ETF Demand Breaks as Crypto Starts Q3 on Defensive Footing

2nd July 2026 • 6 mins read

This Week’s Recap

- Bitcoin ETFs lose record $4.5B in June: US spot Bitcoin ETFs posted their worst month on record, with $4.5 billion leaving the products in June. The scale matters because it was more than three times the $1.25 billion Strategy authorised through its new Bitcoin sales program, so the money leaving ETFs became a larger source of selling pressure than the biggest public-company Bitcoin buyer could offset.

- Bitcoin retakes $60,000 after Fed Chair Warsh comments: BTC briefly moved back through $60,000 after comments that inflation risks had cooled, but the recovery did not last. The move showed how quickly better economic news can still bring buyers back into crypto, while the weak follow-through left ETF selling and dollar strength in control of the broader market.

- Bitcoin falls below $60,000 and tracks rare back-to-back quarterly losses: Bitcoin slipped below $60,000 after a quarter in which it was down about 12%, following a roughly 22% fall in Q1. CoinDesk noted that two red quarters to start a year have only happened twice in Bitcoin’s history, which makes the current weakness more than a routine pullback.

- Bitcoin’s $60K breakdown sets up volatility shock: More than 550,000 BTC reportedly moved to exchange deposit addresses as traders bought protection against further losses. That combination is dangerous because coins sitting near exchanges can be sold faster, while options activity can add more pressure when prices are already falling.

- Bitcoin faces $4.4 billion in possible extra selling as large buyers weaken: Analysts framed the exchange-bound coin movement as roughly $4.4 billion of possible extra selling at the same time ETF demand was turning negative. The timing is the issue: weaker large-buyer demand gives the market less room to handle new supply near a price level that just broke.

- Strategy initiates buybacks and bitcoin sales plan: Strategy authorised a $2 billion buyback program and introduced a plan that could allow Bitcoin sales to support dividend payments and shareholder returns. The change moved the story from pure Bitcoin buying to balance-sheet management, which is different from the one-way Bitcoin buying story investors had been used to.

- MSTR jumps after Strategy says it may sell Bitcoin to fund dividends and buybacks: MSTR rose after the shareholder-return plan because buybacks can support the stock when investors stop valuing it above its Bitcoin holdings. Shareholders got a support mechanism, but the company also made Bitcoin sales part of the plan, weakening the old “never sell” signal that helped define the brand.

- Strategy valuation falls below the value of its Bitcoin holdings: Strategy’s market value fell below the value of its Bitcoin holdings, meaning investors were no longer giving the company extra credit for the structure around the coins. That is a major shift because the buying model depends on the market treating Strategy’s stock and special dividend-paying shares as a useful way to own Bitcoin indirectly.

- Saylor’s Bitcoin machine hits $8 billion cash wall: STRC traded about 25% below its face value, which pushed the effective payout for buyers near 15%. If those special dividend-paying shares become an expensive way to raise money, the company has fewer easy ways to buy more Bitcoin without pressuring either the balance sheet or existing shareholders.

- Ripple CEO criticises Strategy’s financing model: Brad Garlinghouse stayed bullish on Bitcoin but criticised Strategy’s special-share structure as financial engineering. The comment landed because the debate is no longer whether companies can hold BTC in rising markets; it is whether debt-funded Bitcoin buyers help or hurt crypto when money becomes harder to raise.

- Citi slashes 12 month bitcoin and ether targets: Citi cut its 12 month Bitcoin and Ether forecasts after dropping earlier assumptions about steady ETF demand. The downgrade changes the big-investor base case from “ETF buying supports price” to “price must prove demand can return without automatic ETF buying.”

- Circle slides as Stripe, Coinbase and BlackRock back rival stablecoin network: OpenUSD arrived with more than 140 partners and a model built around no-cost minting, redemption, and reserve-income sharing. That puts pressure on how Circle earns money from USDC distribution, which is why Circle’s stock reacted more sharply than it would to a normal competition headline.

