereum ETFs falling 7–8%. However, total assets under management remained substantial, highlighting continued institutional interest in regulated crypto exposure even as short-term sentiment shifted.

The pipeline for new cryptocurrency ETFs continued to expand, with 47 active filings in the U.S. by February, reflecting growing institutional interest in regulated digital asset exposure. A major development came from Franklin Templeton, which filed for a Solana spot ETF on February 21, marking its entry into altcoin-based ETFs. The proposed fund aims to provide investors with direct exposure to Solana and may incorporate staking mechanisms, allowing it to earn rewards through the blockchain’s proof-of-stake consensus process.

Other ETF proposals include diversified crypto baskets, futures-based ETFs for smaller assets, and even memecoin-focused products like Dogecoin and $TRUMP ETFs. Analysts believe Bitcoin and Ethereum-related ETFs, particularly those tied to options strategies or leveraged products, have the highest likelihood of approval. However, the regulatory outlook for altcoin spot ETFs remains uncertain, with cautious optimism that at least one or two non-BTC/ETH spot ETFs could receive approval in 2025, opening the door for broader institutional investment in alternative digital assets. Macroeconomic Landscape, Headwinds, and Sentiment

Macroeconomic Landscape, Headwinds, and Sentiment

The U.S. Consumer Price Index (CPI) for January 2025 reported a 3.0% year-over-year increase, exceeding expectations and marking the highest inflation rate since June 2024. This sustained inflationary pressure has led traders to push back anticipated Federal Reserve interest rate cuts from September to December 2025. CPI has been climbing again since November 2024, reversing its previous downtrend. This upward trajectory suggests that inflation remains persistent, reinforcing the view that the Fed is unlikely to ease monetary policy anytime soon. Consequently, markets reacted negatively on the announcement, with risk assets like Bitcoin and Ethereum experiencing sharp declines, as traders adjusted their rate cut expectations. With inflationary pressures building, the likelihood of an earlier Fed pivot is diminishing, keeping financial markets on edge.

Source: https://www.investing.com/

Despite market turbulence, several macro and policy tailwinds helped sustain investor optimism in February 2025. In the U.S., the Trump administration signaled a more favorable stance on digital assets, with the president publicly discussing Bitcoin and a more innovation-friendly SEC suggesting a potential shift away from the regulatory crackdowns seen in 2024. These developments reassured investors concerned about policy risks, particularly as pro-crypto voices in Washington gained traction. Meanwhile, Europe accelerated its efforts to integrate crypto under the MiCA framework, providing regulatory clarity that contrasted with past uncertainties. In China, signs of economic stimulus helped ease fears of a global slowdown, stabilizing broader risk sentiment. By the end of February, market sentiment was split, bulls highlighted catalysts like the post-Bitcoin halving cycle, growing institutional participation through ETFs, and expectations for eventual Fed easing as reasons to stay constructive. Bears, however, remained cautious, pointing to persistent macro risks, excess leverage in crypto markets (evidenced by $1.5 billion in February liquidations), and the possibility of a stronger-than-expected economy delaying rate cuts. While geopolitical risks and higher interest rate expectations weighed on sentiment, crypto markets demonstrated resilience, with many investors maintaining a cautiously bullish outlook driven by long-term adoption trends, policy clarity, and Bitcoin’s growing role as a digital hedge in uncertain times.

global markets, compounding concerns already fueled by tariffs on Canada, Mexico, and China. His proposal to acquire Greenland, a “gold card” citizenship program allowing wealthy foreign investors to buy U.S. citizenship, and a federal restructuring effort led by Elon Musk’s “Doge” team have sparked debate over the administration’s strategic direction. Meanwhile, his suggestion for the U.S. to take control of Gaza has been swiftly rejected by global leaders, while his push to fast-track a resolution to the Ukraine-Russia conflict has unsettled European allies. These moves, alongside a broader effort to reassert U.S. influence on the world stage, add to the complex geopolitical backdrop that investors must navigate. While these actions may seem destabilizing in the short term, we maintain that they are largely political posturing aimed at reestablishing U.S. dominance in global affairs. The uncertainty they introduce could weigh on risk assets in the immediate future, but they do not alter the long-term crypto thesis. Market cycles, macro trends, and Bitcoin’s role as a hedge against uncertainty remain intact. These may capture the headlines short term, but the long-term crypto thesis is still in play and bullish.

Regulatory Changes Under Trump’s Presidency

Trump’s second term is bringing a significant shift in U.S. crypto policy, with February marking the beginning of a pro-innovation regulatory approach. Under the Biden administration, the Securities and Exchange Commission (SEC) had been known for aggressive enforcement actions, but the new administration took a different path. Mark T. Uyeda was appointed as Acting SEC Chairman, and one of his first major moves was establishing the Crypto Task Force on January 21, 2025, led by Commissioner Hester Peirce. The task force aimed to streamline ETF approvals, clarify crypto classification, and move away from a hostile regulatory stance toward a structured oversight model. A major policy shift came with the repeal of Staff Accounting Bulletin 121 (SAB 121), which had previously discouraged banks from offering crypto custody services. Its removal signaled a broader effort to integrate crypto into traditional finance rather than restrict it, allowing banks to explore digital asset services more freely.

Alongside this regulatory shift, stablecoin legislation gained momentum in February. The bipartisan GENIUS Act, introduced in Congress, proposed a federal framework for stablecoin issuance, including reserve requirements and Federal Reserve oversight for large issuers while allowing state-level supervision for smaller projects. A similar bill in the House reinforced expectations that stablecoin regulation could be the first major piece of U.S. crypto legislation. The growing push for clear stablecoin rules was seen as an effort to preserve the U.S. dollar’s dominance by integrating stablecoins into the financial system while preventing industry migration to offshore jurisdictions with clearer regulatory frameworks, such as Europe’s MiCA regime. Market analysts noted that a well-regulated stablecoin industry could drive more institutional adoption and position the U.S. as a leader in crypto innovation.

