Treasury Sales Made ETF Bleed

4th June 2026 • 11 mins read

This Week’s Recap

- Mt. Gox-linked wallets move 10,422 BTC: The estate shifted about $739 million of Bitcoin to a new address while CoinDesk reported that roughly 34,504 BTC remained in trustee-linked wallets. The move did not prove immediate distribution, but it put dormant supply back into view during the same window ETF demand was thinning.

- Bitcoin crash to $65,000 triggers $1.8 billion in liquidations: Leveraged longs were cleared out as traders started paying for downside protection toward $50,000. The size of the wipeout showed how quickly a support break can turn into forced selling when crowded positioning meets weak spot demand.

- Bitcoin flash crash erases nearly $400 million in one hour: The speed of the move showed how thin bid depth became once $68,000 failed. It also explains why the chart now treats $70,000 as a recovery test rather than a routine intraday level.

- Strategy sells Bitcoin for the first time since 2022: The sale was tiny beside the firm’s stack, but it cracked the assumption that treasury holders only add. The market reacted to the precedent because Strategy has been the cleanest symbol of corporate Bitcoin accumulation.

- Analysts split on Strategy’s sale message: Some analysts treated the 32 BTC sale as economically immaterial, while others saw a new willingness to use Bitcoin to support the capital structure. That divide matters because treasury companies are now being judged on funding discipline as much as coin count.

- Bitcoin ETFs lose $519.2 million in one session: Citi framed the bigger problem as a lack of new buyers, with Strategy’s sale acting as the spark rather than the whole fire. The outflow landed at the same time price was testing support, so the ETF tape became a live demand gauge rather than background data.

- Bitcoin’s biggest ETF selloff hits $3.45 billion: ETF withdrawals stretched across 11 sessions while AI stocks kept attracting the same risk capital Bitcoin wants. The sequence broke the old February 2025 redemption-streak record and showed that ETF access can also make exits easier.

- Digital asset products suffer $1.67 billion in weekly outflows: The second-largest fund exit of 2026 showed that the pressure was sector-wide, even as XRP and HYPE still drew interest. The split says capital was leaving broad crypto beta while traders still chased narrow product or token stories.

- Strive adds 2,500 BTC to treasury: Strive bought $185 million of BTC and lifted holdings to 19,000 coins, giving the treasury trade a buyer while Strategy turned seller. The company also highlighted an 18-month dividend reserve, which is exactly the kind of cash planning investors now want from treasury names.

- Bitwise model sets Bitcoin fair value at $224,000: The model treated Bitcoin as a hedge against G20 sovereign default risk, but price action stayed focused on near-term liquidity. The gap between the model and the tape captured the week well: long-term scarcity arguments had to compete with real-time selling.

- Bitcoin hits a Power Law model discount: The discount resembled levels seen during prior stress events, making the rebound case more visible without confirming it. That gave dip buyers a framework, but the first proof still has to come through $70,000 and ETF stabilization.

- CFTC approves regulated Bitcoin perpetuals: Coinbase and Kalshi gained approval for a product category that has dominated offshore crypto trading. The decision gives US firms a cleaner path into a market built around leverage, funding rates, and round-the-clock price discovery.

- Paxos wins SEC approval to clear US stocks on blockchain: The license gives blockchain settlement a formal path into equities market plumbing. It also broadens the week’s market-structure theme beyond crypto tokens and into the machinery that clears traditional shares.

- CLARITY Act moves through a difficult Senate path: Crypto’s market-structure bill remains alive, but its timeline depends on crowded Senate floor math. The bill still matters for exchanges, token issuers, and stablecoin businesses because regulatory clarity is becoming a capital-allocation input.

- Crypto PACs go 11 for 11 in June primaries: Fairshake’s winning streak kept political pressure behind crypto legislation. The electoral signal gives the industry more leverage in Washington even while prices are moving the other way.

- US seizes about $1 billion in Iranian crypto: The seizure expanded Washington’s financial pressure campaign and tied crypto flows back to geopolitics. It also kept sanctions risk in the same weekly conversation as exchange scrutiny, wallet movement, and Middle East stress.

- UK sanctions Russian crypto network over $90 billion in alleged flows: UK action treated the network more like a sanctioned financial institution than a loose crypto venue. Enforcement is now targeting payment routes as well as exchanges.

- Mastercard expands stablecoin settlement: The payments company will support stablecoin, weekend, holiday, and on-chain settlement across networks including Ethereum, Solana, Polygon, Base, Arbitrum, and XRPL. This is less about a new coin and more about bringing always-on settlement into payment operations.