- Jefferies warns on Circle as OpenUSD competition rises: Jefferies warned against treating Circle’s selloff as an automatic bargain because OpenUSD could force a lower-profit stablecoin market. The key risk is not that USDC disappears. It is that platforms, processors, and asset managers demand a larger share of the reserve income that public investors had attached to Circle.

- BNY expands stablecoin services for large clients with Circle’s USDC: BNY added USDC safekeeping and minting services for large clients, giving Circle a credible bank partner while OpenUSD raised competition. Safekeeping, issuing tokens, and reserve access are becoming the harder parts of the stablecoin business as more companies try to launch dollar tokens.

- US starts clock to bring ID checks into stablecoin issuance: US agencies proposed written customer identification programs for direct stablecoin minting and redemption. That makes issuing stablecoins look more like bank account onboarding, especially for issuers that want large financial firms and direct dollar access.

- UK sets 40 billion pound cap on sterling stablecoins: The Bank of England dropped individual wallet limits but kept a 40 billion pound ceiling for major sterling stablecoin issuers. The softer user limits help adoption, but the cap tells large issuers that UK growth will still be controlled like a payments system rather than left entirely to market demand.

- Taiwan passes bank-led crypto law: Taiwan’s Virtual Asset Service Act creates licensing for exchanges and stablecoin issuers, with full reserves, domestic safekeeping, regular audits, and no interest paid to holders. Illegal issuance can carry prison terms and large fines, so banks and regulated safekeeping providers start with an advantage before the market even starts competing for users.

- Australia enforces new Travel Rule for crypto transfers: Australia’s Travel Rule took effect on July 1 with no broad value threshold, requiring reporting entities to collect, verify, and transmit payer and payee information unless an exemption applies. That makes withdrawals and exchange transfers more like bank identity checks, especially for cross-border transfers and hosted wallets.

- Binance tells EU users it will stop services after failing to secure MiCA license: Binance notified EU customers that it would suspend some services after withdrawing its MiCA application in Greece and missing the July 1 licensing cutoff. For users, the issue is whether they can keep using the same exchange. For the industry, it shows MiCA can move customers away from the largest global venue when licensing risk becomes real.

- Coinbase and OKX target Binance’s EU users: Coinbase and OKX moved quickly to capture displaced Binance users, with bonuses reportedly reaching as high as 8%. The offer war shows that regulation is becoming a customer-acquisition event: compliant venues can use licensing status as both a trust signal and a direct growth channel.

- Europe reviews MiCA as July 1 deadline passes: The EU began reviewing whether MiCA needs updates for a market now shaped by stablecoins, tokenisation, and cross-border exchange pressure. MiCA is no longer a future rulebook. It is active law, and regulators are already trying to close the gaps exposed by its first major rollout.

- JPMorgan warns rushed US crypto rules could create loopholes: JPMorgan warned that rushing the CLARITY Act before the August recess could leave oversight gaps. The bank’s concern is practical: if Congress draws boundaries too quickly between the SEC, CFTC, state agencies, and non-custodial developers, the market may get legal clarity in one area while creating blind spots in another.

- CLARITY Act odds fall to 50% this year: Galaxy Digital cut the bill’s passage odds to 50% as the Senate calendar tightened and new political demands entered the process. Tokens that could benefit from clearer market rules may stay under pressure if the bill slips past the current window.

- SEC gives novel ETFs a rethink: The SEC opened a comment period on exchange-traded product rules, putting novel ETF structures back under review. Crypto managers should watch this closely because future products may depend less on one-off approvals and more on a redesigned rule framework for safekeeping, borrowing, staking, and asset eligibility.

- Bitmine lifts Ether holdings as it joins the Russell 1000: Bitmine bought $43 million of ETH and lifted its holdings to about $57 million as it entered the Russell 1000. The index inclusion can bring index-fund ownership into a company now positioned as a public ETH holder, even while direct ETH demand remains weak.

- Ethereum backers launch nonprofit for large financial users: Ethereum supporters launched an independent nonprofit focused on adoption by large financial firms. The timing is useful because Ethereum is fighting weak price action and money leaving its ETFs, so the ecosystem needs more than developer momentum. It needs large financial firms to treat Ethereum as a system they can actually use.

