Crypto Markets Hold Ground, Liquidity Trends Turn Positive.

31th March 2025 • 13 mins read

Key Numbers:

Bitcoin US$ 83,574.44 (-0.36%) Ethereum US$ 1843.39 (-16.99%)

1-month return

Total Crypto Market Cap US$ 2.7T (-2.8%)

2025 returns

Bitcoin –12.30% Ethereum –45.89% Gold +21.20%

NASDAQ -10.42% S&P500 -4.59%

Key Takeaways

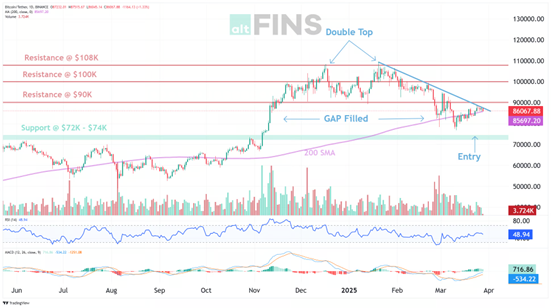

- Bitcoin Consolidates: BTC traded between $80K and $88K after a failed breakout above $95K, showing resilience despite macro headwinds.

- Strategic Reserve Announcement: Trump’s executive order establishing a U.S. Bitcoin Reserve triggered a brief rally and marked Bitcoin’s entrance into sovereign asset status.

- Tariff Uncertainty: Steel, aluminum, and blanket China tariffs went live in March, escalating trade frictions that muddied inflation expectations and investor confidence.

- ETF Outflows Reverse: Following February’s record $1.14B outflow, March saw ETF inflows resume mid-month, signaling institutional reaccumulation at current ranges.

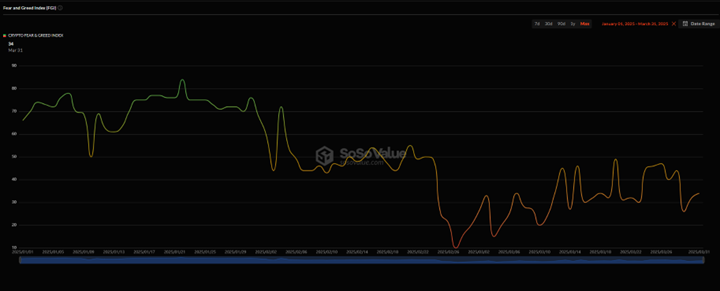

- Fear Bottoms Out: The Crypto Fear & Greed Index hit a low of 10 on Feb 27, but gradually recovered to 34 by month-end, aligning with Bitcoin’s consolidation zone.

- M2 Liquidity Rebound: Global M2 bottomed in late 2024 and surged into Q1 2025. Bitcoin’s historic 10-week lag suggests a rally may be imminent if liquidity trends persist.

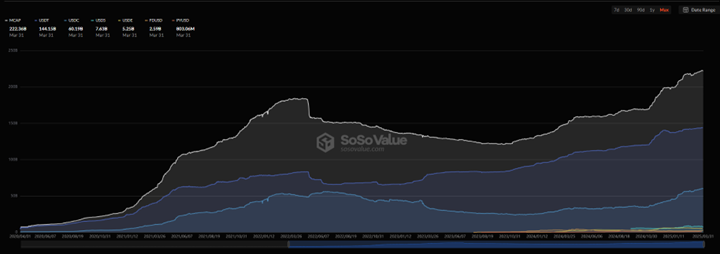

- Stablecoin Growth: USDT and USDC supply grew through March, signaling sidelined capital accumulation despite Bitcoin’s 20% pullback from its $100K high.

- Altcoin Bleed: Sectors like staking, AI, and DePIN suffered sharp losses as speculative capital rotated out. Only exchange tokens posted positive returns.

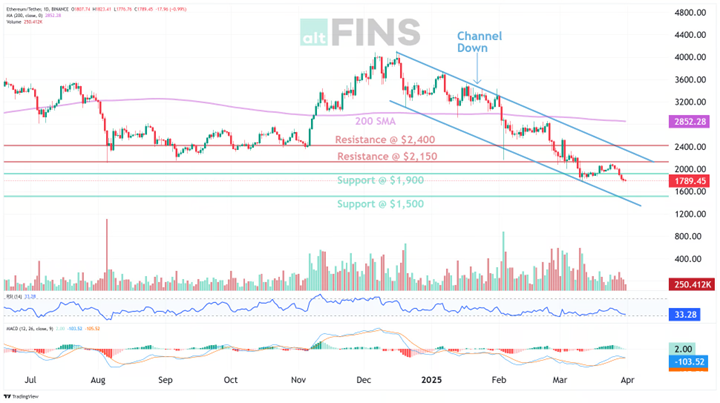

- Ethereum Underperforms: ETH fell nearly 17% on the month, as capital rotated out of its ecosystem and into more efficient L2s and new chains.