- Coinbase backs Ethena before savings-product launch: Coinbase Ventures bought ENA as the protocol prepared an onchain savings integration for more than 100 million Coinbase users. The timing links the stablecoin-yield fight in Washington to a real product push from the largest US exchange.

- Ripple brings RLUSD stablecoin to Turkey: Ripple targeted a market processing nearly $200 billion in annual crypto transactions. Turkey remains a useful test case because inflation, payments demand, and local crypto usage can make dollar tokens practical rather than theoretical.

- MoneyGram launches MGUSD on Stellar: The payments firm launched a dollar-backed token issued by Stripe-owned Bridge, with a US rollout first and global plans across its customer base. MoneyGram’s retail network gives the launch a cash-in and cash-out angle that most stablecoin announcements lack.

- UK Lords warn against Bank of England stablecoin caps: Lawmakers argued that a 20,000 pound individual holding cap could make the pound-token market uneconomic. The debate shows how quickly stablecoin policy moves from consumer protection into market design.

- Tom Lee predicts ETH can reach $250,000: The bullish call leaned on corporate validator control, but ETH’s chart was still pointed lower. It gave Ethereum a high-conviction narrative during a week when the token itself was struggling to hold $1,800.

- Standard Chartered moves to acquire Zodia Custody: The planned full buyout keeps bank-owned custody infrastructure in focus. The deal matters because institutional adoption still depends on custody controls even when market prices are weak.

- Vitalik Buterin proposes liquidation-free DeFi design: The research-stage idea would use synthetic index-tracking assets to reduce automatic liquidation cascades. It landed in the same week liquidations dominated the market, which made the design question feel practical rather than academic.

- Aave overhauls asset listing standards: The protocol moved to tighten risk controls after the rsETH exploit exposed bridge and collateral weaknesses. DeFi lending is still judged by uptime and risk discipline whenever market stress returns.

- Kraken parent plans tokenized IPO access: Payward wants retail users to access US IPO shares at the original offering price through tokenized rails. The story connects crypto market infrastructure to the same IPO and AI-capital cycle that is competing with Bitcoin for attention.

- IREN unveils 800MW Australian AI data center campus: The miner’s AI plan showed why power assets are being repriced as data-center capacity. For miners, the AI trade is no longer only a competing capital theme; it is also becoming a business model.

- HIVE reports record $298 million revenue: HIVE reduced BTC holdings to 150 coins while pushing deeper into AI computing. The update fits the broader split among miners between holding Bitcoin and monetizing power for higher-demand compute.

- Zcash fixes network bug after outage: Developers shipped an emergency upgrade after instability halted block production for four hours. The outage kept reliability and security in the weekly mix at a time when investors were already punishing risk.