- Aave logs biggest network growth day in nearly five years: Aave added 1,806 new Ethereum wallets in a single day, its strongest new-wallet reading since October 2021, according to Santiment. AAVE was still down on the day but higher over the week across market snapshots, making DeFi lending one of the few areas where usage and price both looked better than the wider market.

- Morpho gets Standard Chartered backing as a DeFi lending project: Standard Chartered initiated coverage on Morpho with a 2030 price target, framing it as a core DeFi lending project rather than a short-term payout trade. Morpho’s pitch is simple: if on-chain lending grows, the project can benefit even when other apps own the customer relationship.

- Tokenized Google stock inflated 7,700% in DeFi lending exploit: A tokenized Google stock price feed was manipulated by 7,700%, letting an attacker borrow against collateral valued at 78 times its real price. The exploit is a warning for tokenized equities: bringing real-world assets onchain does not remove oracle risk, and thin markets can turn a familiar asset into dangerous collateral.

- Polymarket hack losses climb above $3 million: Polymarket losses climbed above $3 million after a frontend compromise, with the platform promising user refunds. The damage came during a World Cup-driven volume boom, which makes the lesson sharper: consumer crypto apps can onboard new users quickly, but a weak interface layer can still break trust even when the underlying markets keep functioning.

Bitcoin Market Analysis

Bitcoin spent the week under pressure, trading near $59,700 after falling below the $60,000 area that had carried much of the prior bounce. The latest price data showed a 1 week decline of 2.19%, a 1 month decline of 16.34%, and a price sitting only 3.34% above the 52 week low near $57,794. The week was defined by a $57,794 to $61,319 range, which kept the market close to the lower edge rather than building a clean recovery. The all-time high near $126,218 is now more than 52% above the current price, so the conversation has shifted from upside targets to damage control.

Source: https://altfins.com/technical-analysis

The chart read was still poor. Short-term, medium-term, and long-term direction labels were all marked Strong Down, and every listed moving average from the 5 day SMA through the 200 day EMA was pointed lower. Momentum was less one-sided than price, with MACD marked bullish even though the absolute reading remained deeply negative, but RSI-14 near 37 kept Bitcoin in neutral territory rather than oversold. That mix fits a market that can bounce without changing character. The downward channel still controls the chart.

The nearest level to watch is now $55,000, while $65,000 and then $80,000 sit above as recovery targets. That is a harsher map than last week, because $60,000 has stopped acting like a clean floor. The lower Bollinger Band near $57,583 lines up with the recent low, which explains why buyers appeared there, but the upper band near $67,070 is still close to the first major test at $65,000 to $67,000. A daily close back above $65,000 would improve the tone. A failure near that level would keep Bitcoin stuck in the same lower range.

