Bitcoin Broke Out of Its March Range, Closing The Month Up 12.49% At $94.110.

30th April 2025 • 12 mins read

Key Numbers:

Bitcoin US$ 94,011.44 (12.49%) Ethereum US$ 1,765.41 (-4.25%)

1-month return

Total Crypto Market Cap US$ 3.03T (12.22%)

2025 returns

Bitcoin –1.35% Ethereum –48.1981% Gold +24.34%

NASDAQ -9.65% S&P500 –5.31%

Key Takeaways

- Macro headwinds: Q1 2025 GDP contracted 0.3 % annualized, core PCE inflation held at 2.8 % yoy, and the flash PMI dropped to 51.2, all reflecting tariff-induced strains on growth and sentiment.

- Regulatory shift: the UK unveiled a draft unified crypto-asset framework, US bank regulators rescinded prior digital-asset custody guidance, and the SEC announced a bespoke rulemaking process over the next 12–18 months.

- Bitcoin rally: BTC jumped 5.0 % to $91,713 on April 22, breaking above the 50-day moving average with RSI in the 60s, suggesting tactical entry points with stops near $87,500 to guard against false breakouts.

- Ethereum & DeFi health: ETH slipped 1.6 % to close at $1,793, yet over 92,000 ETH net flowed into Binance, signaling accumulation, while Aave and Compound maintained TVL above $3.4 billion and $2.7 billion respectively.

- On-chain activity: daily active addresses rose 4 %, transaction fees per block peaked at $12,500, stablecoin supply expanded by $4.2 billion, and CME Bitcoin futures open interest hit an all-time high of 120,000 contracts.

- Altcoin season signal: BTC dominance flirting with 70 % marks the cusp of rotation into high-beta sectors—AI protocols, NFT infrastructure, privacy coins and memecoins are poised to lead the next leg of gains.

Late‐April data revealed the U.S. economy contracted at a 0.3 percent annualized rate in Q1 2025—the first quarterly decline in three years—driven largely by import front‐loading ahead of tariff hikes that swelled the trade deficit, even as consumption and equipment investment showed pockets of resilience. Concurrently, April’s PCE price index rose 0.3 percent month-over-month, with core PCE inflation also up 0.3 percent and standing at 2.6 percent year-over-year, underscoring persistent price pressures. This stagflation-like mix kept short-term Treasury yields elevated despite growth concerns, reinforcing market conviction that the Fed will maintain a higher-for-longer policy stance. For our fund, navigating this environment will require agile positioning between inflation-hedge narratives and rate-sensitive carry strategies as real-rate dynamics and investor sentiment evolve.

Evolving Regulatory Frameworks

On April 24, U.S. bank regulators (the Fed, FDIC and OCC) jointly withdrew their 2023 guidance requiring prior approval for crypto custody, trading and stablecoin services—effectively clearing the path for banks to roll out digital-asset offerings under existing safety and soundness rules. For our fund, this means we can leverage a widening pool of partner banks to broaden custody options and enhance settlement efficiency without lengthy regulatory delays. As large institutions accelerate pilot programs in custody and tokenization, we expect new bank–crypto partnerships to deliver cleaner on-ramps and deeper liquidity—advantages our portfolio is already positioned to capture.

On April 25, newly confirmed SEC Chairman Paul Atkins delivered remarks stressing that the crypto industry “deserves clear regulations rather than enforcement by hindsight.” He outlined plans for a bespoke digital-asset regulatory framework to supplant piecemeal interpretive guidance and case-by-case enforcement actions . Atkins highlighted priority areas including standardized disclosure requirements, trading-venue oversight, stablecoin reserve attestations, and custody safeguards.

The SEC’s announcement establishes a 12 to 18-month window for formal rulemaking while enforcement under existing statutes continues. We will actively monitor and participate in public comment periods to help shape the final framework. In the meantime, our emphasis remains on protocols with proven governance, transparent reserve attestations and robust compliance infrastructure—qualities that should deliver outperformance as regulatory clarity takes hold.

On April 29, the UK unveiled draft rules to bring exchanges, dealers and custodians under one regulatory roof—mandating specific capital thresholds, reserve-attestation standards, enhanced consumer safeguards and robust operational-resilience requirements for outages or cyber events. Consultation opens mid-May, with final rules due by year-end and a phased rollout through 2026. For our fund, this harmonization reduces legal ambiguity and streamlines our cross-border operations. At the same time, any upward adjustment to capital charges or custody standards is likely to raise barriers for smaller competitors, reinforcing our position as a well-capitalized, compliance-ready institution.

Price Action & Market Sentiment

Investor appetite for digital assets was underscored this month when exchange-traded funds tracking Bitcoin and Ether attracted over $3.2 billion in net inflows, led by BlackRock’s iShares Bitcoin Trust (IBIT), which alone secured nearly $1.5 billion, in its strongest weekly intake of the year. This enthusiastic fund demand set the stage for Bitcoin’s technical breakout on April 22, when the price jumped 5.01 percent to close at $91,713.49, its first close above $90,000 since early March, driven by easing U.S. tariff rhetoric and firmer expectations of regulatory clarity in both the U.S. and UK.

Bitcoin had further extended its gains to close at $94,011.44, marking a 12.49% increase for the month. Indicators such as a bullish breach of the 50-day moving average, an RSI climb into the 60s, and net-long futures positioning highlighted the move’s strength, while stops near $87,500 (the 200-hour moving average) and close monitoring of basis spreads and delta-neutral funding rates can guard against leverage-driven reversals. In a further show of corporate conviction, MicroStrategy executed its largest April acquisition over the week of April 21 to 27, adding 15,355 BTC and spending about $1.42 billion at an average price of $92,737 per coin, underscoring its long-term bullish stance on Bitcoin.