- Base Leads L2 Race: Base posted $350M in net inflows and grew TVL by 3.18%, emerging as the most dominant Ethereum L2 in liquidity, usage, and cultural adoption.

- Berachain Momentum: Despite ending its airdrop campaign, Berachain sustained strong inflows and TVL growth, showing traction in its proof-of-liquidity thesis.

- Regulatory Reset: The SEC dropped multiple cases against Coinbase, Kraken, Ripple, and others, as new leadership pivots toward pro-innovation oversight.

- Bitcoin Outperforms Equities: BTC closed March down less than 1%, while the S&P 500 and NASDAQ dropped over 4% and 10% respectively, indicating early signs of decoupling.

- TVL Divergence: Base, Berachain, and BSC saw TVL growth, while Ethereum, Solana, and Arbitrum posted notable declines, suggesting capital rotation amid market consolidation.

Market Overview

Bitcoin’s March performance was defined by volatility and consolidation. Following the announcement of the U.S. Strategic Bitcoin Reserve, BTC surged to a monthly high of $95,000 in a sharp, sentiment-driven rally that quickly reversed. Prices fell back to $76,000 by mid-month, retesting key support levels established in February. From there, the market moved within a tighter range between $80,000 and $88,000, with lower volume and reduced leverage pointing to cautious accumulation. What stood out was Bitcoin’s resilience compared to equities. While the S&P 500 and other major indices pulled back due to inflation concerns and ongoing trade uncertainty.

Source: https://altfins.com/technical-analysis

That shift gained more weight on March 6, when President Trump signed an executive order to establish the U.S. Strategic Bitcoin Reserve and a separate Digital Asset Stockpile. Bitcoin will now be treated as a sovereign strategic asset, separate from other cryptocurrencies that the government may eventually sell. The reserve will be capitalized using Bitcoin seized through enforcement actions, and the plan does not include liquidating these holdings. This move sends a strong signal that Bitcoin is being woven into national financial strategy rather than treated as a speculative commodity. The price spike that followed reflected the market’s recognition of this policy shift.

On the macroeconomic front, The Federal Reserve kept interest rates unchanged in its March meeting, holding firm despite slightly improving inflation data. February’s CPI came in below expectations, giving markets a brief sense of relief, but that optimism was tempered by ongoing trade tensions. President Trump’s tariff policy took center stage, not as a clear escalation, but as a series of strategic moves used to gain leverage in trade negotiations. A 25% tariff on steel and aluminum imports from all countries went live on March 12, triggering retaliation from the European Union, including delayed counter-tariffs set to begin in April. Canada and Mexico were hit with a 25% blanket tariff on March 4, but just two days later, the administration announced a temporary pause on goods compliant with the USMCA, effective through April 2. Meanwhile, new blanket tariffs on Chinese goods raised total duties to around 20%, prompting a response from China that included fresh tariffs on U.S. agricultural products. These back-and-forth measures introduced noise into inflation forecasts and added layers of uncertainty to the broader economic outlook. While some tariffs were implemented, others were delayed or revised, reinforcing the view that Trump is using trade policy as a negotiating tool rather than pursuing a full-scale trade war.

Regulatory developments offered a clearer picture. The Senate Banking Committee advanced the Guiding and Establishing National Innovation for U.S. Stablecoins (GENIUS) Act, setting the stage for a more defined compliance framework. Meanwhile, the Securities and Exchange Commission signaled a softer approach to enforcement. Paul Atkins, known for his support of innovation in financial markets, was nominated as the new SEC Chair. Several crypto-related enforcement cases were dismissed, pointing to a shift in strategy from punishment to structured oversight. This new posture is seen as a step toward building a more constructive regulatory environment that supports growth in the digital asset space.

The White House hosted a Bitcoin Summit on March 7. Industry leaders, policymakers, and institutional players gathered to discuss how digital assets fit into America’s future. Key topics included mining incentives, regulatory clarity, stablecoin legislation, and national economic competitiveness. The summit showed a high level of engagement from government stakeholders, reinforcing that crypto is no longer a fringe issue. It is now a recognized part of U.S. economic planning with long-term implications for both financial innovation and strategic positioning.