Source: https://sosovalue.com/assets/etf/us-btc-spot

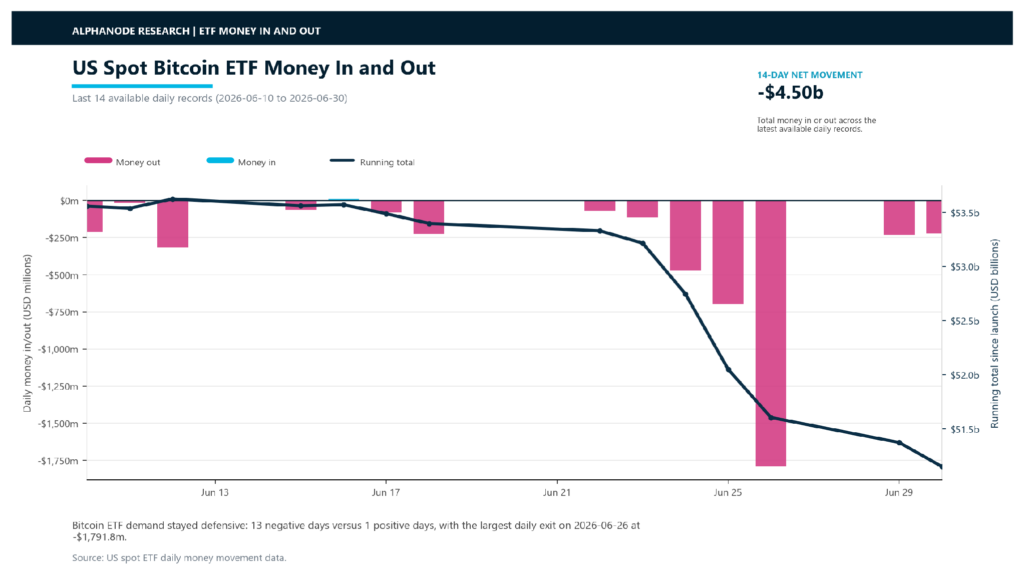

ETF data made the price weakness easier to explain. US spot Bitcoin ETFs lost $4.50 billion across the last 14 available daily records from June 10 to June 30, with money leaving on 13 of those 14 days. June 26 was the worst day in the set at about $1.79 billion of net exits, and June 30 still showed another $222.6 million leaving the products. The products held about $70.95 billion by the latest available date. ETF demand is no longer just choppy. Money has been leaving.

The public-company Bitcoin story also changed tone. Strategy’s authorisation of buybacks and possible Bitcoin sales to fund dividends arrived after its valuation fell below the reported value of its Bitcoin holdings, and STRC weakness raised the cost of its funding model. That does not mean Strategy is finished as a BTC buyer, but it does mean the market is testing whether the balance sheet can hold through a long price decline. Bitcoin did not need another supply concern while ETF money was already leaving.

Citi cut its 12 month bitcoin target as ETF demand dried up, while Cantor argued the bear market may be entering its final stretch. Both can be true over different timeframes. The immediate market is still weak, with $65,000 acting as the first test and $55,000 now the cleaner lower level to watch. The longer-term debate is whether sellers are almost done or whether the market still has another leg lower. The next few sessions need to answer a simple question: can Bitcoin reclaim $60,000 and keep it?

Ethereum Market Analysis

Ethereum’s chart opened from a different place than Bitcoin’s, but it arrived at the same broad conclusion. ETH traded near $1,602 in the latest snapshot, down 1.21% over the week and more than 20% over the month. The range was tight by recent standards, with price moving between $1,552 and $1,646, but the location was uncomfortable. ETH is still only 6.41% above its 52 week low near $1,506 and remains more than 67% below its August 2025 all-time high.

Source: https://altfins.com/technical-analysis

The first level that matters is $1,500. ETH is back near that area, which held in early June, and a break would point toward $1,400 next. The recovery targets sit much higher at $1,800 and then $2,100, so the chart has room to bounce before it proves anything. Short, medium, and long-term direction labels were all Strong Down. ETH is approaching a key level inside a falling market, which can produce a bounce, but it does not prove a full recovery by itself.

The indicators were neutral on the surface and weak underneath. RSI-14 was near 39, which is not oversold, and MACD was marked bullish despite sitting at a negative reading near -68. That mirrors Bitcoin’s setup but with a different rhythm: ETH has not broken a big round level in the same dramatic way, yet it has less support from large buyers and a wider climb before the chart looks healthier. Bollinger Bands ran from about $1,513 to $1,818, putting the current price close to the lower side of the range.