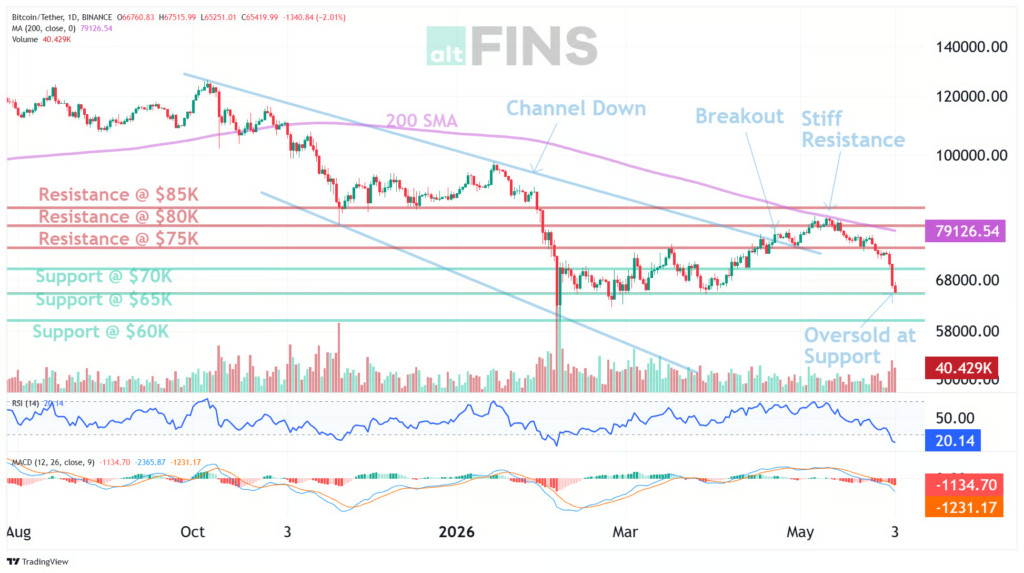

Bitcoin Market Analysis

Bitcoin entered the week with a simple problem: the market lost $70,000, then could not stop the slide quickly enough to keep $65,000 from coming into view. Price was last marked near $63,040, down roughly 15% over the week and about 50% below the October 2025 high. The short-term trade setup is now oversold at support, which can produce a bounce, but the first rebound target is only the old breakdown area near $70,000. A bounce to resistance would ease the tape. It would not repair it.

Source: https://altfins.com/technical-analysis

The level map is narrow and unforgiving. Nearest support sits at $60,000, only a few thousand dollars below the latest price, while resistance is stacked at $75,000 and then $80,000. Bitcoin also crossed below its lower Bollinger Band, with the lower band near $66,633 and the upper band near $81,486. That tells the same story as the chart: price stretched too far on the downside, but the old $75,000 to $80,000 zone has become the area sellers will test first.

Momentum has gone from weak to washed out. Short-term trend is Strong Down, medium-term trend is Strong Down, and long-term trend is Down. RSI-14 is deeply oversold near 18, MACD remains bearish, and the one-week performance sits around -15.3%. Oversold conditions can bring fast relief because shorts cover and late sellers pause. The problem is that trend labels are still pointed lower across every useful horizon.

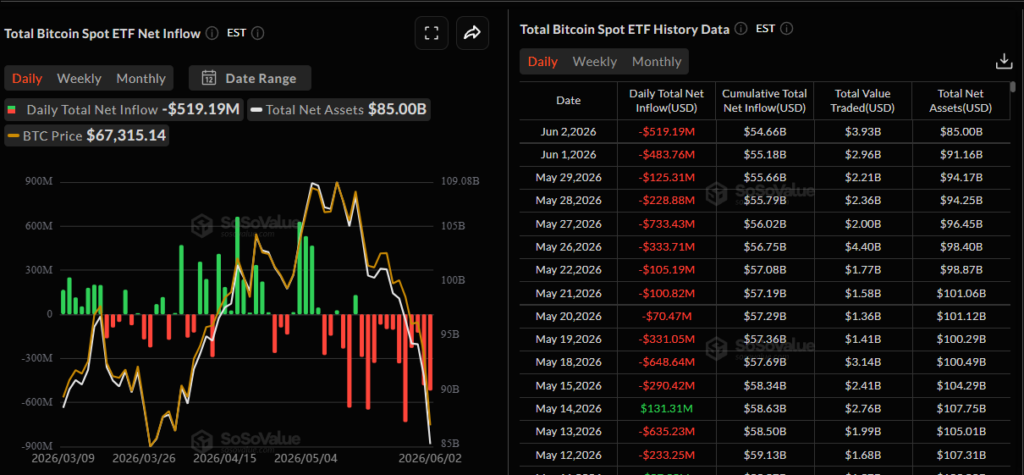

Source: https://sosovalue.com/assets/etf/us-btc-spot

ETF flows are where the weakness turned from chart pressure into a demand question. Spot Bitcoin ETFs lost $519.2 million in the latest snapshot, with about $3.9 billion traded, net assets near $85.0 billion, and cumulative net inflow down to $54.7 billion. CoinDesk reported an 11-session, roughly $3.45 billion outflow streak, the longest redemption run since spot funds launched in 2024. The ETF wrapper is still deep. This week, it was deep enough to let sellers exit.

The treasury story no longer gives Bitcoin a clean cushion. Strategy sold BTC for the first time since 2022, a small move that landed hard because the market had treated Strategy’s stack as permanent demand. Strive bought 2,500 BTC, so corporate buying did not disappear, but buyers and sellers now sit in the same paragraph. Mt. Gox-linked wallets also moved 10,422 BTC, putting old supply back on the board before an October 31, 2026 repayment deadline. That was the week’s inflection.

Bitcoin now needs a better answer than scarcity and long-term models. Bitwise’s $224,000 fair-value argument gives bulls a macro framework, and the Power Law discount gives them a rebound setup. The market is trading the cash problem in front of it. A reclaim of $70,000 would stabilize the tone, and a close above $75,000 would make the bounce harder to dismiss. Below $60,000, the conversation shifts from flush to breakdown.