Closing out the month, Bitcoin-backed lending also regained momentum in March. With many investors reluctant to sell in a sideways market, interest in unlocking liquidity through collateralized loans surged. Platforms offering BTC-secured lending reported increased usage. Unlike in previous cycles, this round of growth is being supported by more robust infrastructure and stricter risk management. The rise in lending activity highlights Bitcoin’s evolution from a speculative asset to a functional component of financial markets, capable of powering yield strategies and credit products.

Liquidity Signals: M2 and Bitcoin’s Next Leg

Bitcoin continues to closely follow global liquidity cycles, and all signs point to the next major move forming soon. Data from Global Macro Investor shows that Global M2, representing the total money supply across major economies—bottomed in late 2024 and has since sharply reversed. Raoul Pal, citing this M2 rebound, points to Bitcoin’s consistent 10-week lag behind liquidity trends. If the pattern holds, Bitcoin is nearing the point where it historically breaks out, following liquidity back into the system. With BTC still range-bound between $80,000 and $88,000, the current chop may be less a sign of weakness and more a precursor to a liquidity-driven rally.

Source: https://www.lseg.com/

Historically, M2 expansions have been a leading indicator for rallies across risk assets, including equities and crypto. When liquidity floods the system as it did post-COVID, Bitcoin and the S&P 500 both soared. When liquidity contracts, risk assets suffer, as seen during 2014, 2018, and the 2022 cycle. The recent surge in M2 suggests that the tide is turning again. Financial conditions are easing, inflation is cooling, and monetary aggregates are recovering. The 10-week lag shown in Pal’s model implies that Bitcoin is due to respond imminently. As in past cycles, the most explosive upside tends to happen after this delayed reaction. If global M2 continues to climb, the structural tailwinds behind Bitcoin and other risk assets could drive the next phase of the bull market.

Bitcoin Outperforms S&P 500 Amid Macro Pressures

While global equities struggled through March, Bitcoin held its ground. From the February highs into late March, the S&P 500 experienced a steady decline, weighed down by renewed inflation fears and unpredictable tariff posturing from the Trump administration. By March 28, the index had fallen to 5,580 just 1.2 percent above its March 13 low. In contrast, Bitcoin showed resilience, bouncing off its March 10 bottom of $76,900 to close the month around $83,574.44, [FJ1] up over 8.7 percent from its local low.

Source: https://x.com/santimentfeed/

Historically, risk assets like Bitcoin have moved in close correlation with equities, particularly during periods of macro stress. But recent price action shows Bitcoin beginning to decouple, with crypto markets posting modest gains even as stocks remained under pressure. The outperformance suggests that Bitcoin is no longer behaving purely as a speculative tech proxy, but rather as a maturing asset with independent drivers. As liquidity conditions improve and traditional markets remain volatile, Bitcoin’s relative strength may position it as a lead indicator for risk appetite returning. For macro-focused investors, this resilience could mark the early signs of a narrative shift in how digital assets behave under stress.

Sentiment Watch: Fear Bottomed, Confidence Gradually Rebuilding

Crypto market sentiment remains fragile, but signs of recovery are emerging. The Fear and Greed Index hit an extreme low of 10 on February 27, marking the most pessimistic level year-to-date. Since then, it has slowly climbed to 34 by the end of March, with each dip forming a higher low. This shift aligns with Bitcoin’s price consolidation between $80,000 and $88,000 over the past few weeks. Despite volatility and macro headlines, the market has absorbed shocks without a breakdown suggesting that fear may have already peaked.

Source: https://sosovalue.com/dashboard/fgi-indicator

What makes this sentiment recovery notable is how it aligns with deeper macro signals. As discussed in the M2 analysis earlier, global liquidity has already turned upward since late 2024, and Bitcoin tends to follow M2 with a 10-week lag. The fear-driven consolidation we’re seeing now could be the final phase before that liquidity impulse begins to flow into prices. Historically, when sentiment bottoms ahead of rising liquidity, markets tend to reprice quickly once confidence returns. So long as no massive negative news breaks the current range, the fear-driven lows of February and early March could prove to be the local bottom.