Source: https://sosovalue.com/assets/etf/us-eth-spot

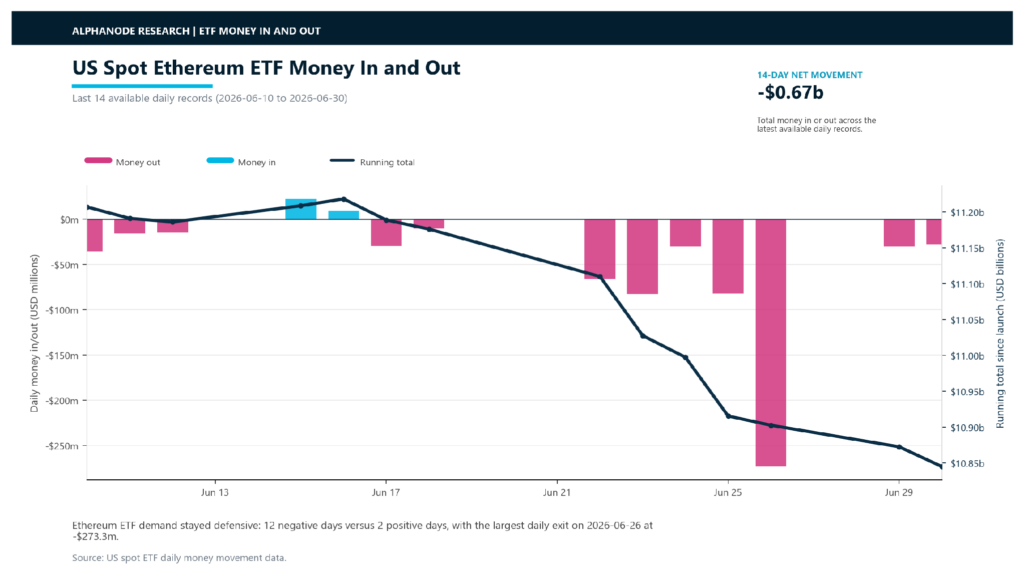

ETF data did not give ETH much cover. US spot ETH ETFs lost $665.2 million across the last 14 available daily records, with money leaving on 12 days and entering on only 2. The worst day in the set was June 26, when $273.3 million left the products, and June 30 still showed another $27.6 million leaving. The products held about $8.33 billion by the end of the window, with about $10.85 billion still in since launch. The ETF market is still alive, but demand has been weak.

Ethereum’s narrative support came from large firms rather than direct buying demand. Bitmine bought $43 million of ETH, Sharplink added 5,000 ETH, and Ethereum backers launched a nonprofit focused on adoption by financial institutions. Those headlines keep the ETH investment story from disappearing during a weak market. They do not offset the money leaving ETFs by themselves.

The risk is that ETH keeps relying on future demand from large firms while current buyers wait for a better entry. A move back above $1,800 would give the rebound a real test, and $2,100 would be the level where the market starts asking whether the decline is losing control. A break below $1,500 would tell a cleaner story in the other direction. For now, Ethereum is sitting near a key price level with ETF selling pulling against it and company-buying headlines trying to slow the fall.

Stablecoin Rules and Rival Networks

Circle became the clearest price signal in the stablecoin fight. CRCL closed at $75.96 on June 29, then fell to $62.63 on June 30 after OpenUSD arrived with backing from Stripe, Coinbase, BlackRock, and a broader partner network. By July 1, the stock was at $61.95. That was not a generic crypto selloff. Investors were questioning how much Circle can keep earning from USDC.

Source: https://www.tradingview.com/

OpenUSD matters because it goes after distribution, not just the token name. A stablecoin with more than 140 partners, no-cost minting and redemption, and reserve-income sharing tells platforms that they do not have to accept USDC’s economics as the default. DefiLlama still shows USDC at about $73.4 billion of supply, or 23.7% of the tracked stablecoin market. The size is real. So is the profit risk.

The rulebook makes that fight harder to ignore. US agencies started the clock on customer identification programs for primary stablecoin issuance and redemption, Taiwan passed a bank-led crypto framework, and Australia’s Travel Rule took effect on July 1. The UK kept a 40 billion pound ceiling on major sterling stablecoins. Rule checks are becoming part of the product. The winners will need distribution, identity checks, bank access, and a fee model that partners are willing to defend.

Circle still has support where it counts. BNY expanded USDC safekeeping and minting services, Credit Agricole is rolling out a euro stablecoin, and JPMorgan is widening blockchain settlement for banks. Those headlines show that regulated stablecoins are moving deeper into finance. The harder question is who keeps the revenue once every major bank, processor, and exchange wants a cut.

Mark Your Calendars

Economic Data Releases:

- July 8, 2026 (Wednesday): Minutes of Fed’s June FOMC meeting and consumer credit

Token Unlock

- July 6, 2026 (Monday): HYPE (HYPE) unlocks about 9.92 million tokens for core contributors

- July 11, 2026 (Saturday): RAIN (RAIN) unlocks about 51.8 billion tokens, roughly 4.51% of total supply