Ethereum Market Analysis

Ethereum’s week started with the $2,100 support failure and ended near the old $1,800 target. Price was last marked around $1,791, down about 11.5% over the week and less than 3% above its 52-week low. That is a different setup from Bitcoin. BTC is trying to bounce from a major round support zone, while ETH is trying to prove that its next support has not already turned into a magnet.

Source: https://altfins.com/technical-analysis

The chart offers fewer clean positives. ETH broke back below $2,100, and the next support area is $1,800. Resistance is set at $2,400 and then $2,700, which leaves a wide recovery gap before the market can talk about real repair. Price also crossed below its lower Bollinger Band, with the lower band near $1,856 and the upper band near $2,226. That break fits the oversold bounce case, but it also confirms that sellers pushed through the level buyers needed to defend.

Trend is worse than Bitcoin’s. Short, medium, and long-term readings are all Strong Down. RSI-14 is oversold near 19.5, MACD remains bearish, ADX is strong, and one-month performance is down nearly 23%. The strong ADX reading matters because it says the current direction has force behind it. A bounce can still happen, but it has to fight the trend.

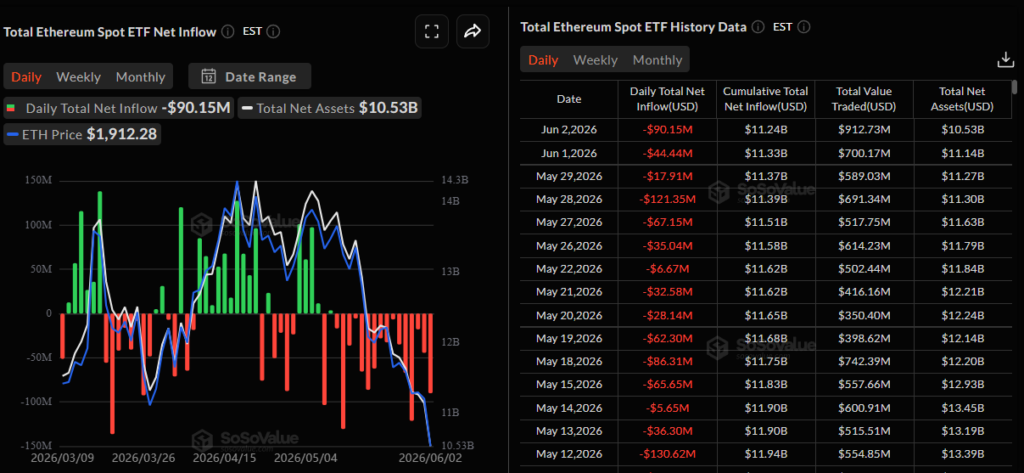

Source: https://sosovalue.com/assets/etf/us-eth-spot

ETF flows did not provide a counterweight. Spot ETH ETFs lost about $90.1 million in the latest snapshot, with $912.7 million traded, net assets near $10.5 billion, and cumulative net inflow around $11.2 billion. Those numbers are smaller than Bitcoin’s, but ETH has less room to absorb disappointment because the chart is already closer to the year’s lows. For ETH, a flat flow tape would have helped. An outflow day made the $1,800 test cleaner.

Ethereum’s better stories are still about structure and applications. Vitalik Buterin floated liquidation-free DeFi designs, and Aave tightened listing standards after bridge-risk losses, both of which speak directly to the failure points exposed during sharp drawdowns. Tom Lee’s $250,000 ETH call put corporate validators back in the conversation, but price did not reward the narrative. Product work is still happening. The token is trading the demand gap.

The next ETH signal is whether $1,800 holds without constant help from oversold readings. A reclaim of $2,100 would be the first sign that the breakdown is being reversed, and $2,400 is the level where the market could start treating the move as more than relief. Standard Chartered’s Zodia Custody deal and Kraken’s tokenized IPO plan keep institutional rails moving forward. ETH needs those rails to show up as actual bid.

The Treasury Bid Starts Answering Harder Questions

Strategy’s 32 BTC sale was small enough to round away and large enough to change the week’s tone. CoinDesk reported it was Strategy’s first BTC sale since December 2022, ending a streak that helped define the corporate treasury trade. The market knew the math. It reacted to the precedent.