ETF Flows: From Capitulation to Accumulation

The first half of March continued the outflow trend that began in late February, as Bitcoin struggled to regain momentum following its rejection at the $100,000 level on February 21. That rejection triggered a sharp pullback to $80,000 by February 28, which coincided with the largest single-day outflow in ETF history, $1.14 billion exited on February 25. These exits reflected widespread profit-taking from Q4’s strong rally, particularly from traditional investors locking in gains as Bitcoin crossed into six-figure territory. Early March showed more of the same, with ETFs experiencing steady outflows as the market searched for direction.

Source: https://sosovalue.com/dashboard/total-crypto-spot-etf-fund-flow

By mid-March, the tone began to shift. Between March 14 and March 27, ETF flows flipped positive, with consistent inflows coinciding with Bitcoin’s consolidation between $80,000 and $88,000. This pattern suggests that institutions are beginning to accumulate within this range, viewing it as a stable entry point after February’s reset. Although assets under management remain below peak levels, the return of inflows supports the idea that the worst of the shakeout has passed. When combined with rising global M2 and recovering sentiment indicators, ETF behavior in late March adds to the growing case that this range may serve as a base before the next major move.

Ethereum’s Performance

Ethereum significantly underperformed the broader market in March, falling 16.99% from $2,221.20 to $1,843.00. This decline stood in contrast to Bitcoin’s relatively stable range-bound movement between $80,000 and $88,000. While overall market caution contributed to ETH’s pullback, its deeper losses reflected growing competition from faster and cheaper chains like Solana, as well as uncertainty surrounding Ethereum-based financial products. Despite its foundational role in Web3 and institutional interest, Ethereum’s narrative cooled during the month, as capital rotated into assets showing stronger momentum

Source: https://altfins.com/technical-analysis

A key factor in the decline was the delay of the Pectra upgrade. Originally planned for earlier in the year, the upgrade was pushed back after developers encountered issues during testnet phases, including block synchronization problems and empty block production. To ensure network stability, a third testnet named Hoodi was launched in March, delaying the rollout of the mainnet upgrade. At the same time, Ethereum ETFs institutional interest slowed down, and their lack of staking functionality has become a limiting factor. BlackRock’s head of digital assets, Robbie Mitchnick, described the current ETH ETF products as successful but incomplete, noting that staking is an essential part of Ethereum’s value proposition. Without it, the ETFs offer less yield potential, which may be deterring some investors. Staking remains a meaningful source of return, with yields ranging from 2 to 7 percent annually. If regulatory clarity allows for staking to be included in these products, it could become a key catalyst for renewed institutional demand.

Stablecoin Market Cap Climbs Despite Bitcoin Pullback

Source: https://sosovalue.com/dashboard/total-crypto-spot-etf-fund-flow

One of the more telling signals in March came from the stablecoin market. While Bitcoin retraced from its $100,000 rejection on February 21 and consolidated between $80,000 and $88,000 throughout March, the total stablecoin market cap continued to rise steadily. Unlike BTC, which saw volatility and a near 20 percent drawdown from its peak, stablecoin supply led by USDT and USDC did not follow suit. The uptrend remained intact, highlighting that capital was not flowing out of the crypto ecosystem, but instead reallocating to stable positions.

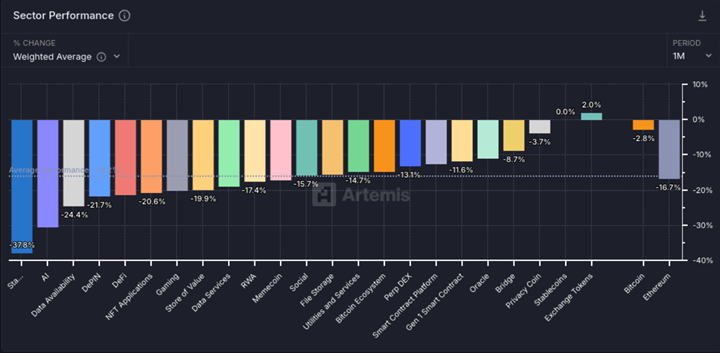

Sector Performance: Altcoins Bleed as Bitcoin Holds Range

March saw a clear divergence between Bitcoin’s relative stability and deep underperformance across most crypto sectors. While BTC traded sideways, the majority of altcoin sectors experienced significant drawdowns, revealing how fragile speculative appetite remains outside of Bitcoin.