The SEC also restructured its approach to enforcement and oversight. On February 20, 2025, it replaced the Crypto Assets and Cyber Unit with the Cyber and Emerging Technologies Unit (CETU), appointing Laura D’Allaird to lead efforts focused on cybersecurity risks, fraud prevention, and innovation-friendly regulation. The most notable regulatory move came on February 21, 2025, when the SEC dismissed its lawsuit against Coinbase, marking a clear departure from its previous enforcement-heavy approach. The SEC also began reviewing applications for new crypto ETFs, including Solana, XRP, and multi-asset funds, suggesting a shift toward allowing regulated exposure beyond Bitcoin and Ethereum. This move was seen as a major step toward expanding institutional crypto products, further solidifying digital assets within traditional financial markets.

Another notable development in February was the growing discussion of Bitcoin as a strategic reserve asset. While no official policy was enacted, Senator Cynthia Lummis and other pro-crypto lawmakers advocated for the U.S. Treasury or Federal Reserve to hold Bitcoin, mirroring its role as “digital gold.” The Texas state legislature advanced a bill to create a Bitcoin-backed state reserve, reinforcing this narrative at the state level. Trump’s pro-Bitcoin rhetoric, combined with the SEC’s regulatory shift, fueled renewed confidence in the market. A survey in February 2025 found that 49% of respondents expected clearer regulations under Trump, while others expressed concerns that Bitcoin might receive preferential treatment over DeFi and Web3 innovations. Overall, February’s regulatory shifts—ranging from SEC policy pivots to stablecoin legislation—galvanized the industry, positioning the U.S. as a leader in crypto regulation and fostering long-term market confidence.

Asian Adoption and Crypto Developments

Asia-Pacific markets played a pivotal role in crypto adoption throughout February 2025, often counterbalancing trends driven by the U.S. South Korea made headlines by reversing its long-standing crypto ETF ban, signaling a shift in institutional access to digital assets. After years of strict limitations, the Korea Exchange announced plans to explore approving crypto-based ETFs, marking a major policy shift driven by global demand and concerns over competitiveness. Simultaneously, South Korea’s Financial Services Commission moved to lift restrictions on institutional crypto trading, opening the door for pension funds and banks to invest in digital assets. These steps, expected to roll out through 2025, have the potential to unlock significant institutional inflows. Market analysts believe South Korea’s pivot could spur Asia-focused crypto ETFs, giving regional investors more options while reinforcing the country’s status as a major player in digital asset markets.

Hong Kong continued positioning itself as a leading crypto hub, building on its regulatory framework that allows licensed exchanges to offer retail crypto trading. By February, trading volumes were climbing as more residents gained access to Bitcoin and Ethereum through approved platforms. The government doubled down on its pro-crypto stance, with additional exchange licenses in the pipeline. Hong Kong’s openness contrasts with mainland China’s continued restrictions, though speculation grew that Beijing could soften its stance if Hong Kong’s model proves successful. Some Chinese state academics began discussing the possibility of a regulated crypto framework by the end of 2025, though no official policy changes had been made. Meanwhile, crypto companies with Chinese origins continued migrating to Hong Kong, further strengthening the region’s role as a gateway for digital assets in Asia.

Elsewhere, Japan and Singapore maintained their strong crypto positions, with Japan’s financial sector launching new products—including its first yen-pegged stablecoin—while Singapore remained a preferred base for blockchain startups due to clear licensing rules and tax incentives. Southeast Asian nations like Thailand and Indonesia advanced regulatory frameworks for crypto exchanges and token offerings, aiming to capitalize on fintech innovation. In contrast, India remained hesitant, with high taxation and regulatory uncertainty dampening retail participation. The key difference between Western and Asian crypto narratives in February was the focus—while the U.S. was driven by ETF approvals and institutional adoption, Asia emphasized retail engagement, gaming, and DeFi. Memecoins, blockchain gaming tokens, and AI-crypto integrations gained traction, particularly in markets like Korea and Vietnam. By the end of February, APAC’s share of global crypto trading volume was rising, with analysts noting that if trends in South Korea and Hong Kong continue, Asia could lead the next wave of adoption.

Wrapping Up

In reviewing the events of February 2025, it is evident that the crypto market was faced with a storm of challenges, ranging from the staggering Bybit breach to escalating geopolitical tensions and tariff-induced uncertainties. While disruptive, these shocks have exposed the inherent resilience of the market, as evidenced by structural long-term trends in major assets like Bitcoin and Ethereum. It was observed that despite sharp corrections and liquidity pressures, the fallout was mitigated by robust institutional backing and rapid regulatory pivots. The ability of the market to absorb these shocks without a complete breakdown signals a maturity that contrasts with its nascent volatility, confirming that while short-term sentiment remains cautious, the underlying fundamentals remain strong.

Looking forward, the transformative regulatory initiatives and strategic technological upgrades—such as Ethereum’s eagerly anticipated “Pectra” upgrade—are poised to redefine the crypto landscape. Global adoption trends, especially the policy shifts in Asia and renewed interest from institutional investors, further underscore a market recalibrating for long-term growth. The interplay of innovation, evolving compliance standards, and the integration of digital assets into traditional finance positions the crypto space not merely as a high-risk asset class, but as a vital component of the future financial ecosystem. In sum, while immediate headwinds persist, the strategic realignments underway lay a robust foundation for sustainable advancement in the years ahead.