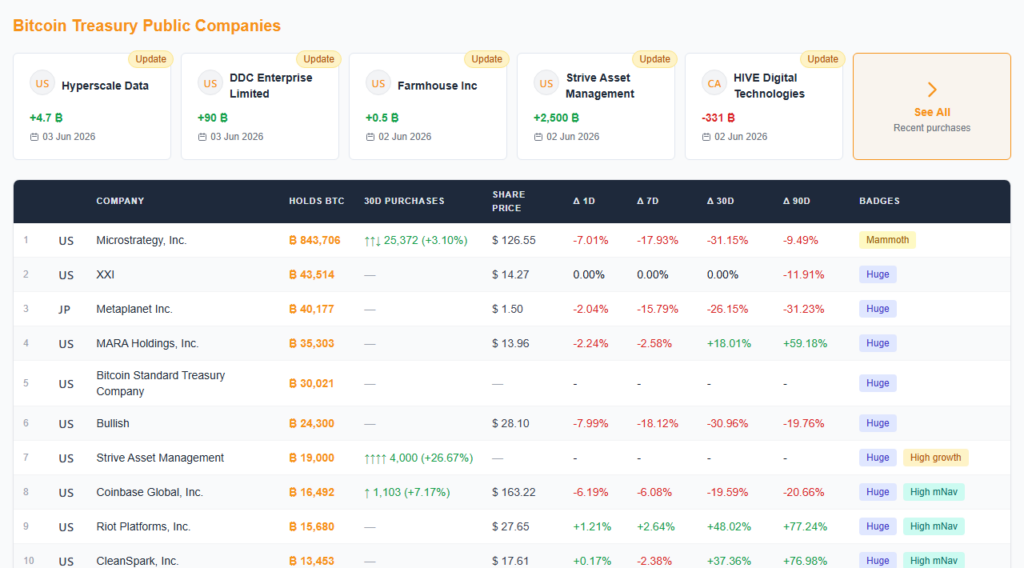

Source: https://cointreasuries.net/

The treasury trade has always depended on a simple belief: balance sheets would absorb supply during stress. That belief got messier this week. Analysts disagreed over whether Strategy’s sale was only tactical or a larger signal, and Strive added 2,500 BTC the next day. Balance-sheet demand is still alive. It is no longer simple.

Mt. Gox made the supply side harder to ignore. Wallets linked to the estate moved 10,422.65 BTC as ETF outflows were already draining demand from the other side of the market, and CoinDesk reported that Mt. Gox still held roughly 34,504 BTC after the transfer. That does not prove immediate selling. It still changes how traders price risk, because dormant supply becomes visible supply the moment coins move.

This is the new test for treasury Bitcoin. The market will give more credit to companies that can buy without leaning on fragile financing and less credit to holders whose capital structure turns Bitcoin into a liquidity source. The bid is still there. It has become selective, and selective demand is weaker than automatic demand when price is breaking support.

Perpetuals Move Back Onshore

The CFTC gave crypto one of its cleaner policy wins of the week. Coinbase and Kalshi received approvals for regulated Bitcoin perpetual futures, bringing a product category that dominates global crypto volume into a US-supervised framework. That is a market-structure change, even if it did not stop the selloff.

Perpetuals matter because they sit where liquidity, leverage, and price discovery meet. Offshore venues built the category first, and US users have often been pushed into indirect routes or limited products. A regulated channel gives institutions a cleaner path to trade continuous crypto exposure without moving entirely outside domestic rules. It also gives US venues a better way to compete with the liquidity that has lived elsewhere.

The timing was awkward. Bitcoin was falling, ETFs were losing assets, and Hyperliquid was being described as a larger venue than NASDAQ by ICE’s CEO. TD Securities said Hyperliquid predicted 80% of an oil-market move before traditional exchanges opened, which is exactly why the onshore approval matters. The US can regulate the product. It still has to win the liquidity.

The next phase is execution. Regulated perpetuals will need enough market makers, clearing capacity, collateral flexibility, and user demand to become more than a compliance-friendly headline. If that happens, the approval could pull a chunk of derivatives activity back into domestic rails. If it does not, offshore and DeFi venues will keep setting the pace while US products trail with better paperwork.

Mark Your Calendars

Economic Data Releases:

- June 5, 2026 (Friday): US nonfarm payrolls report and unemployment rate

- June 5, 2026 (Friday): US consumer credit

- June 6, 2026 (Saturday): Federal Reserve quiet period begins before the next FOMC meeting

Token Unlock

- June 5, 2026 (Friday): OPN (OPN) unlocks about 32.09 million tokens

- June 6, 2026 (Saturday): HYPE (HYPE) unlocks about 9.92 million tokens

- June 7, 2026 (Sunday): RED (RED) unlocks about 40.85 million tokens