Source: https://app.artemis.xyz/

The hardest-hit categories were Staking protocols, AI tokens, and data availability projects, with weighted average declines far exceeding the broader market drop. These sectors, which had seen strong inflows during the early-year rally, suffered from profit-taking and rotation as momentum faded. DePIN, NFT applications, and gaming sectors followed closely, all declining sharply as risk appetite across mid and low caps dried up. In contrast, only a few sectors avoided the bleed. Exchange tokens posted the only positive return among all tracked sectors, while stablecoins ended the month flat. Bitcoin outperformed most sectors despite a modest decline, further reinforcing its dominant position during risk-off conditions. Ethereum lagged slightly, reflecting weaker flows into its broader ecosystem.

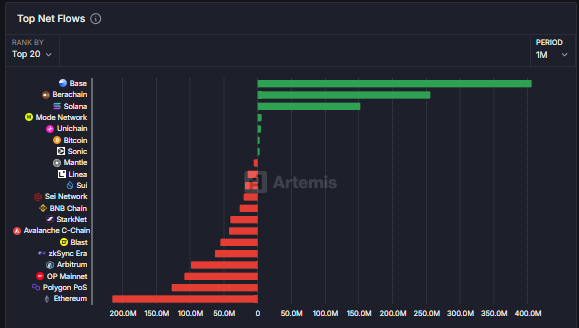

Blockchain Landscape: Base Surges Ahead in L2 Race as Newcomers Attract Capital

Over the past 30 days, net flow data has revealed a shift in ecosystem momentum. Base, Berachain, and Solana led all networks in net positive inflows, while Ethereum mainnet, Arbitrum, Optimism, and Polygon PoS recorded some of the largest outflows. Ethereum’s outflow was the most significant, reflecting a pause in user activity or value migration to more cost-effective chains. Meanwhile, some previously popular L2s like Arbitrum and Optimism are showing signs of stagnation, with capital rotating elsewhere as users and protocols explore faster, cheaper alternatives.

Source: https://app.artemis.xyz/flows

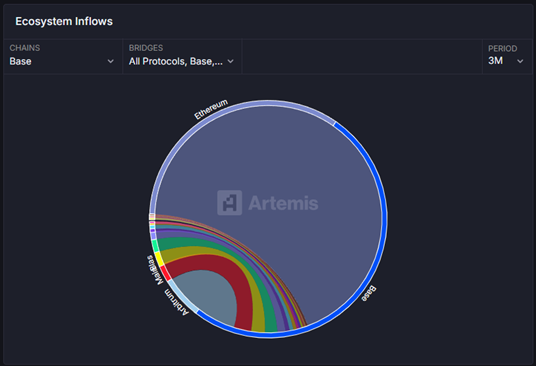

A deeper look into bridge flows shows that Base’s rise is coming directly at the expense of Ethereum mainnet, Arbitrum, and Optimism. Capital is not just entering the crypto ecosystem—it’s being reallocated, with Base acting as a major beneficiary. Ethereum remains the primary source of these bridge inflows, but Arbitrum and Optimism rank among the largest contributors to Base’s liquidity growth. This trend signals more than experimentation; it’s a signal of consolidation as users shift toward the L2 offering the best combination of low fees, accessibility, and velocity of innovation.

Source: https://app.artemis.xyz/flows

Berachain’s strong performance is equally surprising. Despite wrapping up its airdrop farming season earlier this quarter, the chain continues to attract significant net inflows. As a newcomer with a still-developing ecosystem, Berachain’s ability to retain capital post-farming speaks to real interest in its proof-of-liquidity model and DeFi-native culture. Its design choices and strong early community support appear to be anchoring capital longer than expected. For a chain still in its early stages, its inclusion among the month’s top performers is a signal that attention is already shifting to the next generation of modular, purpose-built chains.

Wrapping Up

March 2025 was a month of consolidation, with Bitcoin moving within a stable range between $80K and $88K. While price action remained muted, key developments in policy, regulation, and market structure continued to unfold. ETF outflows from February began to reverse mid-month, stablecoin supply steadily increased, and regulatory pressure eased, especially with several SEC cases being dropped. Altcoins underperformed, but Bitcoin’s relative strength pointed to a more cautious, accumulation-driven environment.

At the ecosystem level, Base and Berachain saw positive momentum in both inflows and TVL, suggesting selective interest despite broader market hesitation. Sentiment showed signs of recovery, and macro liquidity indicators continued to improve. While March did not deliver strong upside, it helped establish a more stable foundation. If current trends continue, April may offer a more favorable setup for renewed movement in the crypto market.