Source: https://altfins.com/technical-analysis

Ethereum underperformed in April, posting a 4.25% loss to close at $1,765.41. On-chain, CryptoQuant data show a net inflow of over 92,000 ETH into Binance during the month, signaling continued accumulatio. DeFi protocols maintained strong liquidity, with Aave V3 reporting $3.426 billion in TVL and Compound V2 holding $2.657 billion as of April 30. Meanwhile, issuers have been awaiting staking permission with the SEC extended its review of Grayscale’s February 14, 2025 proposal to enable staking in its Ethereum ETFs to June 1, 2025 under Section 19(b)(2) of the Securities Exchange Act, and Bloomberg Intelligence’s James Seyffart indicates staking could be approved as early as May 2025, with final decisions by late October 2025.

Looking ahead, the Pectra upgrade is set to activate on May 7, 2025, bundling Prague and Electra improvements such as enhanced user experience, expanded staking limits, and Layer-2 scaling support that could tighten circulating supply and invigorate demand.

Source: https://altfins.com/technical-analysis

Beyond price moves, on-chain analytics revealed sustained growth in active addresses, with daily unique addresses averaging 1.37 million in April—a 4 percent increase month-over-month—and transaction fees per block rising to $12,500 on high-activity days. Stablecoin supply, led by USDC and Tether, grew by $4.2 billion in April, underlining continued demand for dollar-pegged settlement rails. Derivatives flows also shifted. CME Bitcoin futures open interest reached a new all-time high of 120,000 contracts, driven by institutional macro desks hedging inflation and currency risk. Meanwhile, Binance futures funding rates flirted with positive territory, suggesting balanced long-short positioning amid choppy spot moves .

Altcoin season often begins once Bitcoin’s dominance index tops out in the high-60s to low-70s percent range, a signal that market participants have fully cycled through Bitcoin and are hunting for higher-beta opportunities. In both 2017 and 2021, BTC dominance peaked near 71 percent before reversing, and over the subsequent 8 to 12 weeks major altcoins—from Ethereum and Binance Coin to emerging layer-1s and DeFi tokens—rallied by multiples. Given that BTC .D is now flirting with the 70 percent mark amid easing macro headwinds, a similar rotation into alts could very well kick off around May or June 2025 and extend into the summer.

Source: https://altfins.com/technical-analysis

Key confirmations will include a sustained rejection at or just above the 70 to 72 percent level on the dominance chart, coupled with improving on-chain dynamics in large-cap alt sectors. Watch for rising total value locked in DeFi protocols, significant outflows of major tokens from centralized exchanges, and expanding futures open interest in altcoin contracts. Once those signals align, capital is likely to flow into infrastructure plays, DeFi projects and NFT-adjacent tokens, marking the start of a broad altcoin cycle that could drive selected alts over the next two to three months.

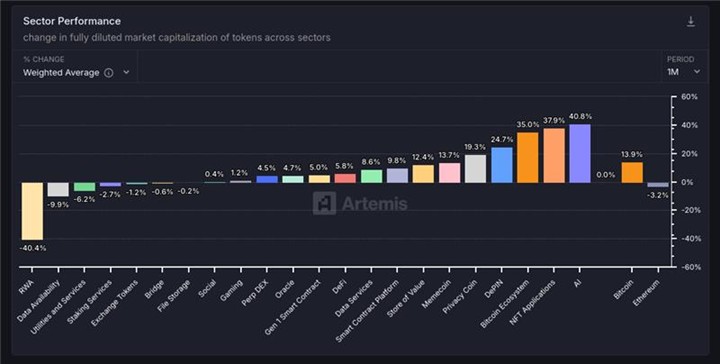

Source: https://app.artemis.xyz/

The crypto market paused in April despite Bitcoin’s breakout, with total capitalization rising 12.2 percent to US $3.03 trillion. Most legacy sectors lagged: real-world asset tokens plunged 40.4 percent, data availability projects fell 9.9 percent, utilities and services declined 6.2 percent, staking services lost 2.7 percent, and exchange tokens slipped 1.2 percent. In contrast, narrative- and technology-driven segments drove gains—AI protocols surged 40.8 percent, NFT applications rose 37.9 percent, the broader Bitcoin ecosystem rallied 35.0 percent, DePIN assets advanced 24.7 percent, and privacy coins climbed 19.3 percent. Even core infrastructure plays posted positive returns, with Gen 1 smart contract platforms up 5.8 percent and DeFi tokens gaining 8.6 percent, underscoring how speculative capital continues rotating into high-beta, on-chain innovation themes. Among individual assets, SUI led with a 46.1 percent gain, fueled by speculation around a potential SUI x Pokémon collaboration, rising to $3.51 on April 30. In contrast, TON underperformed, falling 22.1 percent to $3.16 over the same period, continuing its downward trend since peaking in May last year.

Wrapping Up

In summary, slowing Q1 GDP growth, sticky core inflation and tariff-driven trade distortions have created a challenging macro backdrop even as the Fed remains data-dependent. At the same time, landmark regulatory shifts—from the UK’s draft crypto framework to the U.S. bank custody rollback and the SEC’s forthcoming rulemaking—are paving the way for broader institutional adoption. Bitcoin’s late-April rally above $90,000 and record futures open interest contrast with Ethereum’s modest pullback yet continued net inflows and robust DeFi TVL. Finally, with Bitcoin dominance flirting with the 70 percent threshold, the report’s signals point to an imminent rotation into higher-beta altcoin themes as the next phase of market leadership unfolds.